Ryan ALM

White Papers

Duration vs. Cash Flow Matching

Pension Solutions: Dollar Duration Matching and Cash Flow Matching Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits in a cost-effective manner...

Source: Duration vs. Cash Flow Matching

Pension Solutions:

Dollar Duration Matching and Cash Flow Matching

Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits in a cost-effective manner. Pension management is an assets vs. liabilities objective rather than assets versus generic market indexes objective. Pension asset/liability management (ALM) starts with understanding the pricing and interest rate sensitivity of liabilities and continues with measuring and monitoring such liabilities. There are two primary asset/liability bond strategies in use today: Duration Matching and Cash Flow Matching.

Duration Matching

The purpose of duration matching is an attempt to match the interest rate risk sensitivity of assets to liabilities. The objective is to have the market value or PV changes (growth rate) in the bond portfolio match the market value or PV changes (growth rate) in liabilities for a given change in interest rates. Many fixed income managers attempt to match the average duration of the bond portfolio to the average duration of a bond market index with a similar duration to liabilities (i.e., Bloomberg Barclays long Corporate index). They use the generic bond index as a proxy for liabilities. There are several problems with this strategy.

The fatal flaws in this approach are:

a generic bond index cannot replicate any client’s unique liability cash flows. Client’s liabilities are like snowflakes: different labor force, salaries, mortalities and plan amendments.

average durations give erroneous information because there are an infinite number of combinations of maturities for a bond portfolio that can all have the same average duration, but they will not have the same risk/reward profile.

duration matching is only accurate for small parallel shifts in the yield curve. But the yield curve rarely moves an equal number of basis points at every point along the curve. For more info, Ron Ryan wrote a research paper “The Seven Flaws of Duration” while head of Ryan Labs… see the Ryan ALM website/insights/white papers/classics.

Bond management evolved to remedy these flaws by using Key Rate Durations which attempts to match the duration of multiple points along the yield curve. Key Rate Duration is an improvement over using a single average duration, but it still has several deficiencies:

Actuaries usually do not provide the average duration of liabilities and the projected benefits in their annual actuarial report… reason why generic bond indexes are used.

Matching key rate durations of a generic market index = wrong Key Rate Durations.

Duration is a present value calculation requiring pricing each projected benefit with a discount rate yield curve (i.e., ASC 715 discount rates). As a result, 30 annual benefit payments require 30 separate discount rates.

Duration must be modified (duration/1+YTM) to use as a price return measurement.

Modified duration is a price return measurement and does not include income.

Dollar Duration Matching (DDM)

DDM matches the Dollar Value change per basis point change in yield for assets with the Dollar Value change per basis point change in yield for liabilities. When the Dollar Duration of assets is matched to the Dollar Duration of liabilities for every year in the term structure of liabilities, then DDM is the most precise form of Key Rate duration matching because it matches the Key Rate durations at every point along the liabilities yield cure or benefit payment schedule (30 years = 30 key rate durations). The Ryan ALM approach offers several value-added differences:

Actuarial Projections - We use the actuarial projected benefits of our clients and not a generic bond index.

Modified durations - to be an effective price sensitivity measurement, duration must be modified. Modified Duration measures the percent change in market value or

Dollar duration - our objective here is to match the dollar value change per basis point in assets and liabilities in every maturity on the projected benefit schedule.

The Ryan ALM DDM approach greatly improves the accuracy of Key Rate duration matching by matching the Dollar Value changes in liabilities with the Dollar Value changes in assets across the term structure and yield curve for both assets and liabilities. The liabilities are represented by using a Custom Liability Index to more precisely measure and monitor the dollar value movement in assets versus liabilities given any movement in interest rates.

Cash Flow Matching (CFM)

Ryan ALM believes that the objective for a defined benefit pension is to fund and secure benefits when due in a cost-efficient manner. Ryan ALM does not believe that bonds are performance assets. The value in bonds is in their known and scheduled cash flows which is why cash flow matching has been used as a major strategy for hedging liabilities for many decades (i.e., dedication, defeasance). It is the matching and funding of benefits (future values) that is of primary concern. As such, future values are not interest rate sensitive… a major benefit of cash flow matching. Cash flow driven investing (CDI) dominates the way European pensions are managed under IASB accounting standards. Key Rate Duration using Dollar Duration is great for matching market value (PV) movements between assets and liabilities but what about funding liability payments (future values)?

Since the primary value in bonds is in the certainty of their cash flows, Ryan ALM will cash flow match (fund) projected benefit payments chronologically which provide the plan sponsor with numerous benefits:

Secures the benefits,

Significantly de-risks the plan,

Reduces funding costs significantly,

Reduces volatility of funded ratio and contributions,

Buys time for performance assets (Alpha) to grow unencumbered,

Hedges pension inflation on Retired Lives, Active Lives and Expenses, and

No interest rate risk since LBP is funding future values (benefit payments).

A major cash flow matching benefit is that it buys time for the performance assets to grow unencumbered. History tells us that given time risky assets perform better (i.e., S&P 500). History also tells us if the Alpha assets can grow without any dilution, they perform much better (dividends reinvested > 50% of the S&P 500 growth in the last 50 years). If interest rates rise, cash flow matching can reinvest any excess cash flows at the then higher yields (lower costs) while bonds managed with a purely total return focus would get hurt with lower price returns.

Solutions

Ryan ALM uses a turnkey system approach to asset/liability management for defined benefit pensions:

ASC 715 Discount Rates – Ryan ALM is one of few vendors providing ASC 715 discount rates (AA corporate zero-coupon bonds). We will price each annual projected benefit payment on a monthly basis.

Custom Liability Index (CLI) - Ryan ALM creates a Custom Liability Index (CLI) for each client based on their actuarial projected benefits. We do not use generic market indexes because that would be assets vs. assets. We measure and monitor the performance of assets versus liabilities. The CLI provides all of the calculations needed for either duration matching or cash flow matching. The CLI will calculate YTM, duration, growth rate and interest rate sensitivity for each annual projected benefit as a term structure as well as total liabilities.

Liability Beta Portfolio™ (LBP) – our LBP will cash flow match projected benefits either chronologically or as a dollar duration match using our proprietary LBP cost optimization model that will reduce funding costs significantly.

