Ryan ALM

White Papers

Browse

When is a Pension Fully Funded?

The Funded Ratio tends to be the acid test and benchmark for funded status… but is it? We have written several research white papers (www. RyanALM/Research/White Papers) about the glaring...

Source: When is a Pension Fully Funded?

The Funded Ratio tends to be the acid test and benchmark for funded status… but is it? We have written several research white papers (www. RyanALM/Research/White Papers) about the glaring issues with the Funded Ratio. Here are just a few of the inconsistencies with the Funded Ratio:

Actuarial Value versus Market Value

The Funded Ratio (FR) of a pension is usually based on the actuarial value of assets / actuarial value of liabilities. The Funded Status (FS) is the actuarial value of assets – actuarial value of liabilities. Actuarial values are different than market values… sometimes quite different. Market values are the better measurement of economic reality since you can’t spend actuarial dollars. As a result, this valuation difference can seriously distort the FR and FS calculation.

Present Value versus Future Value

Notably, the FR and FS are present value calculations. But pension liability cash flows (benefits + expenses (B+E)) are future value (FV) projections. Since the FV of most assets is not known this becomes a true pension conundrum. Bonds are the only asset class with a known and certain future value. That is why bonds have been the chosen asset class for defeasance, immunization and cash flow matching for several decades. The disconnect between PVs and FVs haunts pensions. The true objective of a pension is to secure and fully fund liability cash flows in a cost-efficient manner with prudent risk. As a result, the objective should be for asset cash flows to match and fully fund liability cash flows.So, when is a pension fully funded... when asset cash flows (future values) fully fund liability cash flows (future values). This is best accomplished thru cash flow matching and is best measured by the Asset Exhaustion Test.

Contributions = MIA

The FR and FS both ignore contributions as an asset. The truth is that contributions are future assets and should be a high consideration in any asset liability management (ALM). We recommend using the Ryan ALM modified Asset Exhaustion Test (AET) as the best way to measure the solvency and funding status of a pension. We take asset cash flows (based on a ROA) and compare them to NET liability cash flows (benefits + expenses – contributions) to understand if assets can fully fund the liability cash flows. We use a matrix of ROAs to determine what ROA is the best fit. This calculated ROA is in sharp contrast to the current ROA that is based on an asset allocation model that ignores the FR and FS. It is common that a pension plan with a 60% funded ratio and another funded at 90% have the same or similar ROA. How is this possible? Shouldn’t the 60% funded plan need assets to work harder? Yes, but that does not have anything to do with the current ROA calculation. Whatever shortfall there is in asset cash flows to fund liability cash flows (B+E) must be paid by higher contributions… this is not in the best interests of a pension plan and the sponsor’s budget. Clearly, the current ROA is not a calculated return based on the FR and FS that will guarantee a fully funded

status if achieved long-term… nor will it guarantee that contributions will go down. This has been a sad and costly trend for the last 25+ years.

Discount Rates

A most troubling issue is what discount rate to use. FASB and GASB tend to disagree on this.

FASB = high quality AA corporate zero-coupon yield curve

GASB = ROA

Since the ROA is a much higher rate (usually 100 to 200 bps) then liabilities would be priced at a much lower PV (12% to 24%). This would enhance the FR by 8% to 22%. Market rates are best in determining the market or economic value of liabilities. FASB 144 says it well:

“The objective of selecting assumed discount rates is to measure the single amount that, if invested at the measurement date in a portfolio of high-quality debt instruments, would provide the necessary future cash flows to pay the pension benefits when due. Notionally, that single amount, the projected benefit obligation, would equal the current market value of a portfolio of high-quality zero coupon bonds whose maturity dates and amounts would be the same as the timing and amount of the expected future benefit payments. The determination of the assumed discount rate is separate from the determination of the expected rate of return on plan assets”

Ryan ALM Solutions:

Custom Liability Index (CLI): The first step in prudent pension management is to calculate the liability cash flows that assets must fund. This should be a net liability cash flow (benefits + expenses – contributions). Until liabilities are monitored and priced as a Custom Liability Index (CLI) the asset side is in jeopardy of managing to the wrong objectives (i.e. ROA and generic market indexes). Only a CLI best represents the unique liability cash flows of a plan sponsor. Just like snowflakes, no two pension liability schedules are alike due to different labor forces, salaries, mortality and plan amendments. How could a static ROA or genericmarket indexes ever properly represent the risk/reward behavior of such a diverse array of pension liabilities? Once the CLI is installed, the pension can now know the true economic Funded Ratio and Funded Status which should dictate the appropriate Asset Allocation, Asset Management and Performance Measurement.

Asset Exhaustion Test (AET): GASB requires a test of solvency (AET) to document that the asset cash flows (at the ROA) will fully fund the net liability cash flows (benefits + expenses – contributions). GASB correctly understands that assets are funding net liabilities after contributions… and that contributions are future assets. This net liability is rarely focused on by the asset side in asset allocation. Ryan ALM enhances the asset exhaustion test by calculating the ROA that will fully fund net liability cash flows. Usually, we find that a lower ROA can accomplish this goal and is a better fit than the current ROA. This would suggest a more conservative asset allocation and a heavier allocation to fixed income to defease liability cash flows chronologically. This is a common and serious issue. This calculated ROA should be the asset allocation model focus. We urge all pensions to incorporate this modified AET before acting on asset allocation.

