Ryan ALM

White Papers

Problem/Solution: Generic Indexes

Problem: Find Pension Liabilities in any Generic Bond Index Solution: Custom Liability Index (CLI) Pension liabilities are unique to each plan sponsor… different salaries, benefits, expenses, contributions, mortality, inflation assumptions,...

Source: Problem/Solution: Generic Indexes

Problem: Find Pension Liabilities in any Generic Bond Index

Solution: Custom Liability Index (CLI)

Pension liabilities are unique to each plan sponsor… different salaries, benefits, expenses, contributions, mortality, inflation assumptions, plan amendments, etc. In an effort to capture and calculate the true liability objective, the Ryan team created the first Custom Liability Index (CLI) in 1991 as the proper pension benchmark for asset liability management (ALM). We take the actuarial projections of benefits and administrative expenses (B+E) for each client and then subtract Contributions to calculate the true liability cash flows that assets have to fund since contributions are the initial source to fund B+E. We then calculate the monthly liability cash flows as (B+E) – C. The CLI is a monthly report that includes the calculations of:

Net future values broken out by term structure

Net present values broken out by term structure

Total returns broken out by term structure

Summary statistics (yield, duration, etc.)

Interest rate sensitivity

The Ryan ALM CLI should be installed as the index benchmark for any bond manager as well as total assets. This should be the first step in asset management and asset allocation. The CLI can be broken out into any time segment that bond assets are directed to fund (i.e. 1-3 years, 1-10 years, etc.). Moreover, total assets should be compared versus total liabilities to know if the funded ratio and funded status have improved over time. If all asset managers outperform their generic index benchmarks but lose to liability growth rate (total return)… the pension plan loses and must pay a higher contribution.

Since the CLI is a monthly report, plan sponsors can compare assets versus liabilities monthly. There should never be an investment update of just assets versus assets (generic index benchmarks) which is common. It is hard to understand in today’s sophisticated finance world, that liabilities are missing as an index. The reason must be that it is extra work for each client. But it should be clear that no generic bond index could ever properly represent the liability cash flows that assets are required to fund. It is apples versus oranges.

“Given the wrong index benchmark… you will get the wrong risk/reward”

Pension Confusion - Find the Liabilities

Securing and funding liabilities in a cost-efficient manner with prudent risk is the true pension objective. Although liabilities should be the focus of pensions, it is hard to find liabilities...

Source: Pension Confusion - Find the Liabilities

Securing and funding liabilities in a cost-efficient manner with prudent risk is the true pension objective. Although liabilities should be the focus of pensions, it is hard to find liabilities in asset allocation, asset management and performance measurement… especially forPublic and Multiemployer Plans,as theseplans are asset only focused. Private plans are very much liability driven although they have opted out of pensions to buy Insurance BuyOut annuities as a major trend for over ten years.Given the 500 bps increase in the Fed Funds rate in the last two years, Private plans need to revisit the economics of BuyOut annuities versus a defeasance strategy (cash flow matching). I think they may find that a defeasance strategy has definite cost advantages today.

So, what’s the matter? There is an obvious disconnect between assets and liabilities because liabilities are missing from every critical asset function:

Asset Allocation (AA)

Liabilities are like snowflakes, you never find two alikeas each pension plan has a different labor force, salaries, mortality and plan amendments. There can never be a generic market index to replicate any plan sponsor’s unique liability cash flows. Liabilities are the domain of the actuary. They produce a very thorough annual report detailing and itemizing numerous liability calculations. The actuaries do an amazing job given the huge number of calculations. They have a tedious and most important function as the calculator and custodian of the liabilities. This voluminous work is usually presented as an annual report a few months after the end of the fiscal year. More importantly, the actuary calculates the funded status which should be the focus of asset allocation, asset management, and performance measurement.

Most pension asset allocations are based on earning a target ROA or hurdle rate. The ROA is calculated by weighing the expected return for a series of asset classes. Each asset class has its own ROA based on its index benchmark estimated return. Pension consultants are quite diligent in analyzing each asset class and assigning the proper weight to achieve the target ROA and risk behavior. Thorough quarterly reports are presented by the consultants to plan sponsors detailing the risk/reward of every asset manager versus the index benchmark assigned to that asset class as the bogey. As a result, generic market indexes are the driver and focus of asset allocation.