Whether it is dollar duration matching or cash flow matching, Ryan ALM provides both products as part of our asset/liability management product line. Please contact us to learn how our turnkey system can enhance your pension fund.

Best way to hedge pension inflation

Ronald J. Ryan, CFA, CEO July 2020 Executive Summary Pension inflation is what a plan sponsor agrees to as a cost of living adjustment (COLAs) benefit increase for retired lives...

Source: Best way to hedge pension inflation

Executive Summary

Pension inflation is what a plan sponsor agrees to as a cost of living adjustment (COLAs) benefit increase for retired lives and a salary increase factor for active lives. Quite often, these COLAS are based on the CPI with a floor and a cap or even a % of the CPI while salary increases tend to be quite static @ a 3% annual increase. As a result, pension inflation tends to be less volatile and certainly different than the CPI. Please note that the plan will mismatch the actuarial pension inflation and may introduce

Best way to hedge pension inflation

Many pensions have an allocation to some type of inflation hedge strategy. The most common asset strategies are TIPS and real assets. These strategies are based on hedging or outperforming the CPI. The truth is… these are not appropriate strategies for hedging pension inflation. Pension inflation is what a plan sponsor agrees to as a cost of living adjustment (COLAs) benefit increase for retired lives and a salary increase factor for active lives. Quite often, these COLAS are based on the CPI with a floor and a cap or even a % of the CPI while salary increases tend to be quite static at a 3% annual increase. As a result, pension inflation tends to be less volatile and certainly different than the CPI. Please note that the plan sponsor actuary includes pension inflation (COLAs and salary increases) in their projected benefit payment schedule for both retired and active lives. As a result, the best and, perhaps only way, to hedge pension inflation is to… cash flow match projected benefits! All other inflation strategies (i.e. TIPS and real assets) will mismatch the actuarial pension inflation and may introduce higher cost and fees.

Solution: Cash Flow Match Liabilities

Securing benefits of Retired Lives by matching and funding the projected liability benefit payment schedule (liability cash flows) at the lowest cost is the highest priority of any pension. This is also the ideal way to de-risk a pension plan and hedge pension inflation. Since the actuary includes pension inflation in their liability projections, by cash flow matching the projected liability cash flows (benefit payments) you have hedged pension inflation accurately. There is no other asset strategy that can hedge actuarial pension inflation exactly except insurance annuities which come at a high cost (25% to 40% higher than cash flow matching liability cash flows).

Ryan ALM built a liability cash flow matching product, named the Liability Beta Portfolio™ (LBP), as a cost optimization model that matches and funds the actuarial projected liability benefit payment schedule for retired lives at the lowest cost given the investment policy restrictions of our clients. The LBP portfolio is composed of investment grade corporate bonds skewed to A and BBB corporate bonds since that represents about 89% of the investable investment grade corporate bond universe. Our LBP also accepts and uses high yield bonds if the client investment policy allows.

The LBP provides a 10% to 20% funding cost savings versus the projected benefit payments of retired lives (liability cash flows) and a 20% to 30% cost savings versus using Treasury STRIPS to defease the same liabilities (STRIPS is the discount rate method used by insurance annuities)! This is a serious cost reduction and should be a major consideration of any defined benefit pension plan asset allocation, inflation hedge or de-risking strategy. Yes, the LBP model has some credit risk but very limited since we are using investment grade bonds with several credit filters (to enhance solvency) plus the cost savings provide a large value-added cushion.

We recommend funding the first 10 years of Retired Lives on a net liability basis (after contributions). In truth, current assets fund the net liabilities not the gross liabilities as contributions are the initial funding source of liabilities. Our LBP model will calculate with precision the cost to fund net liabilities chronologically in a cost-effective manner which will de-risk the plan gradually. Since liabilities are funded initially by contributions, using the LBP model to cash flow match net liabilities chronologically may be able to fund more liabilities than you think. Contributions tend to be quite large (especially with many Public plans where actuarially determined contributions are legislated) such that a 10% allocation to our LBP could often fund the next 10-years of net Retired Lives easily.

Matching liabilities chronologically should also buy time for the non-bond assets (Alpha assets) to perform and outgrow liabilities. Given time (10 years) most non-bond asset classes tend to outperform bonds. Since pension liabilities behave like bonds there is a high probability that non-bond asset classes should outperform liability growth over an extended time horizon, especially at today’s low yield on bonds (and liabilities) which would enhance the funded status.

Since the primary pension liability objective is to secure benefits in a cost-effective manner, cash flow matching net liabilities with our Liability Beta Portfolio™ would secure benefits and produce the optimalcost savings.

Asset Allocation (AA)

Pension consultants and plan sponsors should consider installing our LBP as the core portfolio in asset allocation. The best value in bonds is the certainty of their cash flows. Bonds are usually not considered performance assets (Alpha assets) especially versus pension liabilities which behave like bonds. By installing the LBP to fund the first 10 years of net Retired Lives, the pension plan buys time for the Alpha assets (non-bonds) to perform. As the Alpha assets perform versus liability growth, thereby enhancing the funded ratio, such excess returns could be transferred (ported) over to the Liability Beta Portfolio™ (LBP) to de-risk more and more liabilities thereby creating a … Portable Alpha strategy. Had this Portable Alpha discipline been in place during the decade of the 1990s when funded ratios grew to their highest historical levels with true economic surpluses… there would be no U.S. pension crisis today!

Note – The largest U.S. DB pension (CalPERS) removed their 9% asset allocation to inflation hedge assets in 2019.

About Ryan ALM, Inc.

Ryan ALM was founded by Ronald J. Ryan, CFA on July 12, 2004 as an Asset/Liability Management firm. The firm builds a turnkey system of proprietary synergistic products designed to measure liabilities as a Custom Liability Index (CLI) and manage assets to the CLI as Liability Beta Portfolios.

Ryan ALM is unique in having its own proprietary Index company named ALM Research Solutions, LLC. This company builds both custom and generic bond indexes. Such indexes range from Custom Liability Indexes to ETF Indexes.

Our Liability Beta Portfolio™ is our proprietary cost optimization model that "cash flow matches" clients projected liability benefit payment schedules at the least cost using investment grade bonds. It is back-tested since 2009 showing a consistent cost savings of 8% to 15%. Our LBP best represents the core portfolio of a pension plan.

