Pension Alert: Secure Funded Status!

Source: Pension Alert: Secure Funded Status!

Private Pension Alert: Secure Funded Status!

The pension objective is to secure benefits in a cost-efficient manner!

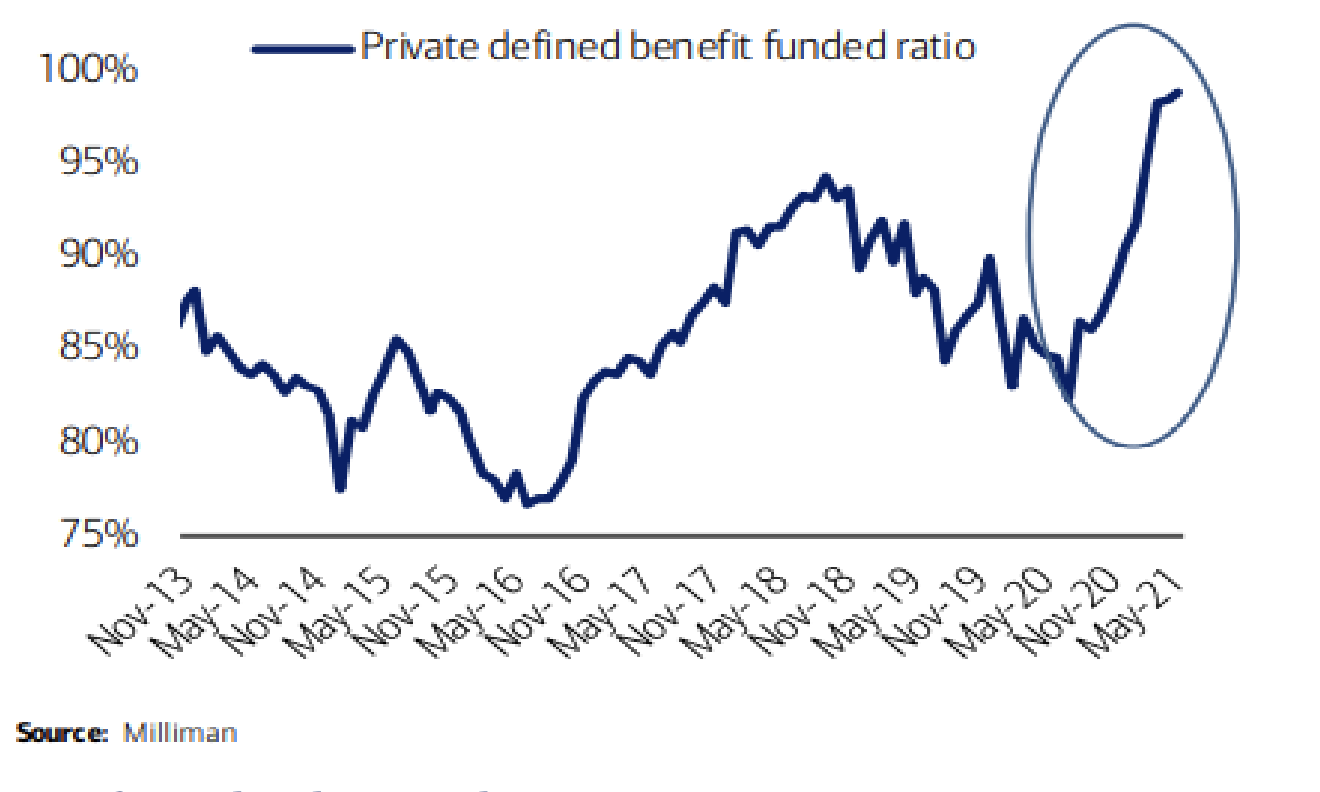

Many private pension plans are in the best funded status since 1999. It should be a high priority to secure this funded status NOW if not enhance it.

Secure Benefits and Reduce Funding Costs

There are basically only two ways to secure pension benefits: insurance annuities and defeasement (through cash flow matching benefit payments). Ryan ALM has been a pension watchdog and written many articles on the benefits of cash flow matching. Insurance buyout annuities (IBA) are expensive, but corporations are purchasing IBAs in record amounts to get rid of the high and rising PBGC premiums caused by the MAP 21 legislation of July 6, 2012 and to avoid longevity risk. However, corporations would be wise to do a cost analysis of the IBA versus a cash flow matching defeasance. The typical IBA prices Retired Lives (liabilities) at a discount rate of ASC 715 (AA corporate zero-coupon yield curve) plus a 3% to 4% premium. According to our calculations, a defeasance strategy (cash flow matching) using investment grade corporates would provide a cost savings of about 30% versus IBA, which is a very significant cost savings and should be reviewed. Such cost savings are immediate while the IBA savings of eliminating PBGC premiums is in the future.