Liability Beta Portfolio™ (LBP):The intrinsic value in bonds is the certainty of its cash flows. That is why bonds have been used for decades to defease liability cash flows. The core or Beta portfolio for a pension should be in investment grade bonds that cash flow match and fully fund liabilities chronologically thereby buying time for the growth (Alpha) assets to outgrow liabilities and erase the deficit. The proper Beta portfolio for any liability objective should be… a Liability Beta Portfolio™. Ryan ALM has developed a LBP which will cash flow match liabilities chronologically and reduce funding costs by about 2% per year (1-10 years = 20%) as well as reduce the volatility of the Funded Status and contribution costs. The LBP should be the core portfolio of any pension and replace active fixed income management. By matching and funding liabilities chronologically, the LBP buys time for the growth or Alpha assets (non-bonds) to perform. By working in harmony with the Alpha assets the plan can gradually enhance its funded status and reduce contribution costs.

Liability Alpha Assets: The non-bond assets should be managed vs. the CLI to exceed liability growth (earn liability Alpha) and enhance the economic Funded Status. The goal here is outgrow liabilities in $s (relative returns) by enough to erase the deficit over a time horizon equal to the average life (duration) of liabilities (calculated by the CLI). As the Alpha assets achieve the required annual Alpha, any excess returns vs. liability growth should be ported over to the Liability Beta Portfolio™ to secure the victory. Had this been in place during the decade of the 1990s when pensions had surpluses… there would be no pension deficits today.

Bond Yields… Caveat Emptor

Most bonds are priced and traded on some yield calculation. These yield calculations are based on assumptions that are difficult, if not impossible, to achieve. For example: Yield to Maturity...

Source: Bond Yields… Caveat Emptor

Most bonds are priced and traded on some yield calculation. These yield calculations are based on assumptions that are difficult, if not impossible, to achieve. For example:

Yield to Maturity (YTM) assumes you will reinvest every six months at the purchase YTM until maturity of the bond. How could this happen? Yields are changing every day, and will you reinvest exactly every six months into the same maturity and same YTM? Sounds like Mission Impossible! In fact, the reinvestment rate on any bond is based on the total return of what you reinvested into. Yes, it is possible to have a negative reinvestment rate if you reinvested into a security with a negative total return. Moreover, the longer the bond maturity… the more the reinvestment rate of return determines the yield or return to maturity. In truth, the basic value of the YTM is to determine a price for the security.

All other yields (yield to call, yield to average life, yield to worst, etc.) are based on assumptions that are most difficult to occur, if not impossible. The intrinsic value of most bonds is the certainty of their cash flows. This is what the smart investor should focus on and utilize. Remove the uncertainty that is embedded in all bond yield calculations. Bonds are the only asset class with this certainty of their cash flows. That is why bonds have been the logical choice for Dedication and Defeasance using Cash Flow Matching (CFM) strategies since the 1970s. Only CFM is a best fit for any liability driven objective (Endowments & Foundations, Lotteries, Pensions, OPEB, etc.). The primary objective of a pension is to secure benefitsin a cost-efficient manner with prudent risk. CFM will secure and fully fund benefits by asset cash flows matching and fully funding monthly liability cash flows chronologically for as far out as the plan sponsor deems necessary.

We believe that a best practice is to separate liquidity assets (liability Beta assets) from growth assets (liability Alpha assets). The Beta assets should be the bond allocation to cash flow match the net liability cash flows (after contributions) chronologically for a target horizon (we recommend 10 years). This will provide the time for risky assets (Alpha) to grow unencumbered since you have the certainty of the Beta assets cash flows for as long a period as you want. It would also be wise to take the Cash and Fixed Income allocation and apply it to a CFM allocation. Several pension plans do a cash sweep of all assets’ income to fund the monthly benefits and expenses. A study of S&P 500 data by Guinness Global has determined that dividends and dividends reinvested account for about 47% of the S&P 500 total return on rolling 10-year periods and 57% for 20-year time horizons. So why would you want to dilute equity returns by spending the dividend income? Let the cash + bond allocation fund the current monthly liability cash flows through our CFM model (Liability Beta Portfolio™ or LBP). Our LBP would match and secure benefits chronologically for as far out as the allocation of funds allows. Since we are dealing with net liabilities (after contributions) a 15% LBP allocation may fund liabilities out to 10-years. The Ryan ALM cash flow matching model is well tested showing a funding cost savings of about 2% per year or more for longer maturity programs (20% for 1-10 years) depending on the liability term structure.

The Ryan ALM LBP model is funding benefits (future values) which are not interest rate sensitive. This eliminates the largest risk in bonds. Our LBP model will usually outyield active bond managers by over 50 bps, which will also reduce costs.

Observations and Benefits of LBP:

No change in Cash and Bond allocation

No dilution of Alpha assets to fund B + E

Reduces funding costs by about 2% per year

Mitigates interest rate risk (funding future values)

Secures + fully funds monthly B+E chronologically

Eliminates the need for a cash sweep which dilutes equity returns

LBP will out yield current bond managers and enhance the ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Logic

Let the performance assets (Alpha assets) perform by growing unencumbered as the liquidity assets (Beta assets) provide cash flow sufficient to fully fund benefits plus expenses chronologically.

Ryan ALM, Inc. Celebrates 20th Anniversary

Ryan ALM, Inc. Celebrates 20 th Anniversary Mission: Protecting and Preserving Pensions Ryan ALM, Inc. was incorporated in Delaware on June 15, 2004. Ronald J, Ryan, founder, says that “we...