Our team has been recognized for our expertise and results including Ron Ryan having won the William F. Sharpe Index Lifetime Achievement Award.

Cash Flow is King!

Executive Summary Pensions are all about cash flows. They require asset cash flows including projected contributions to fund projected benefits + expenses.Retired Lives are the most imminent and certain liability...

Source: Cash Flow is King!

Executive Summary

Pensions are all about cash flows. They require asset cash flows including projected contributions to fund projected benefits + expenses.Retired Lives are the most imminent and certain liability cash flows and should be the highest priority to fund and secure these benefits.Cash flow matching Retired Lives chronologically with bonds (Beta assets) is the most prudent way to secure these benefits in a cost efficient manner. Unfortunately, most bond assets) who need to grow unencumbered to fund

Pension Solution:

Cash Flow Is King!

The primary objective of a pension is to secure benefits in a cost-efficient manner and then secondarily to enhance the efficiency of the plan’s asset allocation. Securing benefits is all about asset cash flows matching and funding liability cash flows chronologically for 10-years or for as far out as the plan sponsor deems necessary.

Insurance Buyout Annuity (IBA)

Cash Flow Matching (CDI) with bonds

IBA is too expensive for Public and multi-employer plans and unnecessary. Corporations use them to remove the PBGC premium expense on Retired Lives. However, corporations would be wise to compare cash flow matching (Cash Flow Driven Investments or CDI) to IBA. We believe they will find that CDI would reduce funding costs by over 20% in present value dollars versus the future value savings of eliminating PBGC premiums. CDI has been in vogue the longest (since the 1960s) and is a proven way to defease liabilities in a low cost, low risk manner.

It would be wise to separate Retired Lives from Active Lives. The Retired Lives are the most important liabilities since they are the most imminent and known benefits as well as they represent long tenured employees. These are the benefits that need to be secured as best as possible. The Active Lives are the less known and longest liabilities, which allow assets time to grow to fund these benefits.

Since contributions are the first source to fund benefits, current assets fund net liabilities. The actuarial projections of benefits and contributions tend to be annual. Net liabilities are usually not provided by the actuary. Moreover, benefits are paid monthly. Although an easy calculation, it is critical that current assets know what they are funding… monthly net liabilities (projected benefits + expenses – contributions).

It would be wise to separate liability Beta assets from Alpha assets. The Beta assets should be the allocation to bonds to cash flow match net Retired Lives chronologically for a target horizon (we recommend 10 years). Our cash flow matching model (Liability Beta Portfolio™ or LBP) is well tested showing a funding cost savings of 8% to 15% depending on the liability term structure.

It would be wise to take the Cash plus the Fixed Income allocation in your plan’s current asset allocation and apply it to a CDI allocation. This would match and secure benefits chronologically for as far out as the allocation of funds allow. Since we are dealing with net liabilities (after contributions) a 15% allocation may fund liabilities out to 10-years +.

Typically bond allocations are expected to outperform some generic bond index whose cash flows look nothing like the Retired Lives. Moreover, the index benchmark may be skewed to long bonds and Government securities. This introduces interest rate risk and more cost, as yields on government securities are generally the lowest for a similar maturity. Our LBP model is funding benefits (future values) which are not interest rate sensitive. This eliminates the largest risk in bonds. Our LBP model will usually outyield active bond managers by over 50 bps, which will reduce costs. The key value added is the efficiency of the cash flows.

No matter what generic bond index is chosen, active fixed income management cannot produce enough cash flows to fund benefits and expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the core portfolio to fund the shorter Retired Lives net liabilities (1-10 years), the Alpha assets are now free to grow without being diluted or unencumbered to pay any benefits. Alpha assets returns will be volatile, but the Liability Beta Portfolio™ bought the plan time (10 years) for the Alpha assets to grow. The example below shows the cash flow difference of bonds managed to a generic index versus cash flow matching to liabilities:

Assumptions

Bond + Cash Allocation = $150 million (15%)

Net Benefits + Expenses (B + E) = $20 m per year ($200 million for 10 years)

Active bond management vs. generic bond index

YTM = 2.50%

Cash flow = $3.75 million annually ($150m x 2.50%)

Cash flow shortfall = $16.25m annually ($20m - $3.75m)

Requires dilution of Alpha assets cash flow to fund the B + E

Liability Beta Portfolio™

YTM = 3.50%

Cash flow = $20 million annual

No dilution of Alpha assets cash flows

Cash flow = Principal + Income + Reinvestment

Benefits of a CDI Approach

Secures benefits for 10 years

No change in Cash and Bond allocation

No dilution of Alpha assets to fund B + E

No interest rate risk (funding future values)

Outyield active bond management which reduces costs

LBP is skewed to higher yielding A/BBB corporate bonds

LBP has no maturities longer than last benefit payment date

Observations

Generic bond indexes cash flows look nothing like the projected benefit payment schedule of a pension.

This leads to a mismatch of cash flows and risk/reward behaviors… serious issues over time.

Alpha assets need time to perform without any dilution of their cash flows to pay benefits so they shouldn’t be a source of liquidity

CDI funds benefit payments and expenses chronologically

CDI will out yield current bond managers and enhance the ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Logic

Let the performance assets (Alpha assets) perform (grow unencumbered) as the liquidity assets (Beta) assets provide cash flow sufficient to fund benefits plus expenses chronologically.

Was founded by Ronald J. Ryan, CFA on July 12, 2004 as an Asset/Liability Management (ALM) firm. The firm builds a turnkey system of proprietary synergistic products designed to measure liabilities as a Custom Liability Index (CLI) and manage assets to the CLI as a Liability Beta Portfolio™

Our Liability Beta Portfolio™ is our proprietary cost optimization model that "cash flow matches" clients projected liability benefit payment schedules at the least cost using investment grade bonds. It is back-tested since 2009 showing a consistent cost savings of 8% to 15%. Our LBP best represents the core portfolio of a pension plan.

Buy Time!

Executive Summary U.S. pension plans have been hard hit by rising pension costs since 2000. This has been primarily characterized by spiking contribution costs and volatile funded ratios. A solution...

Source: Buy Time!