AA should be responsive to the funded status of each client. A 90% funded plan should have a much more conservative AA than a 60% funded plan. But most, if not all, asset allocation models ignore the funded status and focus on achieving the target ROA with the highest probability of success and prudent risk based on historical returns of a database that is almost 100% generic market indexes. The historical risk/reward behavior of numerous generic market indexes are

inputs into an AA optimization model that provides a baseline allocation of each asset class. The pension consultant will then massage those weights to best fit each client. Too often plan sponsors have similar asset allocations no matter what their funded status is because they have similar ROA targets. This has led to inappropriate AA especially in the late 1990s and early 2000s that were heavily skewed to risky assets although the pension plans were greatly overfunded then. Had pensions defeased their liabilities then through a cash flow matching strategy with investment grade bonds, they could have secured their surplus victory and stabilized low contribution costs. Instead, the equity correction of 2000-02 wrecked the funded status of almost all pensions causing spiking contribution costs which have not subsided even today.

Without knowledge of the economic funded status on a frequent and accurate basis, AA cannot function effectively. If the market value of assets is the most accurate measurement of asset valuation then the same is true for liabilities. The Society of Actuaries (SoA) delivered a research paper “Principles Underlying Asset Liability Management (ALM)” years ago that warns of erroneous accounting valuations and recommends that pensions create a set of economic books:

“A consistent ALM structure can only be achieved for economic objectives. Accounting measures can sometimes distort economic reality and produce results inconsistent with economic value. Because ALM is concerned with the future asset and liability cash flows, the natural focus of ALM is economic value.”

Ryan ALM Translation: Pension plans need to create a set of “economic books” so ALM can function effectively. It’s all about asset cash flows funding liability cash flows. A Custom Liability Index (CLI) is the method and proper benchmark to create economic books.

With a CLI in place, consultants and plan sponsors can now know monthly the true economic funded status and liability growth rate. With a CLI, consultants now possess pertinent and private information for each of their clients that no other consultant would have…. a significant advantage over competition. The CLI allows consultants to now customize the AA to best fit the clients dynamic funded status with timely adjustments. Although the actuaries don’t produce a CLI, it is based on the private actuarial projections of benefits, administrative expenses and contributions. Ron Ryan and his team created the first CLI in 1991 as the true benchmark of a pension. The Ryan ALM CLI provides all of the calculations needed for efficient AA, ALM, and performance measurement.

Asset Liability Management (ALM)

It would be hard, if not impossible, for an asset manager to manage assets versus a generic market index if it came out annually, months after the end of the fiscal year with no transparency (index constituents not shown) and it wasn’t priced at the market. Well welcome to the pension world of liabilities. Liabilities are an annual actuarial calculation that has little or no transparency (projections usually not shown) and is priced at the ROA (GASB) as the discount rate. The ROA discount rate is certainly not a market rate you can buy to settle the liabilities. The ROA discount rate is one of the accounting distortions of economic reality the SoA referenced.

This was the message from the SoA. You need to create a set of economic books for ALM to function effectively. This is why a CLI is the critical step in ALM. Assets need to know what they are funding. The answer is usually net liabilities defined as (benefits + expenses) – (contributions) since contributions are the first source to fund the liability cash flows. Because net liabilities are not calculated in the actuarial report, the CLI should be a requirement to understand the net liability cash flows that asset cash flows must fund. Such net liability cash flows are also monthly which is another calculation made by the CLI.

If the true pension objective is to secure benefits in a cost-efficient manner with prudent risk, then cash flow matching (CFM) must be the proper and best ALM strategy. CFM used to be called dedication and has been a stable approach to pension investing for over 50 years. Bonds are the only asset class with the certainty of its cash flows. That is the intrinsic value in bonds and the reason why CFM should be the core portfolio of any pension. As the funded ratio improves, a higher allocation should be given to CFM to secure more and more benefits while stabilizing the funded ratio and contributions.

Performance Measurement

Once the CLI is in place, it will provide monthly calculations of the net liability growth rate (returns). Total asset growth (returns) versus the total net liability growth rate is the critical performance measurement. If all of the asset managers outperformed their generic market index benchmarks but total asset growth underperformed total net liability growth rate… the plan loses. This lost shows up in higher pension expense (contribution costs) and a lower funded status.