Source: Ryan ALM, Inc. Celebrates 20th Anniversary

Ryan ALM, Inc. Celebrates 20th Anniversary Mission: Protecting and Preserving Pensions

Ryan ALM, Inc. was incorporated in Delaware on June 15, 2004. Ronald J, Ryan, founder, says that “we created our company to be dedicated to asset liability management (ALM) as our name suggests. We are quite proud of our progress and achievements in ALM. We have built a turnkey system of products that are quite unique in the ALM industry that we treat as assets shown on our balance sheet, to include:

Custom Liability Index (CLI) – assets need to know what they are funding. Usually, it is monthly net liabilities (benefits + expenses – contributions). Such net liabilities are based on actuarial projections even though actuaries do not calculate net liabilities. The CLI is the proper benchmark for all LDI and ALM objectives. The CLI performs numerous calculations including present values, duration, growth rates, interest rate sensitivity, YTM, etc.

ASC 715 Discount Rates – Ryan ALM is one of few vendors providing ASC 715 discount rates in conformity to FASB. We produce four unique yield curves of AA zero-coupon corporate bonds. Usually, our discount rates are higher than our competitors providing for lower liability valuations and enhanced balance sheets.

Liability Beta Portfolio™ (LBP) – our asset management division, Ryan ALM Advisers, LLC, is entirely focused on cash flow matching as our only ALM product we call LBP. We feel strongly that our LBP provides the most benefits in harmony with the true pension objective of funding liabilities in a cost-efficient manner with prudent risk. Our LBP matches and funds monthly liability cash flows with certainty while reducing funding costs by 2% per year (20% on 1-10 year liabilities). Our LBP will outyield the CLI and enhance the ROA for bonds.

Performance Attribution Report (PAR) – given our CLI, we can calculate the relative risk/reward behavior of assets (as measured by our LBP) versus liabilities (as measured by the CLI). PAR calculates 14 risk/reward measurements including two graphs to clearly show the value added (or lost) of assets versus liabilities. This should be critical information for consultants and plan sponsors to understand how well the plan is being funded.

Asset Exhaustion Test (AET) – assets need to know the hurdle rate or ROA needed to fully fund net liabilities. The current ROA most pensions use is not an accurate calculation of a hurdle rate. Our AET clearly shows the annual difference of asset cash flows versus liability cash flows. We calculate a matrix of ROAs to arrive at the most applicable target ROA. Usually our calculated ROA (AET) is much different and lower than the current ROA since we focus on net liabilities not gross liabilities which reduces the liability cash flows assets need to fund (perhaps significantly).

We are very proud of our synergistic system and thankful for our team of experts with over 168 years of experience. Ryan ALM remains dedicated to achieving the true pension objective of funding liabilities with low cost and low risk.”

Pension Confusion - The Problem with Averages

Pension Confusion: The Problem with Averages Most pension have assets managed to generic market index benchmarks and/or liabilities. In both cases, the focus of these assets is to match or...

Source: Pension Confusion - The Problem with Averages

Pension Confusion:

The Problem with Averages

Most pension have assets managed to generic market index benchmarks and/or liabilities. In both cases, the focus of these assets is to match or beat some average (i.e., duration, total return, YTM). Unfortunately, few understand how these averages can be misleading if not erroneous.

Liabilities (Duration Matching)

Duration matching is a common LDI strategy for pensions where the plan sponsor looks to immunize their bond portfolio versus the interest rate sensitivity of the liabilities they are funding. To achieve this interest rate immunization, the strategy is to match the average duration of the liabilities. There are at least four problems here:

The actuary does not provide the average duration of projected benefits.

The actuarial report usually comes out annually… months after the fiscal year. Duration is a present value calculation that changes with interest rates and time, both of which change daily.

Assets do not fund gross projected benefits. They fund net benefits after contributions. This net liability is not calculated by the actuary which can be much different than the gross liability in dollars and duration especially for Corporate and Public pension plans that have a high contribution rate. Pension assets need to know what they are funding. The economic reality is… assets are funding net liabilities after contributions!