Executive Summary

U.S. pension plans have been hard hit by rising pension costs since 2000. This has been primarily characterized by spiking contribution costs and volatile funded ratios. A solution to this dilemma is to implement a strategy that will buy time! By separating assets into liquidity (Beta) and performance (Alpha) assets, you can achieve the true objective of a pension, which is to secure benefits. The Beta assets secure Retired Lives benefits chronologically (we recommend 10 years) thereby buying time for the Alpha assets to enhance the funded status, while besting future liability growth.

Pension Solution: Buy Time!

Ryan ALM's mission is to solve liability driven problems through low cost, low risk solutions.

Most pensions have been hard hit this year. According to a March study by Milliman of the top 100 Public Pensions, the average funded ratio fell to 66% from 74.9% at the end of 2019. This represents the largest decline Milliman has ever recorded. The funded status deficit grew to $1.82 trillion. They reported only four plans with funded ratios > 90% and 35% were < 60% funded using the ROA as the discount rate. Imagine the funded ratio if Public Plans adopted FASB discount rates of AA corporates. Lower funded ratios also suggest higher contributions are coming. What to do?

How do you buy time? Cash flow match liabilities for the time you need.

We believe the answer is… BUY TIME!

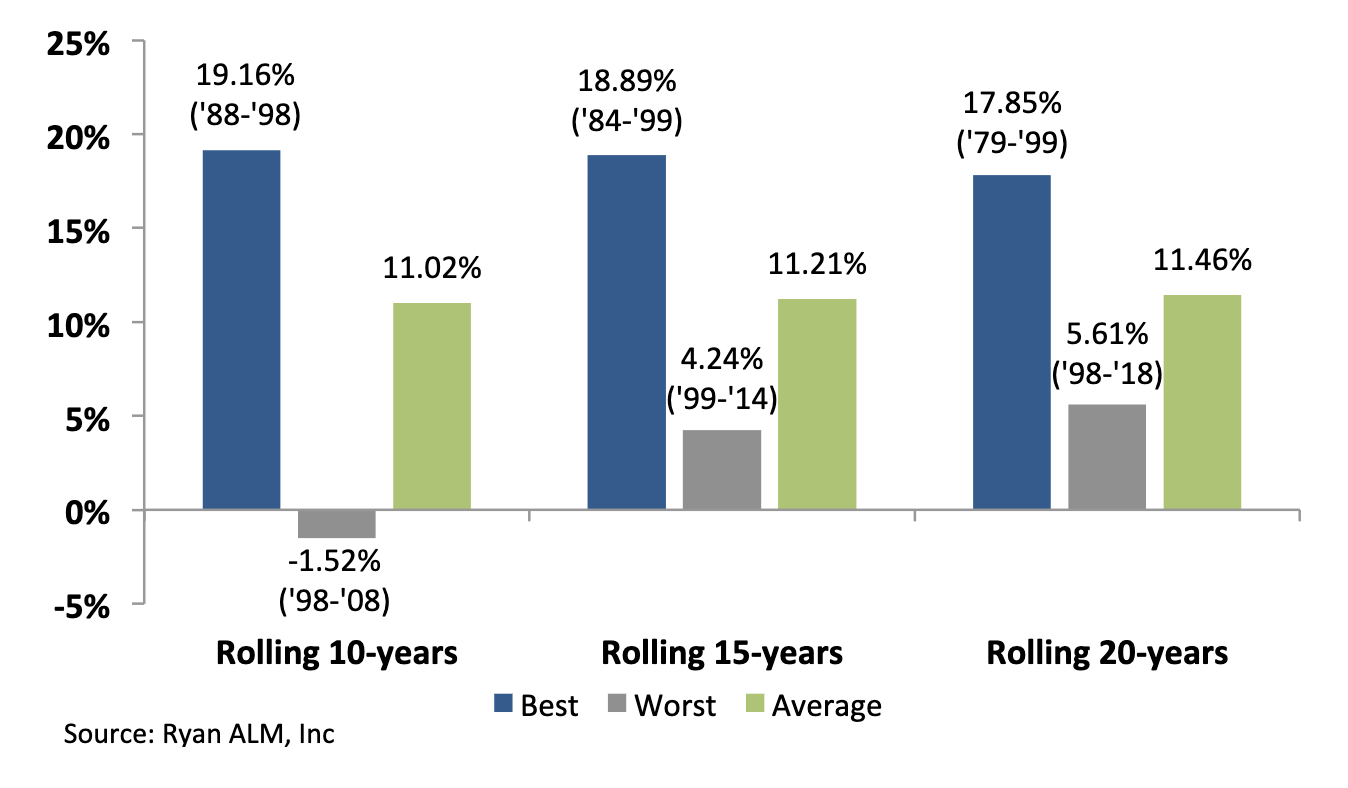

Given time, equities (S&P 500) perform well but they need time. The more time you give equities… the better the returns. Here are historical average S&P 500 return measurements for rolling 10-year, 15-year and 20-year periods ending 12/31/19 over a 50-year horizon starting 1969:

Best, worst, and average returns

So how do you buy time? The answer is… cash flow match liabilities for the time you need. This is best accomplished by transferring the cash + bond allocation assets in kind over to cash flow match net liabilities + expenses. Our cash flow matching model (Liability Beta Portfolio™ or LBP) will calculate with precision the cost to fund net liabilities + expenses in a cost-effective manner chronologically. Since liabilities are funded initially by contributions, using the LBP model to cash flow match net liabilitieschronologically may be able to fund more liabilities than you think. Assume that a 15% bond + 3% cash allocation could match the next 10 years of net Retired Lives benefit payments + expenses chronologically. Based on the Ryan ALM Liability Beta Portfolio™ (LBP) model we show a cost savings (projected benefits – cost of LBP) of about 10% to 15% on cash flow matching the first 10 years of net liabilities (projected benefit payment schedule – projected contributions).

