Ryan ALM

White Papers

Browse

Operation Home Run

Pension Solution: Operation Home Run The true objective of a pension is to secure and fully fund benefits in a cost-efficient manner with prudent risk . This is best accomplished...

Source: Operation Home Run

Pension Solution:Operation Home Run

The true objective of a pension is to secure and fully fund benefits in a cost-efficient manner with prudent risk. This is best accomplished through a cash flow matching (CFM) strategy using investment grade bonds to fully fund and match monthly benefit payments at low cost. CFM has several advantages of which we label four as “Operation Home Run”:

1.Liquidity

Liquidity is a critical and necessary priority of a pension since it must fund monthly benefits + expenses (B + E) on time. Many plan sponsors use a “cash sweep” or a cash allocation strategy to provide such cash flow. Both strategies are not optimal for a pension plan. A cash sweep usually takes income or cash flow from all asset classes to fund the current monthly B+E. This can severely damage the ROA of such asset classes. According to a research report by Guinness Global since 1940, dividends and dividends reinvested have accounted for 47% of the S&P 500 total return on a 10-year rolling period and 57% on a 20-year rolling period. So, this data questions the logic of a cash sweep that uses dividends to fund benefits + expenses (B+E). A cash allocation is usually low yielding + is close to a 1:1 relationship between present value and future value which is high cost. CFM will fully fund monthly B+E in a cost-efficient manner with yields of the average duration of the CFM.

2.Security

Pensions need to secure the benefit payments as a high priority. This is best accomplished through CFM which has the certainty of asset cash flows that fully fund liability cash flows on time with the correct amount. To our knowledge only bonds and annuities have certain cash flows. This is why bonds have been chosen as the appropriate securities to defease liability cash flows for decades.

3.Time

The greatest asset of a pension is time. Most pensions have long average lives. The best way to buy time is with a CFM strategy that will defease liabilities for as long a period of time as the plan sponsor wants. S&P data proves that the longer the time horizon the higher the total return of stocks… and most risky investments. Ryan ALM recommends a CFM strategy to fund at least 1-7 years.

4.Cost

The pension objective is a liability objective and cost objective. Since liabilities are future value costs, only a CFM or annuity strategy could fund liability cash flows with certainty. The Ryan ALM CFM model will reduce funding costs by about 2% per year (20% for 1-10 years of liabilities).

Conclusion

As a best-fit to achieve the true pension objective, Ryan ALM recommends our cash flow matching (CFM) strategy to fully fund B+E in a cost-efficient manner. Our CFM model will provide timely cash flows that will fully fund B+E at the lowest cost to our clients. The benefits of our CFM model are quite substantial:

CFM will provide certainty of cash flows which eliminates liquidity risk.

CFM secures the benefit payments through the certainty of its cash flows.

CFM buys time. The longer the time, the greater the ROA for the growth assets.

CFM is a cost optimization model that reduces funding costs by about 2% per year.

CFM is an investment grade portfolio skewed to the longest maturities within the area it is funding (i.e. 1-5 years or 1-10 years) that should enhance the CFM yield versus the yield on cash reserves and active bond management.

CFM reduces reinvestment risk if interest rates trend downward (as many expect).

As a solution, Ryan ALM recommends separating liquidity assets from growth assets in asset allocation. Let bonds in a CFM strategy be your liquidity assets for the advantages mentioned above. A CFM strategy will have a longer average duration and higher yield than cash thereby reducing the cost to fund B+E. In this way the liquidity assets and the growth assets are a team that will produce the optimal solutions.

Ryan ALM Pension Alert Q2’23

Most Asset Allocations for pensions are based on achieving the ROA. The ROA is an annual forecast of asset returns. Each asset class is assigned a ROA then weighted by...