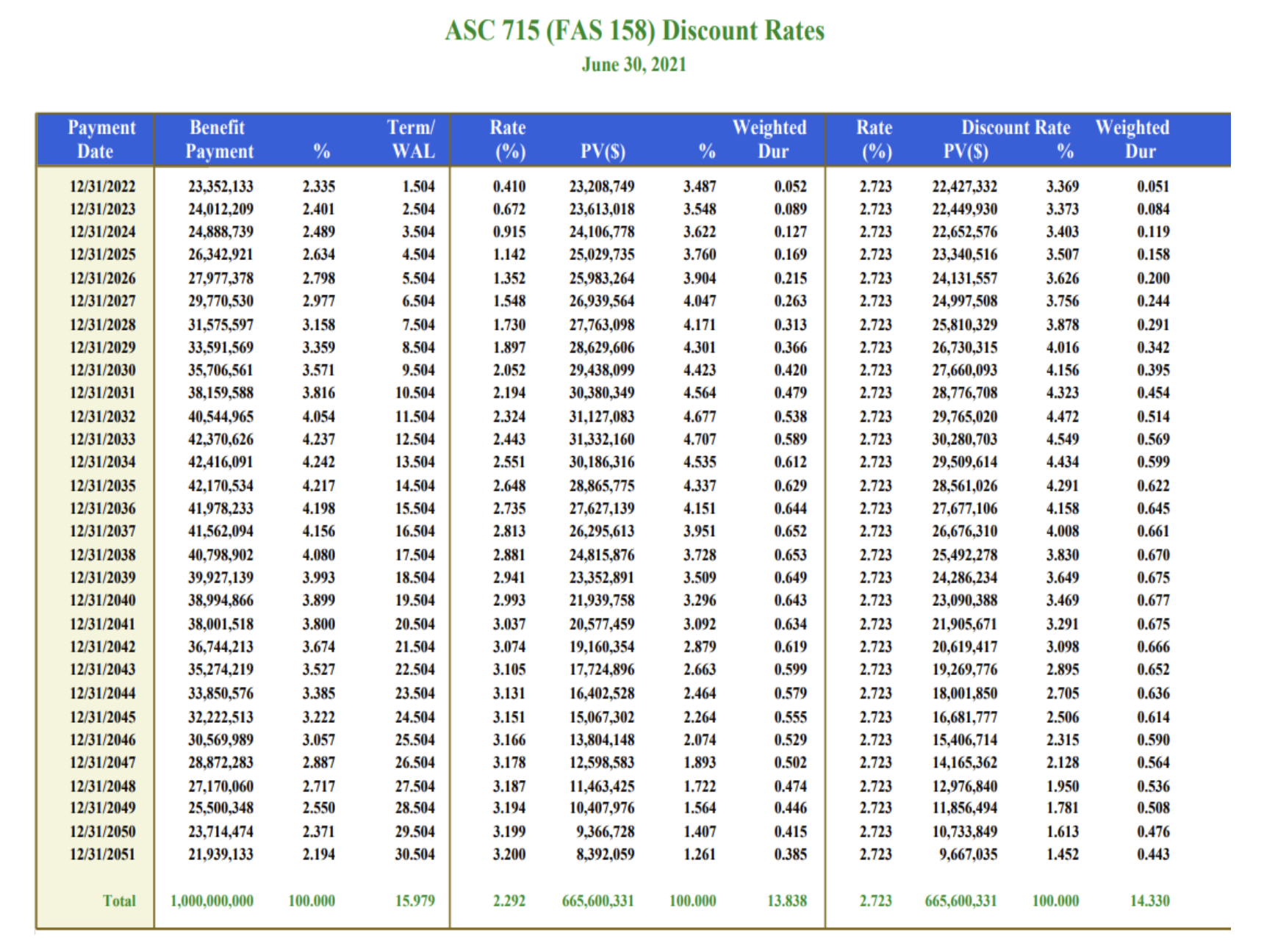

Duration is a present value calculation based on a discount rate yield curve. ASC 715 is the most prominent and acceptable for corporate and multiemployer pension plans. Moreover, Moody’s has adopted ASC 715 discount rates to assess municipal credits instead of the ROA discount rate commonly used under GASB accounting. FASB requires that this ASC 715 discount rate yield curve be converted to a single rate average discount rate. The duration of this single discount rate is certainly different than the average of a multiple discount rate yield curve. In the sample liability term structure shown on the next page priced with ASC 715 discount rates, we calculate:

| ASC 715 Yield Curve | Single Rate | Difference | |

|---|---|---|---|

| Average Yield | 2.29% | 2.72% | 0.43% |

| Duration | 13.84 years | 14.34 years | 0.50 years |

Note: For an accurate immunization, you need to match the duration of the ASC 715 yield curve (all liabilities) not the single rate average duration.

Solution: $ Duration Matching with Modified Duration

Maturity is an indicator of interest rate risk because longer maturity bonds move more in price than shorter maturity bonds given a change in yield. However, maturity is not a good measure of interest rate risk because maturity only considers the timing of the final principal cash flow at maturity and ignores the sizes and timing of all the other cash flows leading up to maturity.

The present value or price volatility of pension liabilities behaves just like bonds. A pension liability schedule is a term structure or yield curve of ASC 715 rates. Therefore, the interest rate risk in a pension liabilities schedule (actuarial projected benefits) can be matched with a portfolio of bonds.

A better measure for interest rate risk in the form of price sensitivity is called Modified Duration. Modified Duration considers all the bonds cash flows and is the weighted average time to receipt of all the cash flows, with the weights being the present values of the cash flows divided by a factor of (1+Y) where Y is the annual yield to maturity of the bond.

Modified Duration represents the percentage price change in market value in response to a change in the asset or liability yield. By weighting modified duration by the market value of the holding, that is, by multiplying the market value of the position by its modified duration, we get dollar-weighted duration. This dollar-weighted duration is known as Dollar Duration and represents the actual dollar change in market value for a bond given a change in its yield. Dollar duration is typically expressed in the dollar value change per one basis point change in yield (DV01).

The major advantages of using dollar duration are that it is additive and better suited for asset liability management. Dollar duration extends easily from individual securities to entire portfolios. The dollar duration of a portfolio is simply the sum of the dollar durations of all the individual holdings. The dollar duration of a bond portfolio can be matched to the dollar duration of pension liabilities. Bond durations cap out around 20-years so for liabilities with durations longer than 20-years it is not possible to match duration but… it is possible to match the Dollar duration of liabilities with durations longer than 20-years. Therefore, Dollar duration is very useful in asset liability management for liability driven investors such as defined benefit pension plans.

Ryan ALM uses dollar duration matching to help reduce pension volatility as defined as the dollar value difference in interest rate sensitivity between the present value of assets and liabilities. Ryan ALM starts by creating a Custom Liability Index (CLI) for each pension client. The Custom Liability Index is derived from the unique liabilities cash flow schedule provided by the plan actuary. The CLI measures and monitors the change in present value for the liabilities given a change in ASC 715 discount rates and is the proper benchmark for a plan sponsor and their liability driven investor(s).

Once we have determined the interest rate risk in the liabilities, the next step is to ensure that the bond portfolio has the same amount of interest rate risk as liabilities in order to reduce volatility between the present value of assets and liabilities. Ryan ALM builds a bond portfolio called the Liability Beta Portfolio (LBP) that matches the cash flows of the bonds to the liability cash flows (benefit payments). Since dollar duration is additive, we can set the dollar duration of the bond portfolio equal to the dollar duration of liabilities. Ryan ALM believes that cash flow matching liabilities with bond cash flows along with the use of dollar duration is a lower cost and lower volatility approach to pension asset liability management. It is certainly more accurate than traditional duration matching to immunize interest rate sensitivity.

