Ryan ALM

White Papers

Browse

What Do Pension Sponsors Want For Christmas?

When asked this question, most pension sponsors would answer lower or stable pension cost and lower volatility on funded status, yet the asset allocation of most pension plans is...

Source: What Do Pension Sponsors Want For Christmas?

When asked this question, most pension sponsors would answer:

Lower or stable pension cost

Lower volatility on funded status

Yet the asset allocation of most pension plans is skewed to risky and volatile assets. This skewness has created a long history of volatile funded ratios and increasing contribution costs. Fortunately, there is a product that will provide the answers pensions have long sought: Cash Flow Matching!

Given that the true objective of a pension is to fully fund benefits and expenses (liabilities) in a cost-efficient manner with prudent risk, plan sponsors and their consultants should be installing a strategy that is the best fit to achieve this true pension objective. CFM is a portfolio of investment grade bonds that provide an accurate and timely match of monthly asset cash flows to fully fund monthly liability cash flows.

The intrinsic value in bonds is the certainty of their cash flows (only asset class with such certainty). Bond math teaches us that the longer the maturity and the higher the yield… the lower the cost. The Ryan ALM CFM portfolio is created through a cost optimization model that fully funds monthly liability cash flows at a cost savings of about 2% per year (20% to fund 1-10-year liabilities). We call our CFM mode the Liability Beta Portfolio (LBP). The LBP should be the core portfolio for any DB pension fund replacing active fixed income management, which is highly interest rate sensitive. Since pension liabilities are future value costs the monthly payments are not interest rate sensitive. As a result, by matching the FV of liabilities, CFM mitigates interest rate risk! By matching and funding liabilities chronologically, the LBP also buys time for the performance or Alpha assets to grow unencumbered. The pension plan can gradually enhance its funded status and stabilize contribution costs by having CFM work in harmony with the Alpha assets. There are numerous benefits to a CFM strategy:

No need for cash sweep as LBP provides the liquidity to fully fund liabilities

Secures benefits for time horizon LBP is funding (example 1-10 years)

Buys time for performance assets to grow unencumbered

Outyields active bond management enhancing ROA

Reduces Volatility of Funded Ratio/Status

Reduces Volatility of Contribution costs

Low Investment Advisory Cost = 15 bps

Reduces Funding costs (2% per year)

Mitigates Interest Rate Risk

Pension Strategy to Reduce Funding Costs by 20%+

The true objective of a pension is to secure and fully fund benefits in a cost-efficient manner with prudent risk . It is a liability and cost objective… it is...

Source: Pension Strategy to Reduce Funding Costs by 20%+

The true objective of a pension is to secure and fully fund benefits in a cost-efficient manner with prudent risk. It is a liability and cost objective… it is NOT a return objective! This objective is best accomplished through a cash flow matching strategy where an optimal bond portfolio will fully fund monthly benefits + administrative expenses net of contributions. Bonds are the only asset class with certainty of its cash flows. That is why bonds have been the asset choice to defease liabilities for over 50 years.

Cash flow matching (CFM) used to be called Dedication in the 1970s and 1980s. As the head of Fixed Income Research at Lehman in the 1970s and early 1980s, I was in charge of our Dedication model. When I created my initial firm in 1984 (Ryan Financial Strategy Group), I hired the two professors in charge of Dedication at I.P. Sharpe to build our model. At Ryan ALM, we have rebuilt a CFM model that best fits any liability objective. The Ryan ALM CFM strategy utilizes our proprietary cost optimization model that will fully fund monthly net liabilities and reduce funding costs by about 2% per year. If we CFM 1-10 years of net liabilities, we should be able to reduce funding costs by about 20%, 1-15 years = 30%, etc. In addition to reducing funding costs, CFM has several benefits that should be utilized and recognized. We strongly urge pensions to consider CFM as the core portfolio that best fits the true pension objective and provides many additional benefits as listed below:

Cash Flow Matching – Provides Liquidity

The intrinsic value of bonds is the certainty of their cash flows! If bonds were used to cash flow match and fund net liabilities (benefits - contributions) chronologically they would produce the liquidity needed to fully fund such net liabilities. Cash flow matching works best with longer coupon bonds where you use semi-annual interest income cash flows to partially fund liabilities. A 10-year bond has 20 interest cash flows + one principal cash flow all priced at a 10-year yield. This would eliminate the need to do a cash sweep of other asset classes which is a common liquidity procedure. According to S&P data, the S&P 500 has 48% of its historical returns from dividends and reinvestment since 1940 on a 10-year rolling period basis. Wouldn’t you want to reinvest dividends back into growth assets rather than spend it on funding benefits + expenses? Wouldn’t you want the ROA of growth assets enhanced?

Cash Flow Matching - Provides TIME

Ryan ALM, Inc. released a 2022 research report titled “Most Important Asset of a Pension… Time!”. By using bonds as the liquidity assets, the growth assets are left unencumbered to grow. The longer the cash flow matching period, the more time the growth assets have to compound their growth. This could significantly enhance the ROA. By cash flow matching net liabilities chronologically, Ryan ALM can buy the time a plan sponsor and their consultant feel is necessary for the growth assets to grow unencumbered… and recover from negative return years. When markets correct and go down (i.e. 2022) it may take several years to recover and achieve the average annual target ROA that was assigned to that asset class.

Cash Flow Matching – Provides Inflation Hedge

Ryan ALM released a 2020 research report and pension alert titled “Pension Inflation =/= CPI”. Pension inflation has three parts: a cost of living adjustment (COLA) lives; a salary increase factor for active lives and a forecast of administrative expenses. The COLA may be based on the CPI but with a floor and a cap or even a % of the CPI while the salary and administrative expense increases tend to be quite static @ 3% annual increase. As a result, pension inflation tends to be less volatile and more static than the CPI. The plan sponsor actuary includes pension inflation in their projected benefit + expenses payment schedule for both retired and active lives. This fact suggests clearly that the best way (and only way) to hedge pension inflation is to cash flow match the actuarial projected benefits + expenses. If you cash flow match the actuarial projections, you have defeased liabilities and hedged pension inflation.