Cash flow matching (using the Ryan ALM Liability Beta Portfolio™) is a cost optimization process where we go through numerous iterations to find the optimal cost savings that will fund each and every monthly Retired Lives benefit payment. Since liabilities are priced like bonds (ASC 715 discount rates) they behave like bonds. As a result, bonds become the proper assets to match and fund liabilities. Bond math tells us that the longer the maturity and the higher the yield… the lower the cost. Our LBP model skews the portfolio weights to longer maturities such that a 30-year coupon bond will partially fund 29 years of benefits through interest income. The same is true for a 29-year, 28-year, 27-year bond, etc. plus principal cash flow at maturities adds even more cash flow. Cash flow matching reduces funding risk because the bond cash flows are certain and the bonds may be held to maturity. Moreover, cash flow matching is the matching and funding of future values which do not change with changes in interest rates.

Reduce and Stabilize Contribution Costs

The LBP will match each and every monthly benefit payment in the liability schedule it is funding (Retired Lives). This will greatly reduce funded status volatility which will help stabilize contribution costs. The LBP is comprised of investment grade bonds skewed to longer maturities and A/BBB credits, so it will out yield liabilities priced as AA corporates (ASC 715 discount rates) by 50 – 100+ bps. Importantly, this extra yield creates an excess return (Alpha), which enhances the funded status, reduces contribution costs and could reduce the PBGC variable premium.

Only cash flow matching (defeasance) can secure benefits and reduce funding costs with certainty! By matching liabilities (benefit payments) it reduces risk accordingly.

Our LBP has numerous benefits that best achieve the true pension objective:

Cash flow matching the liability benefit payment schedule (Retired Lives) at the lowest cost is the ideal way to manage assets for a pension plan. Since Retired Lives are the most certain and most important (most tenured employees) liabilities, cash flow matching is a perfect fit given the certainty of the bond cash flows. Since the pension objective is a cost focus, cash flow matching would produce the optimal cost savings. We urge corporations to do a cost analysis before they buy an IBA! Even if an IBA is the future goal then the LBP would provide the perfect pension risk transfer of assets to an IBA.

Problem: Immunization (Duration Matching)

Duration matching is a strategy that attempts to reduce financial statement volatility while cash flow matching is a strategy for reducing funding volatility. Another difference is that duration is an ever-changing number so with duration matching the manager must continually rebalance for duration drift, while cash flow matching has the advantage that bond cash flows do not change. When we use duration matching to hedge financial statement volatility, we make assumptions that the yield levels of the liability hedging vehicle will move in parallel with liability yields. The fact is yields for different credits, and maturities do not all move in parallel. To facilitate benefits funding management ALM should focus on the liability yield curve or term structure which is exactly what the Ryan ALM custom liabilities cash flow matching and $ duration matching portfolios do in the most cost-efficient manner.

Traditional duration matching has definite liability cash flow mismatches and cost inefficiencies. Since the longest duration coupon bonds are around 19-years today, duration matching is forced to use Treasury zero-coupon bonds (STRIPS) to fund any liability past 19-years. Since Treasuries are the lowest yielding bonds, they are the highest cost bonds to fund and match liabilities. Moreover, duration is a present value (PV) calculation that is very interest rate sensitive. Duration matching is focused on matching liability % growth rates and not on matching and funding benefit payments (future values) and dollar growth rates.

Solution: Dollar Duration Matching (DDM)

DDM matches the dollar value change per basis point change in yield for assets with the dollar value change per basis point change in yield for liabilities. When the dollar duration of assets is matched to the dollar duration of liabilities for every year in the term structure of liabilities, then DDM is in its most precise form. That would be the equivalent of 30 Key Rate durations… one at every point along the liabilities yield cure or benefit payment schedule. The Ryan ALM DDM approach offers several value-added differences:

Actuarial Projections - We use the actuarial projected benefits of our clients and not a generic bond index benchmark.

Modified durations - to be an effective price sensitivity measurement, duration must be modified. Modified Duration measures the percent change in market value or present value for future value cash flows given a 100-basis point movement in yield.

The Ryan ALM DDM approach greatly improves the accuracy of Key Rate duration matching by matching the dollar value changes in liabilities with the dollar value changes in assets across the term structure and yield curve for liabilities. The liabilities are measured and monitored by using a Custom Liability Index (CLI) to more precisely calculate the dollar value (PV) movement in assets versus liabilities given any movement in interest rates.