Ryan ALM

White Papers

Browse

The Risk/Reward of Bonds

Unlike any other asset class, fixed income (bonds) has two risk/reward values: Total Return Certain Cash Flows Total Return Value The total return value in bonds is the converse of...

Source: The Risk/Reward of Bonds

Unlike any other asset class, fixed income (bonds) has two risk/reward values:

Total Return

Certain Cash Flows

Total Return Value

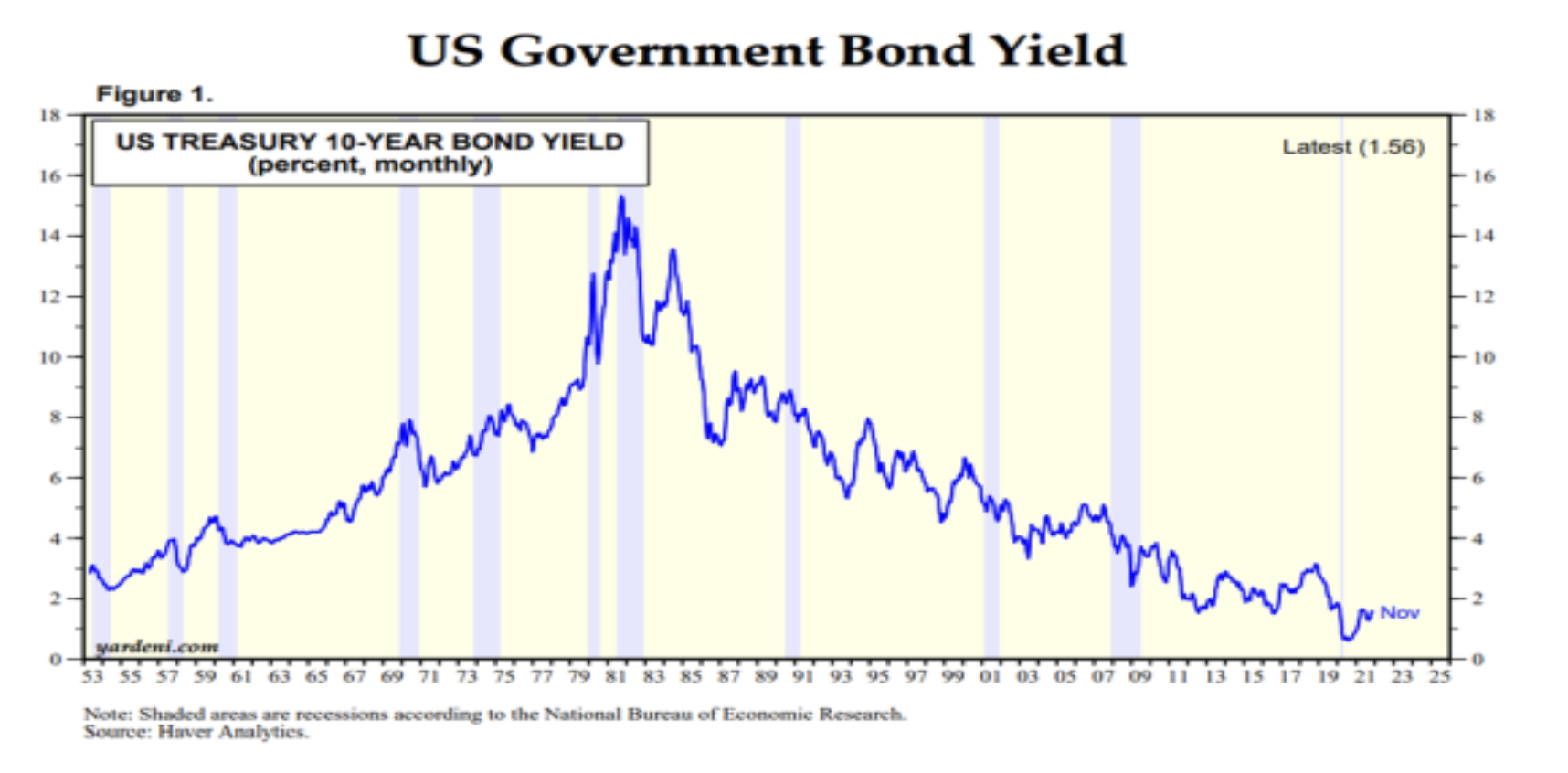

The total return value in bonds is the converse of interest rate movements. When rates go down, as they have from 1981 to 2021, they produce price appreciation and higher total returns. And the opposite happens (negative price returns) when rates go up as they did from 1953 to 1981.