Duration vs. Cash Flow Matching

Pension Solutions: Dollar Duration Matching and Cash Flow Matching Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits in a cost-effective manner...

Source: Duration vs. Cash Flow Matching

Pension Solutions:

Dollar Duration Matching and Cash Flow Matching

Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits in a cost-effective manner. Pension management is an assets vs. liabilities objective rather than assets versus generic market indexes objective. Pension asset/liability management (ALM) starts with understanding the pricing and interest rate sensitivity of liabilities and continues with measuring and monitoring such liabilities. There are two primary asset/liability bond strategies in use today: Duration Matching and Cash Flow Matching.

Duration Matching

The purpose of duration matching is an attempt to match the interest rate risk sensitivity of assets to liabilities. The objective is to have the market value or PV changes (growth rate) in the bond portfolio match the market value or PV changes (growth rate) in liabilities for a given change in interest rates. Many fixed income managers attempt to match the average duration of the bond portfolio to the average duration of a bond market index with a similar duration to liabilities (i.e., Bloomberg Barclays long Corporate index). They use the generic bond index as a proxy for liabilities. There are several problems with this strategy.

The fatal flaws in this approach are:

a generic bond index cannot replicate any client’s unique liability cash flows. Client’s liabilities are like snowflakes: different labor force, salaries, mortalities and plan amendments.

average durations give erroneous information because there are an infinite number of combinations of maturities for a bond portfolio that can all have the same average duration, but they will not have the same risk/reward profile.

duration matching is only accurate for small parallel shifts in the yield curve. But the yield curve rarely moves an equal number of basis points at every point along the curve. For more info, Ron Ryan wrote a research paper “The Seven Flaws of Duration” while head of Ryan Labs… see the Ryan ALM website/insights/white papers/classics.

Bond management evolved to remedy these flaws by using Key Rate Durations which attempts to match the duration of multiple points along the yield curve. Key Rate Duration is an improvement over using a single average duration, but it still has several deficiencies:

Actuaries usually do not provide the average duration of liabilities and the projected benefits in their annual actuarial report… reason why generic bond indexes are used.

Matching key rate durations of a generic market index = wrong Key Rate Durations.

Duration is a present value calculation requiring pricing each projected benefit with a discount rate yield curve (i.e., ASC 715 discount rates). As a result, 30 annual benefit payments require 30 separate discount rates.

Duration must be modified (duration/1+YTM) to use as a price return measurement.

Modified duration is a price return measurement and does not include income.

Dollar Duration Matching (DDM)

DDM matches the Dollar Value change per basis point change in yield for assets with the Dollar Value change per basis point change in yield for liabilities. When the Dollar Duration of assets is matched to the Dollar Duration of liabilities for every year in the term structure of liabilities, then DDM is the most precise form of Key Rate duration matching because it matches the Key Rate durations at every point along the liabilities yield cure or benefit payment schedule (30 years = 30 key rate durations). The Ryan ALM approach offers several value-added differences:

Actuarial Projections - We use the actuarial projected benefits of our clients and not a generic bond index.

Modified durations - to be an effective price sensitivity measurement, duration must be modified. Modified Duration measures the percent change in market value or

Dollar duration - our objective here is to match the dollar value change per basis point in assets and liabilities in every maturity on the projected benefit schedule.

The Ryan ALM DDM approach greatly improves the accuracy of Key Rate duration matching by matching the Dollar Value changes in liabilities with the Dollar Value changes in assets across the term structure and yield curve for both assets and liabilities. The liabilities are represented by using a Custom Liability Index to more precisely measure and monitor the dollar value movement in assets versus liabilities given any movement in interest rates.

Cash Flow Matching (CFM)

Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits when due in a cost-efficient manner. Ryan ALM does not believe that bonds are performance assets. The value in bonds is in their known and scheduled cash flows which is why cash flow matching has been used as a major strategy for hedging liabilities for many decades (i.e., dedication, defeasance). It is the matching and funding of benefits (future values) that is of primary concern. As such, future values are not interest rate sensitive… a major benefit of cash flow matching. Cash flow driven investing (CDI) dominates the way European pensions are managed under IASB accounting standards. Key Rate Duration using Dollar Duration is great for matching market value (PV) movements between assets and liabilities but what about funding liability payments (future values)?

Since the primary value in bonds is in the certainty of their cash flows, Ryan ALM will cash flow match (fund) projected benefit payments chronologically which provide the plan sponsor with numerous benefits:

Secures the benefits,

Significantly de-risks the plan,

Reduces funding costs significantly,

Reduces volatility of funded ratio and contributions,

Buys time for performance assets (Alpha) to grow unencumbered,

Hedges pension inflation on Retired Lives, Active Lives and Expenses, and

No interest rate risk since LBP is funding future values (benefit payments).

A major cash flow matching benefit is that it buys time for the performance assets to grow unencumbered. History tells us that given time risky assets perform better (i.e., S&P 500). History also tells us if the Alpha assets can grow without any dilution, they perform much better (dividends reinvested > 50% of the S&P 500 growth in the last 50 years). If interest rates rise, cash flow matching can reinvest any excess cash flows at the then higher yields (lower costs) while bonds managed with a purely total return focus would get hurt with lower price returns.

Solutions

Ryan ALM uses a turnkey system approach to asset/liability management for defined benefit pensions:

ASC 715 Discount Rates – Ryan ALM is one of few vendors providing ASC 715 discount rates (AA corporate zero-coupon bonds). We will price each annual projected benefit payment on a monthly basis.