Cash Flow Matching – Outyields Benchmark and Bond ROA

The Ryan ALM cash flow matching product (Liability Beta Portfolio or LBP) is heavily skewed to A/BBB corporate bonds while the BB Aggregate is heavily skewed to Government bonds. As a result, the LBP will outyield the BB Aggregate by a significant yield spread… usually 50 – 75 bps, which will enhance the ROA of bonds.

Higher Yields are Good for Cash Flow Matching… and Pensions

Ryan ALM released a topical 2022 research report titled “Why Higher Interest Rates are Good for Pensions”. Pension funds are highly interest rate sensitive! Certainly, fixed income assets are such that the longer their maturity and effective duration, the greater their interest rate sensitivity. But it is pension liabilities that are more interest rate sensitive. Liabilities behave like a 100% zero-coupon bond portfolio because the discount rate(s) chosen price liabilities as zero-coupon bonds. This causes liabilities to be longer in duration then the same maturity(s) coupon bonds. Many discount rates are a yield curve of rates (ASC 715, PPA, PBGC, IASB). As interest rates trend higher, bonds can cash flow match liabilities at lower and lower costs. Note that cash flow matching is focused on funding B + E which are future values. Future values are not interest rate sensitive. Bonds are the only asset class with the certainty of cash flows (future values). That is why bonds have always been used as the methodology for defeasance (cash flow matching) of liabilities. Moreover, if interest rates trend upward any reinvestment of cash flow can buy future value at a lower cost. As a result, cash flow matching sees higher interest rates as an opportunity to reduce funding costs. The Ryan ALM cash flow matching product can reduce funding costs by @ 20% for most pension liabilities out to 10 years. In contrast, bonds used as performance or growth assets could see negative returns… like 2022. Total return performance is not the value in bonds… the certainty of cash flow is the intrinsic value. We urge pensions to transfer their bond allocation from focusing on outperforming some generic bond index to focusing on cash flow matching liabilities chronologically, especially at today’s higher rates.

Reminder: The ROA is Plural… ROAs

Ryan ALM, Inc. released a topical 2022 research report titled “The Pension ROA is plural… ROAs” that details how the ROA is calculated. Each asset class is askby using their index benchmark as the target return proxy. However, for fixed income it is the YIELD of the index benchmark… not the total return like other asset classes. The Bloomberg Barclay Aggregate is most favored as the bond index benchmark. This index and almost all popular bond index benchmarks were designed at Lehman Bros. by me (Ron Ryan) when I was the head of Fixed Income Research & Strategy from 1977 to 1983. Please note… each asset class is NOT required to earn the pension fund ROA assumption (@ 6.50% today). This is an important fact to remember in asset allocation. We at Ryan ALM often hear the criticism and question… how can we invest in 4% bonds to earn our ROA? The answer is bonds do NOT need to earn the pension ROA… just their assigned ROA (yield of index benchmark) in the asset allocation model.

Immunizing Pension Expense Volatility

Pension management is an Assets vs. Liabilities objective. Corporations tend to focus on pension expense since it is a direct hit to earnings and stockholder value. Corporations do not want...

Source: Immunizing Pension Expense Volatility

Pension management is an Assets vs. Liabilities objective. Corporations tend to focus on pension expense since it is a direct hit to earnings and stockholder value. Corporations do not want volatility on earnings coming from pension expense. The major factors affecting pension expense are the dollar growth of assets minus the dollar growth in liabilities. This is in sharp contrast to a % growth difference (ROA of assets – discount rate of liabilities). Pension expense is all about dollars not %. There are two primary liability driven investment (LDI) bond strategies in use today: Duration Matching and Cash Flow Matching.

Duration Matching

The purpose of duration matching is for assets to match the interest rate sensitivity of liabilities (immunization). The objective is to have the market value change (% growth rate) in the immunization bond portfolio match the % growth rate (discount rate) in liabilities for a given change in interest rates. Many LDI fixed income managers attempt to match the average duration of their bond portfolio to the average duration of a bond market index with a similar duration to liabilities (i.e., Bloomberg Barclays long corporate index). They use the bond index as a proxy for liabilities. There are several problems and flaws with this strategy.

A generic bond index cannot replicate any clients’ unique liabilities cash flows. Client’s liabilities are like snowflakes: different labor force, salaries, mortality, etc..

Average durations give erroneous information because there are a numerous number of combinations of maturities for a bond portfolio that can all have the same average duration, but they will not have the same risk/reward profile or interest rate sensitivity.

Duration matching is only accurate for small parallel shifts in the yield curve. But the yield curve rarely moves an equal number of basis points at every point along the curve.

FASB requires a single discount rate for financial statements which does not calculate a proper target duration. You need to use the ASC 715 discount rate yield curve.

LDI bond management evolved to remedy these flaws by using Key Rate durations which attempt to match the duration of multiple points along the liability yield curve. Key Rate duration is an improvement over a single average duration, but still has several deficiencies:

Actuaries usually do not provide the average duration of liabilities and the projected benefits in their annual actuarial report… reason why generic bond indexes are used.

Matching key rate durations of a generic market index = wrong Key Rate durations.

Duration is a present value calculation requiring pricing each projected benefit with a different discount rate (i.e., ASC 715 discount rates yield curve). As a result, 30 annual benefit payments require 30 separate discount rates and 30 key rate durations.

Duration must be modified (duration/1+YTM) to use as a price return or interest rate sensitivity measurement.

Solution: Dollar Duration Matching (DDM)

DDM matches the dollar value change per basis point change in yield for assets with the dollar value change per basis point change in yield for liabilities. When the dollar duration of assets is matched to the dollar duration of liabilities for every year in the term structure of liabilities, then DDM is in its most precise form. That would be the equivalent of 30 Key Rate durations… one at every point along the liabilities yield cure or benefit payment schedule (30 years = 30 key rate durations). Ryan ALM recommends DDM for Active Lives liabilities. The Ryan ALM DDM approach offers several value-added differences:

Actuarial Projections - We use the actuarial projected benefits of our clients and not a generic bond index benchmark.