With a liability objective, the terms Alpha and Beta now take on a different perspective. Liability Alpha is the excess return of asset growth rate versus the liability growth rate. Liability Beta is now the portfolio that matches the liability cash flows it is funding. With the CLI, liability Beta is now a Liability Index Fund. Without a CLI, performance measurement is comparing assets versus assets… this is in sharp contrast to the pension objective of assets versus liabilities.

Ryan ALM Pension Monitor 3Q’22

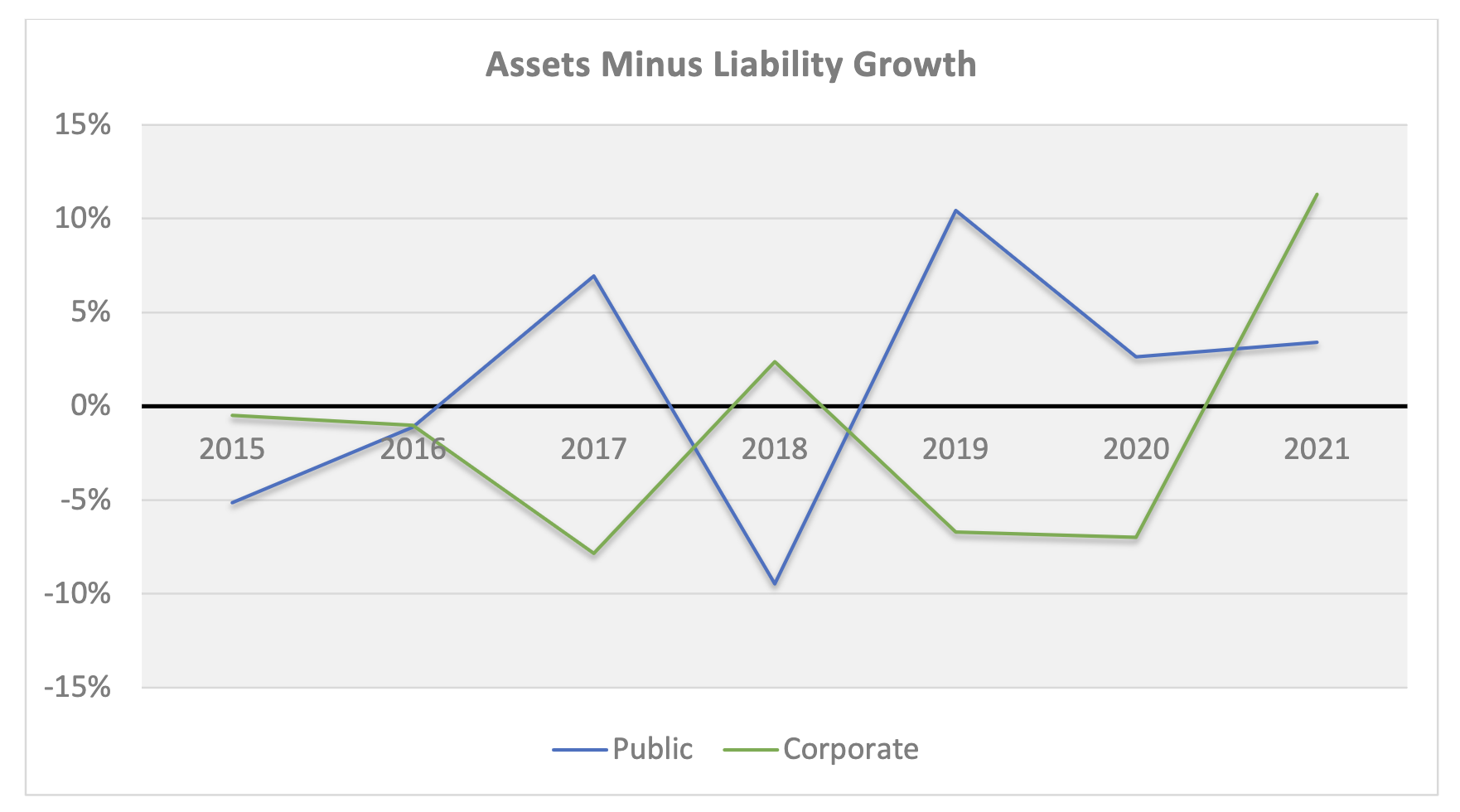

3Q 2022 Ryan ALM Pension Monitor (Through September 30, 2022) Pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets...