Custom Liability Index (CLI) - Ryan ALM creates a Custom Liability Index (CLI) for each client based on their actuarial projected benefits. We do not use generic market indexes because that would be assets vs. assets. We measure and monitor the performance of assets versus liabilities. The CLI provides all of the calculations needed for either duration matching or cash flow matching. The CLI will calculate YTM, duration, growth rate and interest rate sensitivity for each annual projected benefit as a term structure as well as total liabilities.

Liability Beta Portfolio™ (LBP) – our LBP will cash flow match projected benefits either chronologically or as a dollar duration match using our proprietary LBP cost optimization model that will reduce funding costs significantly.

Whether it is dollar duration matching or cash flow matching, Ryan ALM provides both products as part of our asset/liability management product line. Please contact us to learn how our turnkey system can enhance your pension fund.

Cash Flow is King!

Executive Summary Pensions are all about cash flows. They require asset cash flows including projected contributions to fund projected benefits + expenses.Retired Lives are the most imminent and certain liability...

Source: Cash Flow is King!

Executive Summary

Pensions are all about cash flows. They require asset cash flows including projected contributions to fund projected benefits + expenses.Retired Lives are the most imminent and certain liability cash flows and should be the highest priority to fund and secure these benefits.Cash flow matching Retired Lives chronologically with bonds (Beta assets) is the most prudent way to secure these benefits in a cost efficient manner. Unfortunately, most bond assets) who need to grow unencumbered to fund

Pension Solution:

Cash Flow Is King!

The primary objective of a pension is to secure benefits in a cost-efficient manner and then secondarily to enhance the efficiency of the plan’s asset allocation. Securing benefits is all about asset cash flows matching and funding liability cash flows chronologically for 10-years or for as far out as the plan sponsor deems necessary.

Insurance Buyout Annuity (IBA)

Cash Flow Matching (CDI) with bonds

IBA is too expensive for Public and multi-employer plans and unnecessary. Corporations use them to remove the PBGC premium expense on Retired Lives. However, corporations would be wise to compare cash flow matching (Cash Flow Driven Investments or CDI) to IBA. We believe they will find that CDI would reduce funding costs by over 20% in present value dollars versus the future value savings of eliminating PBGC premiums. CDI has been in vogue the longest (since the 1960s) and is a proven way to defease liabilities in a low cost, low risk manner.

It would be wise to separate Retired Lives from Active Lives. The Retired Lives are the most important liabilities since they are the most imminent and known benefits as well as they represent long tenured employees. These are the benefits that need to be secured as best as possible. The Active Lives are the less known and longest liabilities, which allow assets time to grow to fund these benefits.

Since contributions are the first source to fund benefits, current assets fund net liabilities. The actuarial projections of benefits and contributions tend to be annual. Net liabilities are usually not provided by the actuary. Moreover, benefits are paid monthly. Although an easy calculation, it is critical that current assets know what they are funding… monthly net liabilities (projected benefits + expenses – contributions).

It would be wise to separate liability Beta assets from Alpha assets. The Beta assets should be the allocation to bonds to cash flow match net Retired Lives chronologically for a target horizon (we recommend 10 years). Our cash flow matching model (Liability Beta Portfolio™ or LBP) is well tested showing a funding cost savings of 8% to 15% depending on the liability term structure.

It would be wise to take the Cash plus the Fixed Income allocation in your plan’s current asset allocation and apply it to a CDI allocation. This would match and secure benefits chronologically for as far out as the allocation of funds allow. Since we are dealing with net liabilities (after contributions) a 15% allocation may fund liabilities out to 10-years +.

Typically bond allocations are expected to outperform some generic bond index whose cash flows look nothing like the Retired Lives. Moreover, the index benchmark may be skewed to long bonds and Government securities. This introduces interest rate risk and more cost, as yields on government securities are generally the lowest for a similar maturity. Our LBP model is funding benefits (future values) which are not interest rate sensitive. This eliminates the largest risk in bonds. Our LBP model will usually outyield active bond managers by over 50 bps, which will reduce costs. The key value added is the efficiency of the cash flows.

No matter what generic bond index is chosen, active fixed income management cannot produce enough cash flows to fund benefits and expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the core portfolio to fund the shorter Retired Lives net liabilities (1-10 years), the Alpha assets are now free to grow without being diluted or unencumbered to pay any benefits. Alpha assets returns will be volatile, but the Liability Beta Portfolio™ bought the plan time (10 years) for the Alpha assets to grow. The example below shows the cash flow difference of bonds managed to a generic index versus cash flow matching to liabilities:

Assumptions

Bond + Cash Allocation = $150 million (15%)

Net Benefits + Expenses (B + E) = $20 m per year ($200 million for 10 years)

Active bond management vs. generic bond index

YTM = 2.50%

Cash flow = $3.75 million annually ($150m x 2.50%)

Cash flow shortfall = $16.25m annually ($20m - $3.75m)

Requires dilution of Alpha assets cash flow to fund the B + E

Liability Beta Portfolio™

YTM = 3.50%

Cash flow = $20 million annual

No dilution of Alpha assets cash flows

Cash flow = Principal + Income + Reinvestment

Benefits of a CDI Approach

Secures benefits for 10 years

No change in Cash and Bond allocation

No dilution of Alpha assets to fund B + E

No interest rate risk (funding future values)

Outyield active bond management which reduces costs

LBP is skewed to higher yielding A/BBB corporate bonds

LBP has no maturities longer than last benefit payment date

Observations

Generic bond indexes cash flows look nothing like the projected benefit payment schedule of a pension.