Modified durations - to be an effective price sensitivity measurement, duration must be modified. Modified Duration measures the percent change in market value or present value for future value cash flows given a 100-basis point movement in yield.

Dollar duration - our objective here is to match the dollar value change per basis point in assets and liabilities in every annual liability maturity or duration.

The Ryan ALM DDM approach greatly improves the accuracy of Key Rate duration matching by matching the dollar value changes in liabilities with the dollar value changes in assets across the liabilities term structure. DDM is in harmony with the corporate objective of immunizing pension expense. The liabilities are measured and monitored by using a Custom Liability Index (CLI) to more precisely calculate the dollar value (PV) movement in assets versus liabilities given any movement in interest rates. The CLI is the most appropriate benchmark for any asset liability management (ALM) and should be the first step in any LDI strategy.

ASC 715 Discount Rates – Ryan ALM is one of few vendors providing ASC 715 discount rates (AA corporate zero-coupon bonds as a yield curve). We will price each actuarial projected benefit payment on a monthly basis.

Custom Liability Index (CLI) - The CLI provides all of the calculations needed for either dollar duration matching or cash flow matching. The CLI will calculate YTM, modified duration, actual growth rate and interest rate sensitivity for each projected benefit as a term structure as well as total liabilities showing both the % and $ change in present values.

Liability Beta Portfolio™ (LBP) – our LBP will dollar duration match or cash flow match projected benefits chronologically using our proprietary LBP cost optimization model that will secure benefits, reduce funding costs significantly as well as immunize interest rate sensitivity.

Solution: Cash Flow Matching (CDI)

Ryan ALM believes that the true objective for a defined benefit pension is to fund and secure benefits when due in a cost-efficient manner. The value in bonds is in the certainty of their known and scheduled cash flows which is why cash flow matching has been used as a major strategy for hedging liabilities for many decades (i.e., dedication, defeasance). It is the matching and funding of benefits (future values) that is the primary focus of cash flow driven investments (CDI). As such, future values are not interest rate sensitive… a major benefit of cash flow matching. Cash flow driven investing (CDI) dominates the way European pensions are managed under IASB accounting standards. Key Rate duration and especially dollar duration matching (DDM) are good for matching present value movements between assets and liabilities but do not focus on funding liability payments (future values). Pensions require liquidity that is sufficient and timely to fund benefits + expenses (B+E). CDI will cash flow match both B+E based on the actuarial projections. CDI is a best fit to fund Retired Lives given their higher degree of certainty. Active Lives might be best served with dollar duration matching (DDM) given the actuarial noise and uncertainty of such actuarial projections.

Since the primary value in bonds is in the certainty of their cash flows, Ryan ALM will cash flow match projected benefit payments chronologically. This provides numerous benefits:

Secures the benefits

Significantly de-risks the plan

Reduces funding costs significantly

Higher yielding bond portfolio than CLI + DDM

Provide adequate and timely liquidity to fund B+E

Reduces volatility of funded ratio and contributions

Buys time for performance assets (Alpha) to grow unencumbered

No interest rate risk since LBP is funding future values (benefit payments)

A major benefit of the Ryan ALM cash flow matching model is the reduction in funding costs by usually 1% per year. If we cash flow match 1-30 years of benefits = 30% cost reduction between the cost of benefits (future value) and the cost to cash flow match (present value). The CDI is skewed to A/BBB+ bonds and longer maturities to reduce funding costs. This will cause the CDI to outyield liabilities by 50-100 bps and DDM. Moreover, the CDI provides adequate and timely liquidity to fund B+E. Many, if not most, pensions do a cash sweep of all asset classes to fund current benefits + expenses. CDI will fund B+E when due which will buy time for the performance assets (Alpha) to grow unencumbered. S&P data shows that dividends reinvested > 50% of the S&P 500 growth in the last 70 years. If interest rates rise, cash flow matching can reinvest any excess cash flows at the then higher yields which will lower funding costs while bonds managed with a purely total return focus would get hurt with lower price returns.