Source: Ryan ALM Pension Monitor 3Q’22

(Through September 30, 2022)

Pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets cannot be done efficiently or appropriately.

The funded ratio/status of pension plans are present value calculations. Each type of plan is governed by accounting rules and actuarial practices, which determine the discount rate used to calculate the present value of liabilities. Single employer corporate plans are under ASC 715 (FASB) discount rates (AA corporate zero-coupon yield curve); multiemployer plans and public plans use the ROA (return on asset assumption) as the liability discount rate. The difference in liability growth between these plans can be quite significant, which will affect funded status and contribution levels. The table below compares these different liability growth rates (based on a 12-year average duration) versus the asset growth rate using the P&I asset allocation survey of the top 1,000 plans which is updated each year. The graph below shows the contrasting annual differences of asset versus liability growth for corporate and public plans since 2015. The impact of different accounting rules is massive, especially during 2022’s rising rate environment.

| ASSET ALLOCATION | YTD Return | Corporate | Public | Union |

|---|---|---|---|---|

|

Domestic Stock International Stock Global Equity Domestic Fixed Income Global Fixed Income Cash Private Equity Real Estate Equity* Other |

-23.9% -27.1% -25.3% -14.6% -21.3% 0.2% 11.6% 8.6% 9.1% |

11.1% 6.5% 10.4% 46.7% 1.3% 2.0% 8.5% 4.1% 9.4% |

24.4% 16.3% 5.3% 20.2% 1.7% 2.0% 12.7% 7.9% 9.5% |

24.7% 8.6% 11.4% 28.0% 0.9% 0.6% 8.2% 9.3% 8.3% |

| TOTAL ASSETS Growth Rate | -12.0% | -11.9% | -12.9% | |

| LIABILITIES Growth Rate* | -25.9% | 5.6% | 5.6% | |

| Asset Growth – Liability Growth | 13.9% | -17.5% | -18.5% |

Index Benchmarks: Domestic Stock = S&P 500; Int’l Stock = EAFE, Global Equity = All Country World; Domestic Fixed Income = BB Aggregate; Global Fixed Income = FTSE World Gov’t (unhedged); Cash = 3 mo. T-Bill; Private Equity =10-year return for the R2500 + 2%; *Real estate Equity =NFI-DP Index (delayed one month); Alternative Investments and Other = CPI-U & 3%.

*Liabilities = Ryan ALM Custom Liability Indexes (CLI)

Footnote: The measurement of asset growth to liability growth is an annual calculation beginning on December 31, 2015. For periods shorter than 1-year, the observation is a YTD calculation.

Ryan ALM Pension Monitor 3Q ‘21

Ryan ALM Pension Monitor (Through September 30, 2021) Pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets cannot be...

Source: Ryan ALM Pension Monitor 3Q

(Through September 30, 2021)

Pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets cannot be done appropriately.

The funded ratio/status of pension plans are present value calculations. Each type of plan is governed by accounting rules and actuarial practices, which determine the discount rate used to calculate the present value of liabilities. Single employer corporate plans are under ASC 715 (FASB) discount rates (AA corporate zero-coupon yield curve); multiemployer plans and public plans use the ROA (return on asset assumption) as the liability discount rate. The difference in liability growth between these plans can be quite significant, which will affect funded status and contribution levels.