Matching liabilities chronologically should buy time for the non-bond assets (Alpha assets) to perform. Given time (10 years) most non-bond asset classes tend to outperform bonds and the ROA. Since liabilities behave like bonds there is a high probability that non-bond asset classes could outperform liability growth (earn liability Alpha) over an extended time horizon especially at today’s low yield on bonds and liabilities. This would enhance the funded status allowing for reduced contribution costs or increased benefits or both. Our LBP also has numerous benefits that enhance the pension plan:

Secures Benefits

Cash flow match monthly Retired Lives benefits chronologically

Reduces Costs

LBP reduces Contribution, Funding and Asset Management Costs:

(LBP Fee = 15 bps… much less than most active bond managers)

Reduces Volatility

Reduces volatility of Contributions and Funded Ratio

Reduces Risk

Risk = Uncertainty of Funding Benefit Payments

(LBP funds benefits with certainty)

Projected Benefit Payments are Future Values

(FV have NO Interest Rate Sensitive)

Enhances ROA

LBP should out yield most active management bond portfolios

Buys Time

LBP matches & funds liabilities chronologically

Moves deficit out longer extending the investment horizon

Buys Time for Non-bond assets (Alpha assets) to grow

No dilution of Alpha assets to fund benefits

However, most bond allocations are for active bond management versus a generic index benchmark(s). As the designer of the Lehman bond indexes from my days as the Director of Fixed Income Research at Lehman, I can tell you unequivocally that generic bond indexes look nothing like a projected pension benefit payment schedule. Such a mismatch will distort the cash flows and risk/reward behavior of assets vs. liabilities. The major issues and differences are:

Versus Generic Bond Indexes

Does not fund benefits + expenses

Aggregate Index = low yielding @ 1.42%

Generic bond index =/= plan sponsor’s liabilities

Cash flows do not match plan sponsor’s liabilities

Index skewed to long bonds + Government securities

Performance (value added) = small to none (after fees)

Cash Flow Matching (Liability Beta Portfolio™ – LBP)

Custom Liability Index = plan sponsor’s liabilities

LBP funds Net Benefit + Expense payments (monthly)

Performance = immediate funded cost savings of 8% to 20%

But the worst difference and discrepancy is… all about cash flows. Active bond management is focused on outperforming the returns of a generic bond index benchmark. As a result, cash flows are not a consideration. But no matter what generic bond index is chosen; the fixed income assets cannot produce enough cash flows to fund benefits + expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the corebond management is focused on outperforming the returns of a generic bond index benchmark. As a result, cash flows are not a consideration. But no matter what generic bond index is chosen; the fixed income assets cannot produce enough cash flows to fund benefits + expenses. As a result, bonds will require help from performance assets to fund benefits. This will create dilution and disruption of the growth rate of such performance assets. With the Liability Beta Portfolio™ in place as the core portfolio to fund the shorter Retired Lives net liabilities (1-10 years), the Alpha assets are now free to grow without being diluted or unencumbered to pay any benefits. Alpha assets returns will be volatile, but the Liability Beta Portfolio™ bought time (10 years) for the Alpha assets to grow. The example below shows the cash flow difference of bonds managed to a generic index versus cash flow matching to liabilities:

Bond + Cash allocation = $150 million

Net Benefits + Expenses = $20 million per year

Bond management vs. generic bond index

YTM = 2.50%

Cash flow = $3.75 million annual ($2.50% x $150m)

Annual cash flow shortfall = $16.25 million ($20m - $3.75m)

Dilution of Alpha assets cash flow to fund benefits + expenses

Cash Flow Matching

YTM = 3.50% (skewed to A/BBB corporate bonds)

Cash flow = $20 million annual (includes principal + income + income reinvested)

No dilution of Alpha assets cash flows

Observations:

Generic bond indexes look nothing like the projected benefit payment schedule of a pension.

This leads to a mismatch of cash flows and risk/reward behaviors… serious issue over time.

Alpha assets need time to perform without any dilution of their cash flows to pay benefits.

Cash flow matching funds benefit payments chronologically

Cash flow matching will out yield current bond managers and enhance ROA

Cash flow matching buys time for Alpha assets to grow unencumbered

Logic

Let the performance (Alpha) assets perform (grow) as the liquidity (Beta) assets provide cash flow sufficient to fund benefits plus expenses over a time horizon sufficient to let the Alpha assets grow unencumbered.

The Role of Bonds in Pension Asset Allocation

Custom Liability Index (CLI) The first step in prudent pension management is to install a Custom Liability Index (CLI) to calculate and monitor the present and future value term structure,...

Source: The Role of Bonds in Pension Asset Allocation

Custom Liability Index (CLI)

The first step in prudent pension management is to install a Custom Liability Index (CLI) to calculate and monitor the present and future value term structure, growth rate and interest rate sensitivity of the plan’s liabilities. The CLI is the proper benchmark for any pension defined benefit plan. It is based on the actuarial projections of the future benefit payment schedule. The CLI will produce all of the critical calculations needed to manage and understand a pension: future value, present value, yield, duration, growth rate, term structure and interest rate sensitivity. Since contributions are the initial source to fund liabilities, current assets truly fund the net liabilities (after contributions). As a result, there needs to be both a gross and net CLI to show the significant differences in future values, present values, yield, duration, growth rates and interest rate sensitivity. It is rare to find a CLI installed in most pensions which leads to a misalignment of assets vs. liabilities. Beware of custom indexes that are a blend of generic bond indexes… where are the client’s liabilities? Ron Ryan created the first CLI in 1991 and Ryan ALM is a leader in providing CLIs to plan sponsors. We will price the CLI at any discount rate the client prefers: ASC 715, ROA, PPA, Treasury STRIPS. Since Moody’s has adopted the ASC 715 discount rates (zero-coupon AA corporates) for Public pensions and FASB uses ASC 715 discount rates for corporations, the ASC 715 discount rates would be the logical choice to calculate liability present value to understand the true economic funded status and liability growth rate.

Asset Allocation (AA)

Asset allocation is the single most important asset decision since it affects all assets. The goal of AA is to enhance the funded ratio and funded status in a cost-effective manner with prudent risk. AA should be based on the funded ratio and funded status not the ROA. A pension plan with a surplus should have a radically different asset allocation than a plan with a major deficit. Yet if these two plans had the same ROA (return on asset assumption) they would most probably have the same asset allocation… totally inappropriate! Note once again, assets fund the net liabilities (after contributions). So it is the net liabilities that should be used to calculate a net funded ratio and funded status which drives the AA. It is this net funded ratio and funded status that should be the focus of asset allocation. It is critical that current assets know what they are funding… net liabilities!