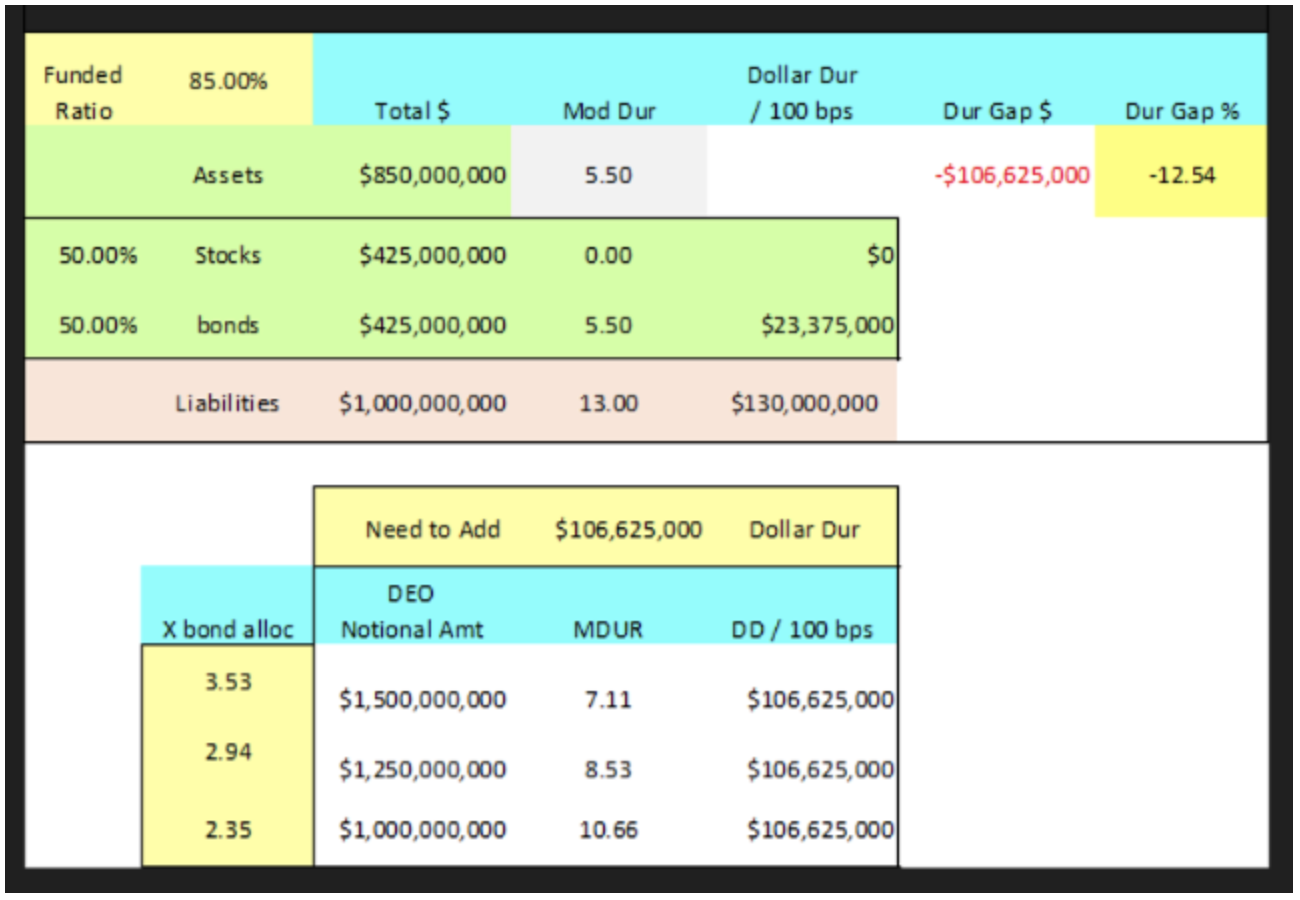

Solution: Duration Enhancing Overlay (DEO)

DDM and CDI cannot hedge 30+ year liabilities well due to the lack of bonds to buy. In a Duration Enhancing Overlay (DEO) strategy, derivatives are used to add duration. The assets in the DDM and CDI portfolios can be used as margin capital for targeted positions in interest rate swaps, swaptions or buy/sell Treasury Futures.

A Duration Enhanced Overlay (DEO) is a zero-investment strategy that can be constructed by taking long only derivatives positions like futures positions in long-dated Treasury bonds, or by taking positions in futures on long-dated treasury bonds while also taking the opposite positions in shorter term Treasury securities.

A DEO should be in addition to a CDI or DDM strategy not instead of. The issue becomes the size of the derivative contracts needed to close the duration gap. In the example below, it would take 2.2x to 3.5x the bond position to close the $ duration gap. Ryan ALM cautions against such a strategy as undue leverage but we admit the existence of a dollar duration gap.

Pension Quiz

Is it better to have 10% ROA or reduce Funding Costs by 10%? The primary objective of a pension is to secure benefits (Retired Lives) in a cost- efficient manner...

Source: Pension Quiz

Is it better to have 10% ROA or reduce Funding Costs by 10%?

The primary objective of a pension is to secure benefits (Retired Lives) in a cost-efficient manner with prudent risk. The secondary objective is to enhance the funded status by maximizing the efficiency of asset allocation. However, most pensions have the stated objective as a… target absolute % return on assets (ROA).

Achieving a 10% ROA

History has proven that achieving the ROA does not mean you achieved a fully funded plan or even enhanced the funded status such that the $ deficit and contribution costs have been reduced. Simple math can prove this assertion as shown in Exhibit 1 where pension assets achieved the ROA growth target of 8% consistently for last 6 years. Liabilities are assumed to have the same 8% growth rate (actuarial discount rate = ROA). As a result, the funded ratio stays stable at 60% but the funded status $ deficit increases by 59.6% ($40 to 63.44) which would increase contribution costs accordingly. In order for contribution costs to remain stable or go lower, assets would have to match or outgrow liabilities by 5.33% annually (13.33% ROA minimum):

Exhibit 1

Funded Ratio = 60% ($40 Deficit)

Assets and Liabilities grow at ROA = 8%

| Assets | Liabilities | Funded Status/Ratio | ||||

|---|---|---|---|---|---|---|

| Year | Begin | End | Begin | End | $ Deficit | Funded Ratio |

| 1 | $60.00 | $64.80 | $100.00 | $108.00 | $43.20 | 60% |

| 2 | 64.80 | 69.98 | 108.00 | 116.64 | 46.66 | 60% |

| 3 | 69.98 | 75.58 | 116.64 | 125.97 | 50.39 | 60% |

| 4 | 75.58 | 81.63 | 125.97 | 136.05 | 54.42 | 60% |

| 5 | 81.63 | 88.16 | 136.05 | 146.93 | 58.77 | 60% |

| 6 | 88.16 | 95.21 | 146.93 | 158.65 | 63.44 | 60% |

If the actual asset growth rate was 10% instead of 8% (Exhibit 2), assets would grow to $106.29 over six years which creates a 67% funded ratio but a growing deficit of $52.36 or 30.9% greater than the initial $40 underfunding which increases contribution costs accordingly. Even a 70% funded ratio would increase the deficit to $45.91 or 14.78% greater. The pension return objective should be for assets to outgrow liabilities in economic dollars not actuarial dollars… it is relative $ returns that count not an absolute % return (ROA)! It is the economic funded status that counts not the funded ratio! Asset allocation needs to know the economic relative return needed to enhance the economic funded status.

