Pension Alert: Spread between ROA and Bonds Narrowest in 20+ Years

Source: Pension Alert: Spread between ROA and Bonds Narrowest in 20+ Years

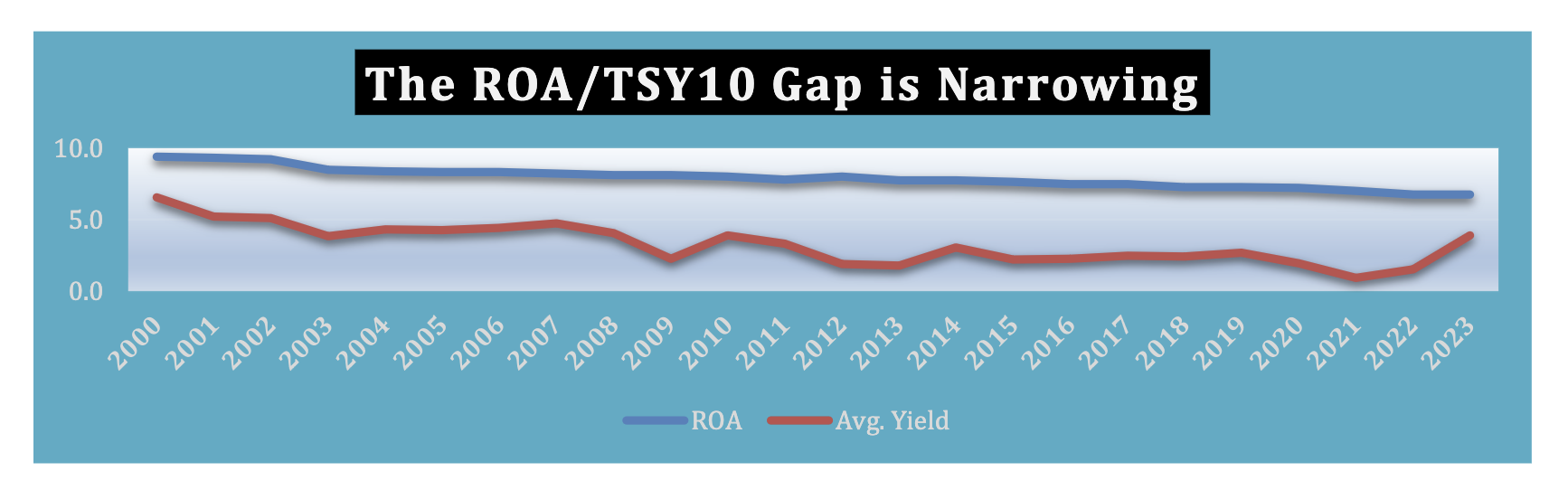

Most Asset Allocations for pensions are based on achieving the ROA. The ROA is an annual forecast of asset returns. Each asset class is assigned a ROA then weighted by the target allocation to get an average or target ROA. Currently, the ROA for most Public pensions is around 6.75%. This is in sharp contrast to the history of reported discount rates (ROA) for funding purposes as reported in the Milliman Public Funding Surveys.

| Year | ROA (%) | Year | ROA (%) | Year | ROA (%) | Year | ROA (%) | Year | ROA (%) |