Funded Ratios History

Most pensions had a surplus in the 1990s. Prudent fiduciary responsibility should have secured this surplus through an asset liability matching (ALM) strategy using bonds (i.e. cash flow matching, defeasance or immunization). But since bond interest rates were low and trending lower, asset allocation models went the other way and reduced their allocation to bonds consistently and skewed their allocation to more and more risky assets (i.e. equity) in an attempt to achieve the ROA. This became a fatal mistake as funded ratios eroded by about 50% in the 2000-2002 equity correction period and have stayed in a deficit position ever since. The old adage, “if you go down 50%, you have to go up 100% to get back to 0%”... rang true in pensions. Had asset allocation been responsive to the rising funded ratio in the 1990s, it would have transferred more and more assets to bonds in an ALM strategy. Moreover, there was no anchor or core portfolio to de-risk the plan (ALM strategy) that would have significantly reduced the volatility of the funded ratio and secured the surplus.

De-Risking a Pension

Pension plans should want to de-risk their plans consistently over time. The lowest risk assets for a pension are those that match the liability benefit payment schedule (future values) with certainty. By definition, Treasury zero-coupon bonds (STRIPS) and annuities would be the lowest risk assets for pension since they have a known future value… but they tend to come at a high cost since they are low yielding and have high fees (annuities). Given that the pension objective is a liability objective with cost constraints, then solving for cost while matching the liability benefit payment schedule would be the ideal way to de-risk a pension. This is best accomplished thru a cash flow matching strategy. A pension liability benefit payment schedule is a term structure or yield curve often referred to as the liability cash flow. In order to match or de-risk the liability cash flow requires a matching cash flow from assets. Basically, only bonds and annuities produce a certain cash flow. That is why bonds and annuities are preferred as the way to defease, immunize and de-risk a pension plan.

Problem: Immunization Strategies (Duration Matching)

The initial problem with duration matching is where do you get the duration of each client’s liabilities. The actuary does not calculate and provide the average duration of liabilities in the annual actuarial report. Most, if not all, duration matching strategies use a generic bond market index as the proxy for liabilities. How could one generic index represent each unique pension plan? Pension liabilities are like snowflakes, you will never find two alike… different labor force, salaries, mortality, plan amendments, etc. The difference in liability cash flows and durations could be quite significant. For every year you are off in duration, should represent a 1% difference in liability growth per 100 bp move in the discount rates. Without a custom liability index, duration matching is a futile effort.

Imagine a 12-year average duration liability benefit payment schedule. It could have many different term structure shapes to come up with an average 12-year average duration. Imagine a bond portfolio where 100% of the bond assets have a 12-year duration. If interest rates rose 50 basis points in a year the total assets and liabilities supposedly would both have a -6% price return (interest rate movement x duration (as a negative number)). If they had the same income return = 4% they would match again (note that assets usually don’t match the income or yield of liabilities). However, if the matching assets are used to fund the liability cash flow of annual benefits then a -2% loss (-6% + 4% = -2%) on assets could be funding a one-year liability which should have a small positive growth rate. Consequently, the assets could be taking a loss each year to fund the next liability payment if interest rates continue to rise. This could be a serious costly mismatch if interest rates began a secular trend to higher rates for the next five years. But the point is… there is no cash flow match of the liability term structure, only a duration match of total liabilities so there is serious funding risk!

Imagine another duration matching approach where you buy bonds that exactly match the duration of each liability payment. So you would buy a 3-year duration bond to fund a 3-year benefit payment, a 5-year bond to fund a 5-year benefit payment, etc. Using corporate bonds to duration match is difficult, if not impossible. First, there are no corporate zero-coupon bonds. Second, the duration of a coupon bond changes with interest rates so if interest rates go down the durations should go up and vice versa. This is not compatible with funding each benefit payment as they come due over time since liabilities behave like zero-coupon bonds. Third, duration matching does not match or fund each benefit payment (the benefit payment schedule). Last, there are no corporate coupon bonds whose durations exceed 16-years so you are forced into Treasury STRIPS to fund liabilities past 16 years. Treasury STRIPS will certainly match these longer liabilities but come at a high cost. You want to buy longer bonds whose cash flows match the liability benefit payment schedule but at a much lower cost. This requires long coupon bonds which would create a duration mismatch.

Interest rate swaps and futures (derivatives) are another immunization strategy. They are contracts not true assets. There is no cash flow or funds available to make the liability cash flow payments. They are certainly NOT de-risking strategies but hedges vs. the liability growth rate. In fact, these strategies introduce more risk: counter party risk, interest rate risk, non-matching risk of assets purchased (usually equities) vs. liabilities and leverage. In addition, interest rate swaps and futures have all of the problems associated with a liability duration proxy… as listed with duration matching.

Problems with Insurance Buyout Annuities (IBA)

The buyout annuity is certainly the least risky approach to de-risking a pension but it comes at the highest cost. The current trend is to price liabilities at the Treasury STRIPS yield curve and create a single discount rate (i.e. 3.00%) + a fee of around 4%. The plan sponsor would have to transfer assets and funds over to the insurance company such that the plan is fully funded (or even up to 105% funded) at this single discount rate.

The insurance buyout annuity should be more costly than defeasing the plan with Treasury STRIPS which was always considered the high cost de-risking strategy. Defeasance with Treasury STRIPS should also allow an accounting removal of the pension liability debt. Since the primary pension objective is to fund liabilities at low and stable costs, the buyout annuity should be given a second thought before executing. In addition, if the insurance company goes bankrupt there may be a claw back of pension liabilities to the plan sponsor.

Solution: Cash Flow Matching

As stated in the beginning, matching the liability benefit payment schedule (liability cash flow) at the lowest cost is the ideal way to de-risk a pension plan. Ryan ALM spent two years building a liability cash flow matching product, named the Liability Beta Portfolio™ (LBP), as a cost optimization model that matches the liability benefit payment schedule at the lowest cost given the investment policy restrictions of our clients. Based on the same sample benefit payment schedule used above for the buyout annuity vs Treasury defeasance comparison, our LBP model shows a 26.84% funding cost savings vs. the buyout annuity and 26.54% vs. STRIPS! This is a serious funding cost reduction and should be a major consideration of any de-risking strategy. Yes, the LBP model has some credit risk but very small since we are using investment grade bonds only. The funding cost savings + the extra yield vs. liabilities annually (@100 bps) provide a large value-added cushion vs. any credit problems. Since our LBP is matching and funding the liability benefit payment schedule (future values), there is no interest rate risk since future values are not interest rate sensitive.