Exhibit 2

Funded Ratio = 60% ($40 Deficit)

Assets grow at 10% but Liabilities grow at ROA = 8%

| Assets | Liabilities | Funded Status/Ratio | ||||

|---|---|---|---|---|---|---|

| Year | Begin | End | Begin | End | $ Deficit | Funded Ratio |

| 1 | $60.00 | $66.00 | $100.00 | $108.00 | $42.00 | 61% |

| 2 | 64.80 | 72.60 | 108.00 | 116.64 | 44.04 | 62% |

| 3 | 69.98 | 79.86 | 116.64 | 125.97 | 46.11 | 63% |

| 4 | 75.58 | 87.85 | 125.97 | 136.05 | 48.19 | 65% |

| 5 | 81.63 | 96.63 | 136.05 | 146.93 | 50.30 | 66% |

| 6 | 88.16 | 106.29 | 146.93 | 158.65 | 52.36 | 67% |

If we use market (economic) values for liabilities (ASC 715 discount rates), liabilities become highly interest rate sensitive… the economic truth. Using ASC 715 (AA corporates as a zero-coupon yield curve) as the discount rate for liabilities, a small increase in interest rates (+60 bp per year) would create negative growth in liabilities! Accordingly, any positive growth in assets would enhance the economic funded ratio and funded status. In just five years a 60% funded ratio could be 91% funded with just 5% asset growth while a 70% funded ratio would be 106% funded… and at no time did assets earn the ROA!

5-year Horizon

Liabilities ASC 715 Discount rate goes from 2.00% to 5.00%

Liabilities Growth Rate = (3.40%) at 12-year duration

| ----- Annual Growth Rate ----- | |||

|---|---|---|---|

| Assets | 5.00% | 6.00% | 7.00% |

| Liabilities | -3.40% | -3.40% | -3.40% |

| Alpha (Annual) | 8.40% | 9.40% | 10.40% |

| Funded Ratio @ 60% ... | 91.0% | 94.5% | 100.1% |

| @ 70% ... | 106.2% | 111.4% | 116.7% |

Achieving a 10% Funding Cost Savings

The primary objective of a pension is to fund liabilities in a cost-effective manner. It is a liability objective with cost considerations. Since 1999, most pensions have been hard hit by spiking contribution costs which were unexpected and not a budget forecast. For many plan sponsors, the contribution cost has risen as much as 5x to 10x from the fiscal 1999 level. Such costs are a product of the size of the funded status deficit where asset $ growth did not match liability $ growth over time. Indeed, it is the relative $ growth of pension assets vs. liability $ growth that is critical… not the absolute % return on pension assets.

The pension objective is best achieved by separating the assets into liquidity (Beta) and growth (Alpha) assets. The job of the liability Beta (liquidity) assets is to secure benefits (Retired Lives) in a cost-efficient manner with prudent risk. This is best accomplished through cash flow matching net liabilities chronologically. Ryan ALM has built a liability cash flow matching product, named the Liability Beta Portfolio™ (LBP), as a cost optimization model that matches and funds the net liability benefit payment schedule (minus contributions) at the lowest cost given the investment policy restrictions of our clients.

Since liabilities are funded initially by contributions, using the LBP model to cash flow match net liabilities chronologically may be able to fund more liabilities than you think. Assume that a 15% bond allocation could cash flow match the next 10 years of net Retired Lives payments chronologically. Based on the Ryan ALM Liability Beta Portfolio™ (LBP) model we show a cost savings of about 8% to 15% on cash flow matching the first 10 years of liabilities versus the ASC 715 discount rates (AA corporate zero-coupon bonds). For every $100 million in bonds used in our LBP model could save about $10 million or 10% in funding cost savings vs. the projected net liabilities. This cost savings is received immediately upon implementation of the Liability Beta Portfolio™ rather than over several years as forecasted returns suggest would happen, if at all. This is a serious cost reduction that reduces the volatility of the funded status and contributions and should be a major consideration of any pension asset allocation as the core portfolio.

Matching liabilities chronologically should also buy time for the growth assets (Alpha assets) to perform and outgrow liabilities without being diluted or unencumbered to partially fund liabilities as is the case so often today. Given time (10 years) most non-bond asset classes tend to outperform bonds. Since liabilities behave like bonds there is a high probability that Alpha assets (i.e. equities) could outperform liability growth over an extended time horizon especially at today’s low yield on bonds (and liabilities).