The table below compares these different liability growth rates (based on 12-year average duration) versus the asset growth rate based on the P&I asset allocation survey of the top 1,000 plans. The graph below shows the contrasting annual differences of asset versus liability growth for corporate and public plans since 2015.

| ASSET ALLOCATION | YTD 09/21 Return | Corporate | Public | Union |

|---|---|---|---|---|

|

Domestic Stock International Stock Global Equity Domestic Fixed Income Global Fixed Income Cash Private Equity Real Estate Equity Alternative Investments Other |

15.9% 8.3% 11.5% -1.6% -5.9% 0.1% 15.3% 10.5% 8.3% 8.3% |

10.6% 7.1% 13.3% 48.3% 0.7% 2.4% 6.2% 4.5% 4.6% 2.5% |

24.6% 16.9% 6.2% 21.0% 2.3% 2.0% 10.3% 8.7% 7.6% 1.4% |

24.7% 8.6% 11.4% 28.0% 0.9% 0.6% 8.2% 9.3% 8.3% 0.0% |

| TOTAL ASSETS Growth Rate | 5.0% | 8.7% | 8.4% | |

| LIABILITIES Growth Rate | -6.3% | 5.3% | 5.3% | |

| Asset Growth – Liability Growth | 11.3% | 3.4% | 3.1% |

Index Benchmarks: Domestic Stock = S&P 500; Int’l Stock = EAFE, Global Equity = All Country World; Domestic Fixed Income = BB Aggregate; Global Fixed Income = FTSE World Gov’t (unhedged); Cash = 3 mo. T-Bill; Private Equity =10-year return for the R2500 + 2%; Real estate Equity =NFI-DP Index; Alternative Investments and Other = CPI-U & 3%.

Footnote: The measurement of asset growth to liability growth is an annual calculation beginning on December 31, 2015. For periods shorter than 1-year, the observation is a YTD calculation.

Pension Solutions Series Part 4 - Performance Measurement

Pension Solution: Performance Measurement Most pension assets are managed versus a market index as the objective or benchmark. However, the true objective of a pension is to fund the pension...

Source: Pension Solutions Series Part 4 - Performance Measurement

Pension Solution: Performance Measurement

Most pension assets are managed versus a market index as the objective or benchmark. However, the true objective of a pension is to fund the pension liabilities (benefit payments) at the lowest cost to the plan with prudent risk. No market index could ever represent the liability objective of any pension. Just like snowflakes, no two pension liabilities are alike due to each plan having a different labor force, salaries, mortality and plan amendments. As pensions have experienced too often, given the wrong index objective … you will get the wrong risk/reward profile!

This has been the pattern for most pension plans as their Funded Ratios have been on a roller coaster for several decades. Until the true liability objective of a pension plan (and any liability driven objective) is measured and monitored frequently and accurately, pension assets are in jeopardy of being managed to the wrong index objective(s). Until a Custom Liability Index is built and put in place as the proper benchmark, all asset decisions are in danger of being mismanaged. Given the wrong index objective(s), performance measurement will then provide inappropriate risk/reward measurements. It is rare that pension assets are ever compared to pension liabilities in performance measurement reports. It follows that if you outperform the S&P 500 or any market index but lose to liability growth …the pension plan loses!

Traditional generic bond indexes do a good job of measuring the risk/reward behavior of a market sector but have nothing to do with pension liabilities. Only a Custom Liability Index (CLI) could ever measure and monitor the risk/reward behavior of any pension liability cash flow schedule. Since contributions are the initial source to fund benefits, current assets fund net liabilities (benefits – contributions). Assets need to know what they are funding… net liabilities!

Solution: Performance Measurement

Once the Liability Beta Portfolio™ is installed to cash flow match net Retired Lives chronologically, you now need the Alpha assets to outgrow net residual liability growth (benefits – contributions of 10-year + Retired Lives and Active Lives)) to enhance the funded status. The CLI will provide the growth rate of net residual liabilities just like any index benchmark so performance measurement of Alpha assets versus net residual liabilities (as measured by the CLI) can be easily assessed. If Alpha assets can outgrow net residual liabilities, then the funded status will be enhanced and contribution costs should be reduced. The Ryan ALM Performance Attribution Report (PAR) will calculate:

eight measurements of risk

four measurements of reward

two measurements of risk-adjusted returns

Pension Solutions Series Part 1 - Custom Liability Index (CLI)

Pension Solution: Custom Liability Index (CLI) Most pension assets are managed versus a market index as the objective or benchmark. However, the true objective of a pension is to fund...