The funded ratio should dictate the allocation to bonds. A surplus should have a high allocation to bonds matched to liabilities and vice versa for a deficit funded status. Unfortunately, asset allocation did not respond to the surplus status in the 1990s which led to the US pension crisis. I wrote a book “The U.S. Pension Crisis” detailing the causes and solutions of this enormous financial crisis. With funded ratios at 120% to 150% in the 1990s, why didn’t pensions de-risk their plan (cash flow match) and secure this victory? Because pensions were focused on achieving the ROA (return on asset assumption) instead of focusing on the funded ratio and status, they reduced their bond allocations when bond yields went below the ROA… around 1988. Amazingly, instead of increasing their bond allocation in response to a growing funded ratio they reduced it consistently to the lowest bond allocations in modern history by 1999. The equity correction of 2000-02 erased pension surpluses and created severe deficits that most pensions have not recovered from with spiking contribution costs ever since 2000.

Based on the allocation to bonds should determine how much of the liabilities we can cash flow match (i.e. 25% bond allocation could fund the next 10 years of net liabilities). Most current bond allocations are historically low. As a result, you cannot match and de-risk 100% of liabilities with a 25% bond allocation, especially if you have a funded status deficit. Such a 25% allocation could be used to match and de-risk either a % of total net liabilities or net liabilities chronologically… both methods will de-risk the plan gradually. There are advantages for each method.

Since liabilities are funded initially by contributions, using the LBP model to cash flow match net liabilities chronologically may be able to fund more liabilities than you think. Assume that a 25% bond allocation could match the next 10 years of net liability payments chronologically. Based on the Ryan ALM Liability Beta Portfolio™ (LBP) model we show a funding cost savings of about 4% to 6% on cash flow matching the first 10 years of liabilities versus the ASC 715 discount rate (AA corporate zero-coupon bonds). Note that Ryan ALM is one of few vendors who provide the ASC 715 discount rates since 2008. Our discount rates are consistently higher than the Citigroup rates providing a lower present value on liabilities and enhancing funded ratios and balance sheets. Price Waterhouse has been a subscriber to our ASC 715 discount rates since 2008.

Matching liabilities chronologically should also buy time for the non-bond assets (Alpha assets) to perform and outgrow liabilities (as measured by the CLI). Given time (10 years) most non-bond asset classes tend to outperform bonds. Since liabilities behave like bonds there is a high probability that non-bond asset classes should outperform liability growth over an extended time horizon especially at today’s low yield on bonds (i.e. liabilities).

Since the pension liability objective is also a cost focus, cash flow matching a % of total liabilities would produce the optimal funding cost savings since the longer the bond the less it costs given the same future value. Our LBP model is back tested since 2009 showing a cost savings of 8% to 12% on cash flow matching a % of total net liabilities. For every $1 billion in bonds used in our LBP model could save about $100 million in cost savings vs. the ASC 715 present value of liabilities.

Core Bond Portfolio (De-Risk)

Pension consultants and plan sponsors should consider installing a LBP as the core portfolio in asset allocation. This would gradually de-risk the plan and facilitate portable alpha asset allocation. The best value in bonds is their cash flows. Bonds are usually not considered performance assets (Alpha assets) especially vs. pension liabilities which behave like bonds. The P&I performance study has proven for decades that fixed income managers have little or no value added vs. bond index benchmarks (after fees).

Given no change in the bond allocation… replace high fee active bond management with a LBP that will de-risk the plan, reduce funding costs and reduce contribution volatility at a low asset management fee (@ 12 bps). As the Alpha assets (non-bonds) perform vs. liability growth (as measured by the CLI), thereby enhancing the economic funded ratio, such excess returns (liability Alpha) should be transferred over to the Liability Beta Portfolio™ (LBP) to de-risk more and more liabilities… Portable Alpha. Had this portable Alpha discipline been in place during the decade of the 1990s when funded ratios grew to their highest historical levels with true economic surpluses… there would be no U.S. pension crisis today!

Nota Bene (Note Well)

Please note that the definition of risk used in this research report is in sharp contrast to the traditional approach produced by the Nobel Prize winner Ph.D. William F. Sharpe back in 1966. Professor Sharpe proposed that risk is the volatility of total returns and that the three-month T-Bill was the default risk-free rate. He developed the Sharpe Ratio as a means of calculating the risk-adjusted return by subtracting the return of the three-month T-Bill from the mean return of the assets being analyzed and dividing the net return by the volatility of the return of the assets in review. For many decades the Sharpe Ratio was the standard measurement of risk-adjusted returns. In 1994 Prof. Sharpe called me and invited me to Stanford to discuss our unique custom liability index data and index reports. I had the unique pleasure to meet and debate with one of the finest intellects I ever met.

I proposed that risk is not a generic measurement but based on each client’s objective. I referenced pensions where every client’s liabilities are different (like snowflakes). As proof, I asked him what is the risk-free asset for a 10-year liability payment? Prof. Sharpe answered… a 10-year Treasury zero-coupon bond that matches the liability payment with certainty. Prof. Sharpe identified that the three-month T-Bill would have 39 reinvestment moments of uncertainty, so there is no way the three-month T-Bill could match a 10-year liability future value with any certainty and would become a risky asset. Our discussion led to Prof. Sharpe re-inventing the Sharpe Ratio in 1994 to include the benchmark objective instead of the three-month T-Bill in the numerator and denominator such that the average return of the asset portfolio is reduced by the average return of the objective (numerator). This net average return is then divided by the standard deviation of the asset portfolio return vs. the objective return (tracking error). This is commonly called today… the Information Ratio.

The Smartest Beta

The term “beta” is credited to William F. Sharpe, Ph.D. in his 1964 work in development of the “Capital Asset Pricing Model (CAPM)”. It means (1) the covariance of the...