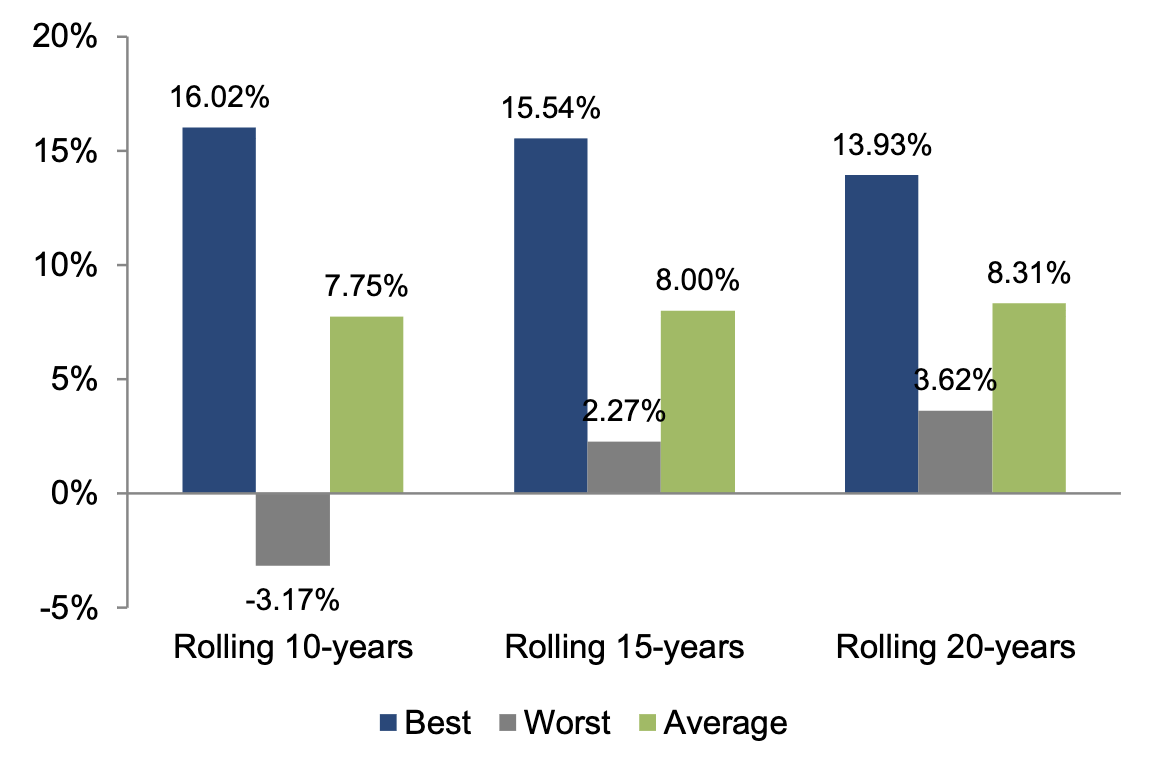

Given time, equities (S&P 500) perform well. The more time you give equities… the better the returns. Below are historical average S&P 500 return measurements for rolling 10-year, 15-year and 20-year periods ending 12/31/19 over a 50-year horizon starting 1969. The table shows an average return of 7.75% for rolling 10-years, 8.00% for rolling 15-years and 8.31% for rolling 20-years. The table below also suggests how difficult it is to average a 10% return for any extended period of time… even 9.00% is not a proven performance attainment:

Best, worst, and average returns

Solution: BUY TIME!

So how do you buy time? The answer is… cash flow match liabilities

How do you buy time? Cash flow match liabilities for the time you need.for the time you need. We recommend funding net Retired Lives out 10-years or more chronologically as the historical equity returns document. Our cash flow matching model (Liability Beta Portfolio™ or LBP) will calculate with precision the cost to fund net liabilities + expenses in a cost-effective manner chronologically.for the time you need. We recommend funding net Retired Lives out 10-years or more chronologically as the historical equity returns document. Our cash flow matching model (Liability Beta Portfolio™ or LBP) will calculate with precision the cost to fund net liabilities + expenses in a cost-effective manner chronologically.

Benefits: Cash Flow Matching

Our LBP also has numerous benefits that enhance the pension plan:

Secures Benefits

Cash flow match monthly Retired Lives benefits chronologically

Reduces Costs

LBP reduces Contribution, Funding and Asset Management Costs:

(LBP Fee = 15 bps… much less than most active bond managers)

Reduces Volatility

Reduces volatility of Contributions and Funded Ratio

Reduces Risk

Risk = Uncertainty of Funding Benefit Payments

(LBP funds benefits with certainty)Projected Benefit Payments are Future Values

(FV have NO Interest Rate Sensitive)

Enhances ROA

LBP should out yield most active management bond portfolios

Buys Time

LBP matches & funds liabilities chronologically

Moves deficit out longer extending the investment horizon

Buys Time for Non-bond assets (Alpha assets) to grow

No dilution of Alpha assets to fund benefits

However, most bond allocations are for active bond management versus a generic index benchmark(s). As the designer of the Lehman bond indexes from my days as the Director of Fixed Income Research at Lehman, I can tell you unequivocally that generic bond indexes look nothing like a projected pension benefit payment schedule. Such a mismatch will distort the cash flows and risk/reward behavior of assets vs. liabilities. The major issues and differences are:

Bond Assets Managed Versus Generic Bond Indexes

Does not fund benefits + expenses

Aggregate Index = low yielding @ 1.42%

Generic bond index =/= plan sponsor’s liabilities

Cash flows do not match plan sponsor’s liabilities

Index skewed to long bonds + Government securities

Performance (value added) = small to none (after fees)

But the worst difference and discrepancy is… all about cash flows. Active bond management is usually focused on outperforming the returns of a generic bond index benchmark. As a result, cash flows are not a consideration. But no matter what generic bond index is chosen; the fixed income assets cannot produce enough income cash flow to fund benefits + expenses. As a result, bonds will require help from performance (Alpha) assets to fund benefits + expenses. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the core portfolio to fund the shorter Retired Lives net liabilities (1-10 years), the Alpha assets are now free to grow long-term without being diluted or unencumbered to pay any benefits. The example below shows the cash flow difference of bonds managed to a generic index versus cash flow matching to liabilities:

It’s All about Cash Flows!

Bond allocation = $150 million

Liabilities (Net Benefits + Expenses) = $20 million per year

Bond management vs. generic bond index

YTM = 2.50%

Income Cash flow = $3.75 million annual ($2.50% x $150m)

Annual cash flow shortfall= $16.25 million ($20m - $3.75m)

Requires dilution of Alpha assets cash flow to fully fund liabilities

Cash Flow Matching next 10 years

YTM = 3.50% (skewed to A/BBB corporate bonds)

Cash flow = $20 million annual (fully funds liabilities)

(Cash flow includes principal + income + income reinvested)

No dilution of Alpha assets (allowed to grow unencumbered)

Observations:

Generic bond indexes cash flows look nothing like the projected benefit payment schedule of a pension

This leads to mismatch of cash flows and risk/reward behaviors … serious issue over time

Alpha assets need time to perform without any dilution of their cash flows to pay benefits

Cash flow matching (Beta assets) matches plus funds benefit payments chronologically

Cash flow matching will out yield current bond managers and enhance ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Let the performance (Alpha) assets perform (grow) as the liquidity (Beta) assets provide cash flow sufficient to fund net benefits plus expenses. Pension consultants and plan sponsors should consider installing an LBP as the core portfolio in asset allocation. The best value in bonds is the certainty of their cash flows. Bonds are usually not considered performance assets especially vs. pension liabilities which behave like bonds. As the Alpha assets perform vs. liability growth, enhancing the funded ratio, such excess returns could be transferred over to the Liability Beta Portfolio™ (LBP) to fund and de-risk more liabilities… Portable Alpha. Had this Portable Alpha discipline been in place during the 1990s when funded ratios grew to their highest historical levels with true surpluses… there would be no U.S. pension crisis today!