|---|---|---|---|---|---|---|---|---|---|

| 2000 | 9.4 | 2005 | 8.3 | 2010 | 8.0 | 2015 | 7.7 | 2020 | 7.2 |

| 2001 | 9.3 | 2006 | 8.3 | 2011 | 7.8 | 2016 | 7.5 | 2021 | 7.0 |

| 2002 | 9.2 | 2007 | 8.2 | 2012 | 8.0 | 2017 | 7.5 | 2022 | 6.75E |

| 2003 | 8.5 | 2008 | 8.1 | 2013 | 7.8 | 2018 | 7.3 | 2023 | 6.75E |

| 2004 | 8.4 | 2009 | 8.1 | 2014 | 7.8 | 2019 | 7.3 |

Sources: Milliman Public Funding Surveys

Ryan ALM estimates for 2022 + 2023

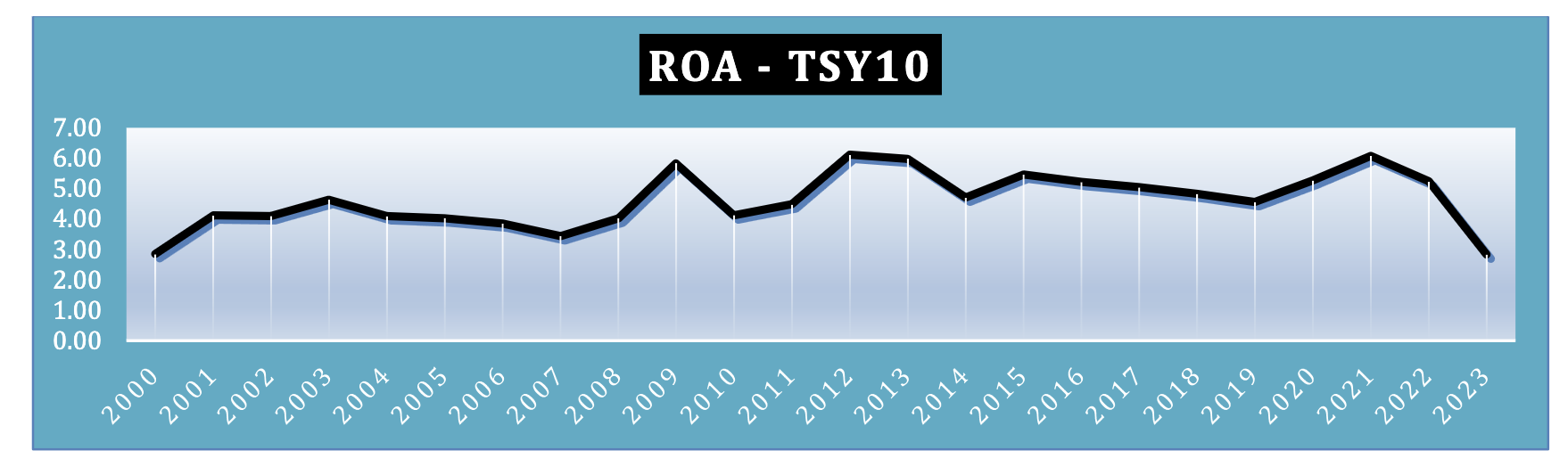

As the Milliman Surveys show, the reported ROAs as discount rates for Public pension liabilities has trended downward from a high of 9.40% in 2000 to somewhere around 6.75% today. Corporate pensions are under ASC 715 discount rates (AA corporate zero-coupon yield curve) and have been reflective of market rates which are consistently much lower than the ROA discount rates. Plotting the ROA discount rates for Public pensions versus the history of 10-year Treasury rates (source: Ryan Treasury Indexes) shows that the yield difference is now at a 22-year low of around 283 basis points (as of 12/31/22). This trend would support a greater allocation to fixed income.

Ryan ALM Advisers uses and promotes A and BBB corporate bonds to cash flow match and defease clients projected liabilities. As a result, the yield spread versus the ROA gets even narrower. The current yield spreads for 10-year corporate bonds versus the 10-year Treasury are:

AA +56 bps

A +75 bps

BBB +114 bps

Using an average yield spread versus the 10-year Treasury for A/BBB corporate bonds = 95 basis points would narrow the ROA – Corporate Bond Yield Spread to 187 basis points. This suggests that fixed income can provide 72% of the target ROA. More importantly, using A/BBB corporate bond portfolio would outyield the BB Aggregate index (bond ROA) by around 75-100 basis points. The BB index YTW levels prove this point:

12/31/22 1/17/23

BB Aggregate = 4.68% 4.32%

BB Corporates = 5.42% 5.03%

Benefits of Higher Bond Allocation to Cash Flow Matching:

Improve Liquidity

Reduce Volatility (risk)

Outyield Index Benchmark and bond ROA

Create CORE portfolio as anchor to earning ROA

Reduce costs to fund Benefits + Expenses (B + E)

Buy TIME for performance assets to grow unencumbered