Source: Ryan ALM Pension Alert Q2’23

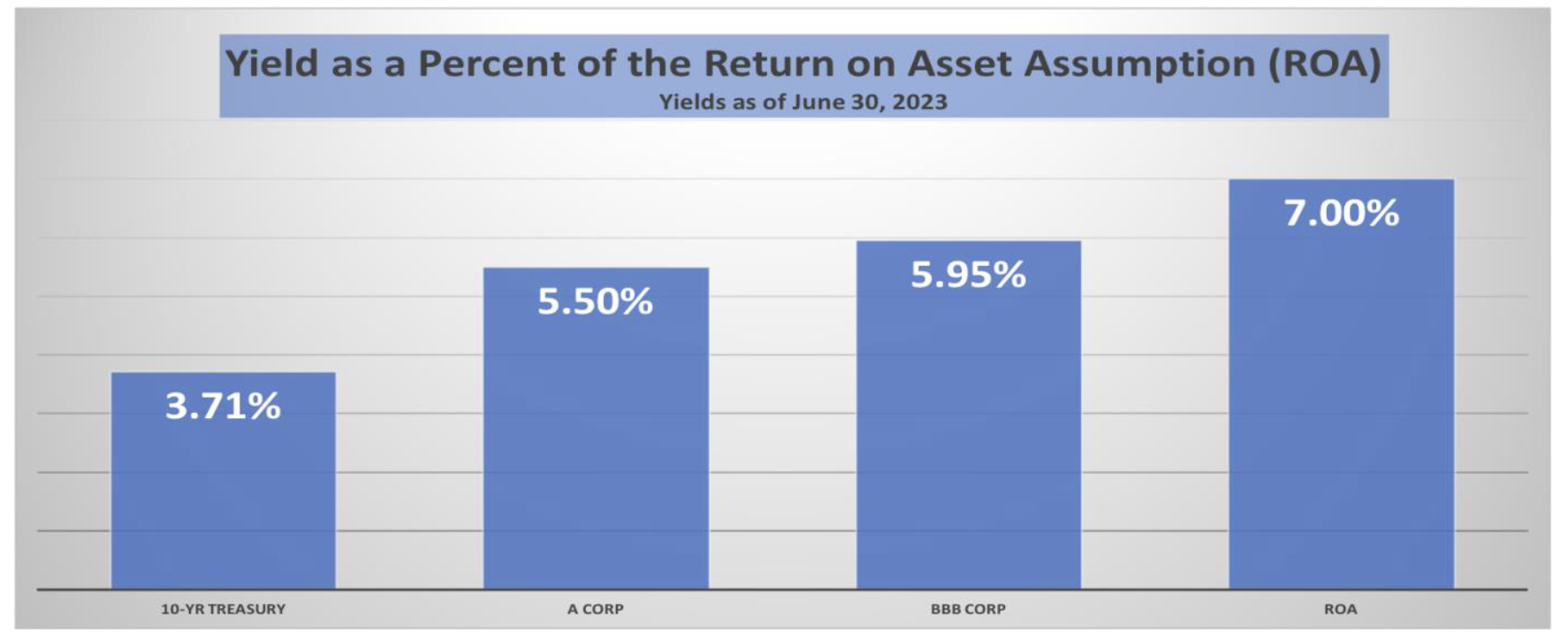

Spread between ROA and Bonds Narrowest in 20+ Years

Most Asset Allocations for pensions are based on achieving the ROA. The ROA is an annual forecast of asset returns. Each asset class is assigned a ROA then weighted by the target allocation to get an average or target ROA. Currently, the ROA for most Public pensions is around 7.00%. Yields on A and BBB corporates have risen significantly in the last two years and are now fast approaching the ROA target return. With A and BBB corporate yields at 78.6% to 85.0% of the ROA, a strong argument should be made to increase the allocation to fixed income. The 2023 Milliman Public Funding Survey suggests that the ROA will continue its trend lower. With the Milliman 2024 estimate of a 6.75% ROA, A and BBB corporate bonds would approach 81.5% to 88.2% of the target return. Ryan ALM recommends using bonds for their intrinsic value… the certainty of their cash flows. Cash flow matching liabilities chronologically would be in harmony with the true objective of a pension… to secure the promised benefits in a cost-efficient manner with prudent risk.

Benefits of Higher Bond Allocation to Cash Flow Matching:

Improve Liquidity

Outyield ROA = liability Alpha

Reduce Volatility (risk) of Funded Ratio

Create CORE portfolio as anchor to earning ROA

Reduce costs to fund Benefits + Expenses (B + E)

Buy TIME for performance assets to grow unencumbered