Conclusion (Logic)

So, is it better to have a 10% cost savings that is immediate and certain with numerous benefits itemized in this report? Or is it better to have an uncertain 10% ROA in the future that may or may not enhance funding (could increase the deficit)?

10% cost savings = $100 million reduced funding costs per $1 billion

10% ROA = 60% funded ratio on $1b = $400m deficit that grows to $522.60m in 6 years or 30.7% higher contribution costs = $122.6m.

Compare: $122.6m more in costs vs. $100m cost savings!!!

I think the facts speak clearly that… cost savings is the better goal and better fit with the primary objective of a pension… but you can have both:

To achieve the primary and secondary pension objective:

Primary = cash flow match net Retired Lives chronologically (Beta assets)

Secondary = have asset growth > liability growth not % ROA (Alpha assets)

The Risk/Reward of Bonds

Unlike any other asset class, fixed income (bonds) has two risk/reward values: Total Return Certain Cash Flows Total Return Value The total return value in bonds is the converse of...

Source: The Risk/Reward of Bonds

Unlike any other asset class, fixed income (bonds) has two risk/reward values:

Total Return

Certain Cash Flows

Total Return Value

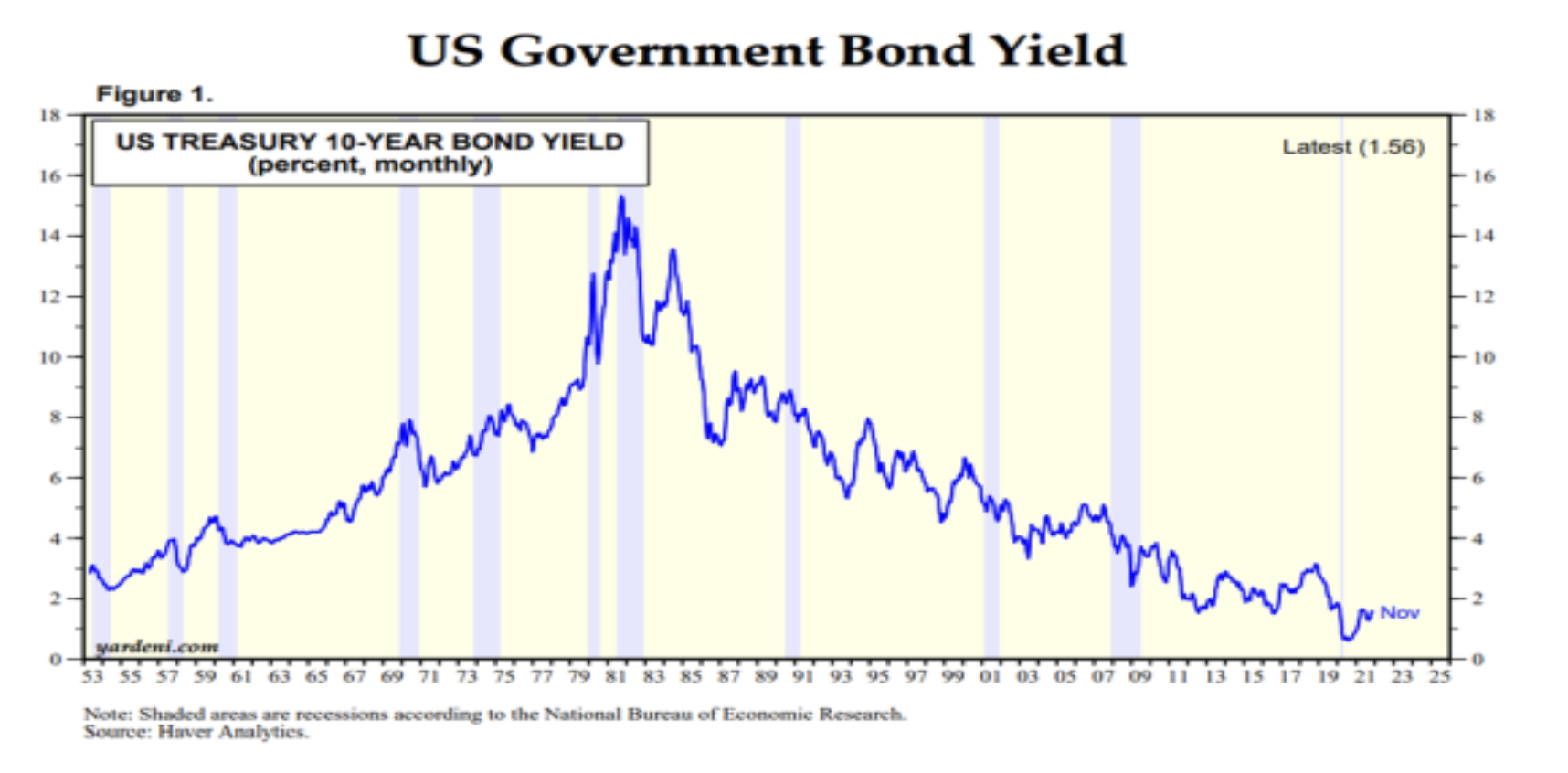

The total return value in bonds is the converse of interest rate movements. When rates go down, as they have from 1981 to 2021, they produce price appreciation and higher total returns. And the opposite happens (negative price returns) when rates go up as they did from 1953 to 1981.

Since the start of 2022, interest rates have trended upward causing negative bond returns (BB Aggregate Index -3.25% YTD thru 02/28/22). Given the current inflation rate of over 7.0% on the CPI and over 9.0% for the PPI, coupled with the expectation that the Fed will raise short rates several times this year… this interest rate trend to higher rates should continue. As a result, pensions should expect negative fixed income returns this year and for the foreseeable future.