This leads to a mismatch of cash flows and risk/reward behaviors… serious issues over time.

Alpha assets need time to perform without any dilution of their cash flows to pay benefits so they shouldn’t be a source of liquidity

CDI funds benefit payments and expenses chronologically

CDI will out yield current bond managers and enhance the ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Logic

Let the performance assets (Alpha assets) perform (grow unencumbered) as the liquidity assets (Beta) assets provide cash flow sufficient to fund benefits plus expenses chronologically.

Was founded by Ronald J. Ryan, CFA on July 12, 2004 as an Asset/Liability Management (ALM) firm. The firm builds a turnkey system of proprietary synergistic products designed to measure liabilities as a Custom Liability Index (CLI) and manage assets to the CLI as a Liability Beta Portfolio™

Our Liability Beta Portfolio™ is our proprietary cost optimization model that "cash flow matches" clients projected liability benefit payment schedules at the least cost using investment grade bonds. It is back-tested since 2009 showing a consistent cost savings of 8% to 15%. Our LBP best represents the core portfolio of a pension plan.

Buy Time!

Executive Summary U.S. pension plans have been hard hit by rising pension costs since 2000. This has been primarily characterized by spiking contribution costs and volatile funded ratios. A solution...

Source: Buy Time!

Executive Summary

U.S. pension plans have been hard hit by rising pension costs since 2000. This has been primarily characterized by spiking contribution costs and volatile funded ratios. A solution to this dilemma is to implement a strategy that will buy time! By separating assets into liquidity (Beta) and performance (Alpha) assets, you can achieve the true objective of a pension, which is to secure benefits. The Beta assets secure Retired Lives benefits chronologically (we recommend 10 years) thereby buying time for the Alpha assets to enhance the funded status, while besting future liability growth.

Pension Solution: Buy Time!

Ryan ALM's mission is to solve liability driven problems through low cost, low risk solutions.

Most pensions have been hard hit this year. According to a March study by Milliman of the top 100 Public Pensions, the average funded ratio fell to 66% from 74.9% at the end of 2019. This represents the largest decline Milliman has ever recorded. The funded status deficit grew to $1.82 trillion. They reported only four plans with funded ratios > 90% and 35% were < 60% funded using the ROA as the discount rate. Imagine the funded ratio if Public Plans adopted FASB discount rates of AA corporates. Lower funded ratios also suggest higher contributions are coming. What to do?

How do you buy time? Cash flow match liabilities for the time you need.

We believe the answer is… BUY TIME!

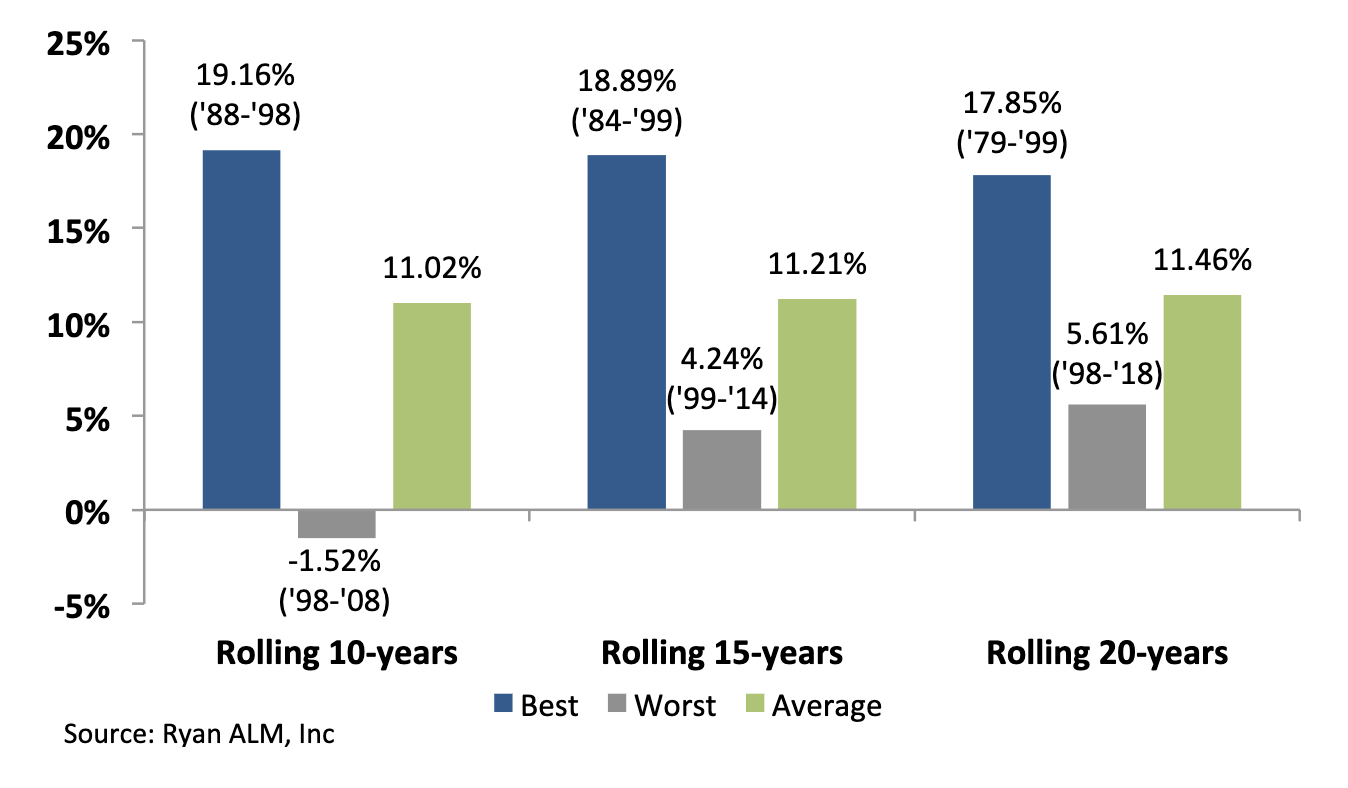

Given time, equities (S&P 500) perform well but they need time. The more time you give equities… the better the returns. Here are historical average S&P 500 return measurements for rolling 10-year, 15-year and 20-year periods ending 12/31/19 over a 50-year horizon starting 1969:

Best, worst, and average returns

So how do you buy time? The answer is… cash flow match liabilities for the time you need. This is best accomplished by transferring the cash + bond allocation assets in kind over to cash flow match net liabilities + expenses. Our cash flow matching model (Liability Beta Portfolio™ or LBP) will calculate with precision the cost to fund net liabilities + expenses in a cost-effective manner chronologically. Since liabilities are funded initially by contributions, using the LBP model to cash flow match net liabilitieschronologically may be able to fund more liabilities than you think. Assume that a 15% bond + 3% cash allocation could match the next 10 years of net Retired Lives benefit payments + expenses chronologically. Based on the Ryan ALM Liability Beta Portfolio™ (LBP) model we show a cost savings (projected benefits – cost of LBP) of about 10% to 15% on cash flow matching the first 10 years of net liabilities (projected benefit payment schedule – projected contributions).

Matching liabilities chronologically should buy time for the non-bond assets (Alpha assets) to perform. Given time (10 years) most non-bond asset classes tend to outperform bonds and the ROA. Since liabilities behave like bonds there is a high probability that non-bond asset classes could outperform liability growth (earn liability Alpha) over an extended time horizon especially at today’s low yield on bonds and liabilities. This would enhance the funded status allowing for reduced contribution costs or increased benefits or both. Our LBP also has numerous benefits that enhance the pension plan:

Secures Benefits

Cash flow match monthly Retired Lives benefits chronologically

Reduces Costs

LBP reduces Contribution, Funding and Asset Management Costs:

(LBP Fee = 15 bps… much less than most active bond managers)

Reduces Volatility

Reduces volatility of Contributions and Funded Ratio

Reduces Risk

Risk = Uncertainty of Funding Benefit Payments

(LBP funds benefits with certainty)

Projected Benefit Payments are Future Values

(FV have NO Interest Rate Sensitive)

Enhances ROA

LBP should out yield most active management bond portfolios

Buys Time

LBP matches & funds liabilities chronologically

Moves deficit out longer extending the investment horizon

Buys Time for Non-bond assets (Alpha assets) to grow

No dilution of Alpha assets to fund benefits

However, most bond allocations are for active bond management versus a generic index benchmark(s). As the designer of the Lehman bond indexes from my days as the Director of Fixed Income Research at Lehman, I can tell you unequivocally that generic bond indexes look nothing like a projected pension benefit payment schedule. Such a mismatch will distort the cash flows and risk/reward behavior of assets vs. liabilities. The major issues and differences are:

Versus Generic Bond Indexes

Does not fund benefits + expenses

Aggregate Index = low yielding @ 1.42%

Generic bond index =/= plan sponsor’s liabilities

Cash flows do not match plan sponsor’s liabilities

Index skewed to long bonds + Government securities

Performance (value added) = small to none (after fees)

Cash Flow Matching (Liability Beta Portfolio™ – LBP)

Custom Liability Index = plan sponsor’s liabilities

LBP funds Net Benefit + Expense payments (monthly)

Performance = immediate funded cost savings of 8% to 20%

But the worst difference and discrepancy is… all about cash flows. Active bond management is focused on outperforming the returns of a generic bond index benchmark. As a result, cash flows are not a consideration. But no matter what generic bond index is chosen; the fixed income assets cannot produce enough cash flows to fund benefits + expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the corebond management is focused on outperforming the returns of a generic bond index benchmark. As a result, cash flows are not a consideration. But no matter what generic bond index is chosen; the fixed income assets cannot produce enough cash flows to fund benefits + expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the core portfolio to fund the shorter Retired Lives net liabilities (1-10 years), the Alpha assets are now free to grow without being diluted or unencumbered to pay any benefits. Alpha assets returns will be volatile, but the Liability Beta Portfolio™ bought time (10 years) for the Alpha assets to grow. The example below shows the cash flow difference of bonds managed to a generic index versus cash flow matching to liabilities:

Bond + Cash allocation = $150 million

Net Benefits + Expenses = $20 million per year

Bond management vs. generic bond index

YTM = 2.50%

Cash flow = $3.75 million annual ($2.50% x $150m)

Annual cash flow shortfall = $16.25 million ($20m - $3.75m)

Dilution of Alpha assets cash flow to fund benefits + expenses

Cash Flow Matching

YTM = 3.50% (skewed to A/BBB corporate bonds)

Cash flow = $20 million annual (includes principal + income + income reinvested)

No dilution of Alpha assets cash flows

Observations:

Generic bond indexes look nothing like the projected benefit payment schedule of a pension.

This leads to a mismatch of cash flows and risk/reward behaviors… serious issue over time.

Alpha assets need time to perform without any dilution of their cash flows to pay benefits.

Cash flow matching funds benefit payments chronologically

Cash flow matching will out yield current bond managers and enhance ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Logic

Let the performance (Alpha) assets perform (grow) as the liquidity (Beta) assets provide cash flow sufficient to fund benefits plus expenses over a time horizon sufficient to let the Alpha assets grow unencumbered.