Source: The Smartest Beta

The term “beta” is credited to William F. Sharpe, Ph.D. in his 1964 work in development of the “Capital Asset Pricing Model (CAPM)”. It means (1) the covariance of the return on a security or portfolio with that of the market portfolio divided by (2) the variance of the return on the market portfolio. Professor Sharpe originally called this “market sensitivity” since you are comparing an investment to the market as defined by a market index. A beta of 1.0 suggests you have no residual risk in that you match the risk/reward behavior of the market index you are being compared against. Ideally, a market index fund should consistently have a market beta of 1.0.

Beta is a measurement based on a market or objective index. Without the index benchmark there is no applicable beta calculation. Traditionally, this has been the popular index benchmarks (i.e. S&P 500, Lehman Aggregate, etc.) but in truth it can be any index that best represents the objective of such funds (i.e. ETFs, index funds). Back in 1964 there was the absence of market indexes so beta was limited mainly to a measurement versus the S&P 500. The first bond index was introduced by Kuhn Loeb in 1973 (merged into Lehman in 1977). Since the advent of ETFs in 1993 there has been numerous new indexes created to feed the explosive growth of ETFs. Such new indexes are the stated objective of these many new ETFs.

Smart Beta

Smart beta is the optimization of the risk/reward behavior of a market index usually by changing the weights. Popular smart beta weighting schemes have been: fundamental weighting, equal-weighting, risk-clusters, and diversity weighting (combines equal and cap weighting). By changing the weights methodology the goal is to enhance returns or reduce volatility or both. Smart beta products have grown well in a short period of time but for the most part are still equity index derivatives. Rob Arnott and Research Affiliates, LLC have been a leader here introducing fundamental weighting for both bond and stock indexes as risk/reward value-added.

There is debate as to whether changing the weight methodology of a market index is really active management or an alpha strategy rather than a beta strategy or discipline. My recommendation is that the objective decides what is beta and alpha. What is important is to have the objective defined by a rules based index. If this reweighted index is the stated objective of an ETF, mutual fund or client then beta is the portfolio that matches the risk/reward of this objective index version. It also follows that alpha is the excess return versus this modified index objective. All comparisons to the traditional generic market index are just good information to know but do not determine the alpha and beta calculations.

Liability Beta Portfolio (The Smartest Beta)

The “smartest beta” portfolio is the portfolio that best matches and achieves the true client objective with the least amount of risk and cost. Risk is best measured as the uncertainty of achieving the objective. Cost is the amount required to fund the objective. The true objective of most institutions and even individuals is some type of liability (annuities, banks, insurance, lotteries, NDT, OPEB, pensions, etc.). The absolute level of volatility of returns is not risk given a liability objective. Indeed a 10-year liability payment is best matched and funded (defeased) by a 10-year Treasury STRIPS which has a certain future value. A three month T-bill would be very risky given this liability objective as it has 39 reinvestment moments of uncertainty. Although the 10-year Treasury STRIPS would be much more volatile in returns, such a return pattern would match the present value behavior of the 10-year liability and thus be low risk or even risk-free (defeasance).

Given a liability objective it is critical to create a custom liability index (CLI) as the proper benchmark. It must be a custom index since liabilities are like snowflakes… you will never find two alike. The CLI is a portfolio of liability payments weighted by the schedule of payments (term structure). Most institutional liabilities are calculated by actuaries who produce an actuarial projection of the liability payment schedule for each client. As such, the CLI is weighted by the actuarial projection in present value dollars. To calculate the present value of each liability payment you need to price liabilities based on a yield curve of discount rates. Depending on the type of liability there are accounting rules (ASC, FASB, GASB, IASB, PPA, etc.) that dictate the discount rate methodology.

Most, if not all, liabilities are priced as zero-coupon bonds since they produce a certain future value. Using U.S. corporate pensions, as an example, they are regulated by ASC 715 (formerly FAS 158) for GAAP accounting purposes. These rules suggest pricing liabilities as if they were AA corporate zero-coupon bonds. Since such bonds are not available in the bond market, they have to be manufactured as hypothetical zero-coupon bonds. As a result, liabilities behave like a yield curve of zero-coupon bonds weighted by the actuarial projections. This means that pension liabilities are extremely interest rate sensitive.

The CLI should calculate all of the necessary statistics to maintain and monitor a liability beta portfolio: term structure weights, total present value, YTM, duration, growth rate, interest rate sensitivity. The CLI is also the proper benchmark to measure liability alpha. If equity assets outperform the S&P 500 but underperform the CLI growth rate… did you earn alpha? In the eyes of the client you lost to liability growth which will damage the funded ratio

(assets/liabilities), credit rating and increase contribution cost. Liability alpha is the excess return versus the CLI return (growth rate) and not versus a market index return. Based on Ryan ALM indexes, liability YTD returns through November 30 should be between 12.7% (10-year duration) and 22.2% (15-year duration). Hard to believe that any pension has earned liability alpha so far in 2014.

The key point here is that the client objective is truly the focus and determinant of relative risk and reward (beta and alpha). The client objective is to fund liabilities in such a way that risk and cost are reduced and stable over a long horizon. Given a long average life (duration) based on the liability payment schedule then the liability beta portfolio needs to match these term structure weights. An S&P 500 index fund or any generic market index fund could never represent the beta portfolio for a liability driven objective. Cash or a money market fund is a very risky investment for most liability objectives that have long average lives (duration).

The most appropriate and smartest beta portfolio is the one that matches the liabilities cash flow as measured by the CLI. In essence, the smartest beta portfolio is a custom liability index fund. Such a portfolio should be the core portfolio for any liability objective. By matching the liability term structure the uncertainty risk of matching liabilities is eliminated and interest rate sensitivity is neutralized. By matching the liability term structure with bonds that have higher yields and lower present values (price) than the discount rates used… you have reduced costs. Since the accounting rules (ASC 715, IASB, and PPA) use AA zero-coupon discount rates then a liability beta portfolio of A and BBB will produce higher yields and lower costs. This should provide significant cost savings of 10% to 15%. This matching process is called cash flow matching. Beware of duration matching strategies (i.e. immunization) which do not match the liability cash flows but just the average duration. This is not an accurate or cost effective way to match liabilities. The smartest beta portfolio is a liability cash flow matched portfolio!