Certain Cash Flow Value

If you buy bonds for their intrinsic value (certainty of cash flows) you will immunize or mitigate interest rate risk! Since cash flows are future values, they are not affected by interest rate movements.Moreover, any excess cash flow reinvested will be able to buy new cash flows at reduced costs. This is truly the value in bonds and we strongly recommend that pensions use bonds as their liquidity or Beta assets. Let the performance or Alpha assets be the non-bond assets. Use bonds to cash flow match pension benefits and expenses chronologically. This synergy of Beta and Alpha assets should secure benefits, reduce funding costs, and buy time for the Alpha assets to grow unencumbered.

Cash flow matching by any name (defeasance, dedication, immunization) may be the oldest fixed-income strategy. It should be the core portfolio of a pension and the fixed income strategy chosen by pensions today given the likelihood of higher interest rates. Cash flow matching will secure benefits in a cost-efficient manner. The Ryan ALM cash flow matching product (Liability Beta Portfolio™) will reduce funding costs by about 1% per year of matching (i.e. 1-10 years = 10% funding cost reduction).

With the stock market struggling this year (S&P 500 -10.7% YTD thru 03/07/22), a cash flow matching bond allocation will buy time for the equity allocation to recover without any dilution to fund benefits and expenses. Let bonds be the liquidity assets to fund benefits + expenses. Let the growth assets grow unencumbered without any dilution. History tells us that 48% of the S&P 500 returns on a rolling 10-year basis come from dividends reinvested.

Pension Solutions Series Part 2 - Liability Beta Portfolio™ (LBP)

Pension Solution: Liability Beta Portfolio™ (LBP) The primary pension objective is to secure promised benefits (Retired Lives) in a cost- effective manner (stable to lower contribution costs) with prudent risk...

Source: Pension Solutions Series Part 2 - Liability Beta Portfolio™ (LBP)

Pension Solution: Liability Beta Portfolio™ (LBP)

The primary pension objective is to secure promised benefits (Retired Lives) in a cost-effective manner (stable to lower contribution costs) with prudent risk. This is best accomplished through cash flow matching.

Cash Flow Matching

Since benefits (liabilities) are future value numbers, it is consistent and necessary to match the future value of assets to the future value of liabilities. This is better said as cash flow matching asset cash flows to liability cash flows… cash flow driven investments (CDI). Since bonds are the only asset class with a known future value, it has been the obvious choice to cash flow match liabilities. Indeed, this is the true value of fixed income assets. In truth,cash flow matching the liability benefit payment schedule (liability cash flow) isthe ideal way to de-risk a pension plan. Since projected benefits (future values) are not interest rate sensitive, cash flow matching projected benefits eliminates the biggest risk in bonds… interest rate sensitivity.

Since contributions are the initial source to fund liabilities, current assets fund net liabilities (benefits – contributions). It is critical that current assets know what they are funding… net liabilities! Fixed income assets are best cash flow managed versus Retired Lives, which are the most certain and imminent liabilities. Active Lives tend to be the most uncertain cash flows (actuarial noise). Matching Retired Lives net liabilities chronologically is wise and recommended as it not only secures benefits over a certain time horizon, it buys time for the non-bond assets (Alpha assets) to perform and outgrow Active Lives liabilities. It would not be prudent to use volatile, risky assets to fund the shorter Retired Lives liabilities… too uncertain.

Ryan ALM has developed a cash flow matching model called the Liability Beta Portfolio™ (LBP). Our LBP is a cost optimization model that matches and funds Retired Lives monthly benefit payments chronologically at the lowest cost to the plan sponsor. Our LBP should reduce funding costs by 8% to 10% vs. 1-10 years Retired Lives. The true value in bonds is the certainty of their cash flows. We urge plan sponsors to transfer current active fixed income management from generic index benchmarks to our LBP to de-risk the plan gradually and reduce costs.

Asset Allocation

Asset allocation would be wise to separate Retired Lives from Active Lives and liability Beta assets from liability Alpha assets. We recommend using bonds cash flow matched to Retired Lives chronologically as the liability Beta assets and use Alpha assets (risky assets) for the Active Lives. The funded ratio should dictate the allocation to bonds. The higher the funded ratio: the higher the allocation to liability Beta assets. The pension plan’s current allocation to bonds should determine how much of the net liabilities bonds can cash flow match (i.e. 15% bond allocation might fund the next seven to 10-years of Net Retired Lives). By switching from traditional bond management and generic bond indexes to a Custom Liability Index coupled with a Liability Beta Portfolio will produce many benefits to the pension plan:

1. Reduce Funding Costs

The Liability Beta Portfolio should be the core portfolio since it best represents the true pension objective… securing benefits in a cost-effective manner. Our LBP will reduce funding costs by 8% to 10% in funding 1-10 years of Retired Lives. The true quest of any pension or liability driven objective is to reach and maintain a fully funded liability cash flow matched asset position. This can only be achieved with a cash flow matching bond portfolio. Any other asset class does not match the behavior of liabilities and creates the roller coaster effect of victories (surplus) and losses (deficits).

2. Reduces Volatility in Funded Ratio

If you match liabilities then you match the risk/reward behavior of the present value of liabilities. This eliminates the roller coaster effect that most plans have in their Funded Ratio due to a mismatching of assets vs. liabilities. This erratic growth difference between assets vs. liabilities plays havoc with budgets (i.e. Contributions), benefit decisions and financial statements.

3. Reduces Contribution Volatility and Cost

If you match liabilities then the funded ratio is less volatile which in turns means that contribution costs become less volatile. Our LBP will also outyield liabilities thereby creating some Alpha which will reduce Contribution costs.

4. Reduces Interest Rate Risk

Benefit payments are future value amounts which are not interest rate sensitive. By cash flow matching future values, we have neutralized interest rate risk.

5. Reduces Bond Asset Management Fees

The Ryan ALM Liability Beta Portfolio (LBP) has a low fee which should save clients about 50% on bond asset management fees.

6. Buys Time for Alpha assets

The LBP will match and fund Retired Lives chronologically. If the LBP funds 1-10 years of Retired Lives it buys 10-years of time for the Alpha assets to grow and perform. History tells us that risky assets do better the more time you give them to perform.