Since the start of 2022, interest rates have trended upward causing negative bond returns (BB Aggregate Index -3.25% YTD thru 02/28/22). Given the current inflation rate of over 7.0% on the CPI and over 9.0% for the PPI, coupled with the expectation that the Fed will raise short rates several times this year… this interest rate trend to higher rates should continue. As a result, pensions should expect negative fixed income returns this year and for the foreseeable future.

Certain Cash Flow Value

If you buy bonds for their intrinsic value (certainty of cash flows) you will immunize or mitigate interest rate risk! Since cash flows are future values, they are not affected by interest rate movements.Moreover, any excess cash flow reinvested will be able to buy new cash flows at reduced costs. This is truly the value in bonds and we strongly recommend that pensions use bonds as their liquidity or Beta assets. Let the performance or Alpha assets be the non-bond assets. Use bonds to cash flow match pension benefits and expenses chronologically. This synergy of Beta and Alpha assets should secure benefits, reduce funding costs, and buy time for the Alpha assets to grow unencumbered.

Cash flow matching by any name (defeasance, dedication, immunization) may be the oldest fixed-income strategy. It should be the core portfolio of a pension and the fixed income strategy chosen by pensions today given the likelihood of higher interest rates. Cash flow matching will secure benefits in a cost-efficient manner. The Ryan ALM cash flow matching product (Liability Beta Portfolio™) will reduce funding costs by about 1% per year of matching (i.e. 1-10 years = 10% funding cost reduction).

With the stock market struggling this year (S&P 500 -10.7% YTD thru 03/07/22), a cash flow matching bond allocation will buy time for the equity allocation to recover without any dilution to fund benefits and expenses. Let bonds be the liquidity assets to fund benefits + expenses. Let the growth assets grow unencumbered without any dilution. History tells us that 48% of the S&P 500 returns on a rolling 10-year basis come from dividends reinvested.

Response to: Presidential Memo on Pensions

Response to: Presidential Memo on Pensions Mr. President, I applaud your memo of October 22 to the Secretaries of Treasury, Commerce and Labor. You gave them an order to review...

Source: Response to: Presidential Memo on Pensions

Response to: Presidential Memo on Pensions

Mr. President,

I applaud your memo of October 22 to the Secretaries of Treasury, Commerce and Labor. You gave them an order to review the Delphi pension matter and inform you “within 90 days of this memorandum of any appropriate action that may be taken, consistent with applicable law to (i) address affected Delphi retirees’ lost pension benefits and (ii) bring transparency to the decision to terminate the plan. This review shall include an evaluation of the feasibility of enacting legislation.”

The solution you are looking for can be found in the Butch Lewis Act (BLA) passed by the House through a bipartisan vote (all Democrats + 29 Republicans) on July 26, 2019 as H.R. 397. It has been awaiting approval by the Senate since then. The BLA would create a new agency under the Treasury Department called the Pension Rehabilitation Administration (PRA). The PRA would provide low-interest-rate loans to critical and declining multi-employer pensions at the 30-year Treasury rate plus a profit margin (@ 0.25%). The BLA would provide 100% payment of all retirees benefits in sharp contrast to the PBGC limit of $12,870 for a 30-years of services retiree ($35.75 x 12 months x years of service). The Council of Budget Office estimates the cost of the BLA at $34 billion (if no loans are repaid), which can be minimized by the fact that all PRA loans come with a profit margin. Even at $34 billion it is a small burden compared to the potential cost to cover 1.4 million workers’ pensions affected by the current pension crisis. The PBGC is not the answer… but the BLA is. I urge you to have the Senate approve the BLA legislation that is awaiting their approval for over 15 months now. Time is of the essence!

God Bless Pension America!