Source: Pension Solutions Series Part 1 - Custom Liability Index (CLI)

Pension Solution: Custom Liability Index (CLI)

Most pension assets are managed versus a market index as the objective or benchmark. However, the true objective of a pension is to fund the pension liabilities (benefit payments) at the lowest cost to the plan with prudent risk. No market index could ever represent the liability objective of any pension. Just like snowflakes, no two pension liabilities are alike due to each plan having a different labor force, salaries, mortality and plan amendments. As pensions have experienced too often, given the wrong index objective … you will get the wrong risk/reward profile!

This has been the pattern for most pension plans as their Funded Ratios have been on a roller coaster for several decades. Until the true liability objective of a pension plan (and any liability driven objective) is measured and monitored frequently and accurately, pension assets are in jeopardy of being managed to the wrong index objective(s). Until a Custom Liability Index is built and put in place as the proper benchmark, all asset decisions are in danger of being mismanaged. Asset Allocation, Asset Management and Performance Measurement are all index driven. Given the wrong Funded Ratio, asset allocation will most probably function inappropriately. It follows that a pension plan with a surplus should have a different asset allocation than a plan with a large deficit. Such Funded Ratios need to be based on market or economic valuations not accounting or actuarial valuations. Given the wrong index objective(s), asset management will behave accordingly and produce an inappropriate risk/reward profile (same as index benchmark). Given the wrong index objective(s), performance measurement will then provide inappropriate risk/reward measurements. It is rare that pension assets are ever compared to pension liabilities in performance measurement reports. It follows that if you outperform the S&P 500 or any market index but lose to liability growth …the pension plan loses!

Traditional generic bond indexes do a good job of measuring the risk/reward behavior of a market sector but have nothing to do with pension liabilities. It is mission impossible for any generic index to measure the unique cash flows of any pension. Only a Custom Liability Index could ever measure and monitor the risk/reward behavior of any pension liability cash flow schedule.

Accounting and Actuarial Reports

Most accounting and actuarial reports are based on an annual fiscal year basis. These tedious and complicated reports usually take months to compile. Such reports usually include a thorough analysis of pension liabilities based on current accounting rules (i.e. ASC 715, ASC 960, PPA, GASB) and actuarial practices (i.e. ASOP 27).

Although these annual accounting and actuarial reports are quite thorough they do not provide the calculations, transparency and frequency needed for proper asset/liability management (ALM). What asset manager could manage assets to an index that comes out annually, months delinquent and you are not provided with the index portfolio. It is rare that the liability cash flow schedule of benefit payments is provided in an actuarial report or CAFR.

Solution: Custom Liability Index (CLI)

Given a liability objective, the first step in a solution is a Custom Liability Index that accurately and frequently measures the size, term structure shape and risk/reward behavior of this unique cash flow. A Custom Liability Index is the proper benchmark for liability driven objectives. The CLI creates a true economic ormarket value measurement of liabilities instead of a single discount rate approach (that is not a market rate) used by most clients today. Since Contributions are the first source to fund benefit payments, the Ryan ALM Custom Liability Index creates a gross and net CLI (after Contributions). Assets need to know what they are funding… net liabilities (after Contributions). Unlike actuarial reports that come out annually and even tri-annually (delinquent), the Ryan ALM Custom Liability Indexes are monthly reports. Our CLI will calculate:

YTM

Duration

Future Value

Present Value

Growth Rate %

Term Structure

Interest Rate Sensitivity

Gross and Net Liabilities

Benefit: Asset Allocation (AA)

Plan sponsors can now know their economic funded status monthly on both a gross and net liability basis. Asset allocation should be based on the economic net liability funded status. A surplus should have a much different AA than a deficit. A deep deficit should have a different AA than a small deficit.

Benefit: Proper Benchmark for Assets

Assets need to know what they are funding… net liabilities (after Contributions). Bonds are best as the core portfolio to cash flow match Retired Lives chronologically. Out Liability Beta Portfolio (LBP) is the proper cash flow matching tool and is explained in our future research topic. This buys time for the Alpha assets to grow and perform vs. the CLI.

Benefit: Performance Measurement

Once the Liability Beta Portfolio is installed to cash flow match Retired Lives chronologically, you now need the Alpha assets to outgrow liability growth to enhance the funded status. The CLI will provide the growth rate of net liabilities just like any index benchmark so performance measurement can be easily assessed.

An error is not a mistake until you refuse to correct it. John F. Kennedy