Ryan ALM

White Papers

Magnificent 7: Caveat Emptor!

As pension watchdogs, Ryan ALM is always interested and concerned about trends that may affect the funded status of pensions. Since the major asset holding of most pensions is the...

Source: Magnificent 7: Caveat Emptor!

As pension watchdogs, Ryan ALM is always interested and concerned about trends that may affect the funded status of pensions. Since the major asset holding of most pensions is the S&P 500, we are on the alert for anything that may affect this valuable asset. I recently attended a CFA dinner where Rob Arnott, founder and chairman of Research Affiliates a subdivision of PIMCO was the guest speaker. Rob is quite articulate and brilliant on his assessments and forecasts. He was concerned about the valuation of the Magnificent 7 and thought the P/E multiples may not be sustainable. I share Rob’s concerns for the following reasons.

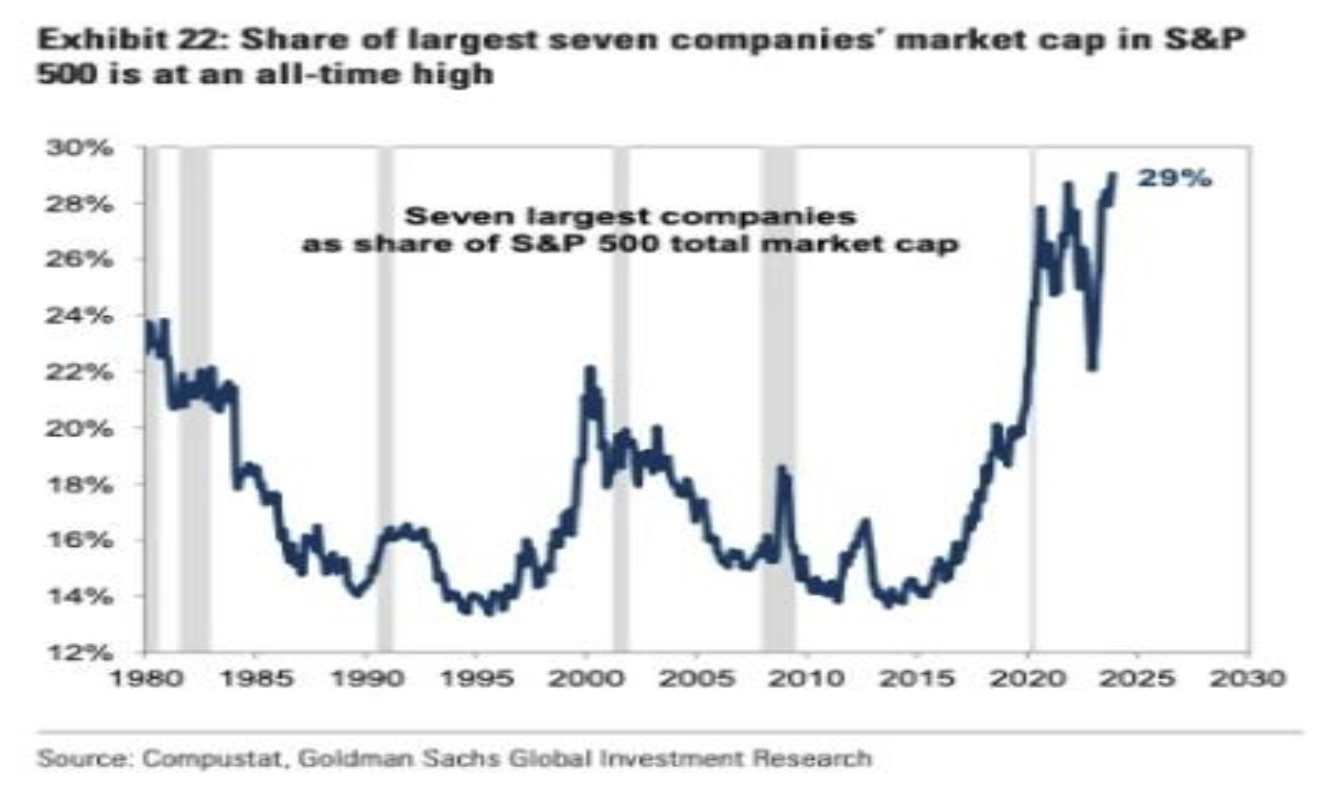

Apple became the first $3 trillion market valuation in America’s history. The seven largest capitalized technology stocks (i.e. the Magnificent 7) have been the main driver of returns for the S&P 500 for several years and certainly in 2023 YTD. As of December 1, this group had a total return = 98.79% based on the Bloomberg Magnificent Seven equal weighted index. At the same time the S&P 500 has a YTD return of 20.96%. According to BOA Global Investment Research, the Mag 7 account for 29.6% of the S&P 500 market capitalization. The newly released Bloomberg Large Cap index without the Magnificent 7 (B500XM7T) posted a YTD return of 7.6% which is 36.4% of the YTD S&P 500 return of 20.96%. This means that the Mag 7 has a YTD weighted group return of 13.33% which accounts for 63.6% of the S&P 500 YTD return (as of 12/01/23).

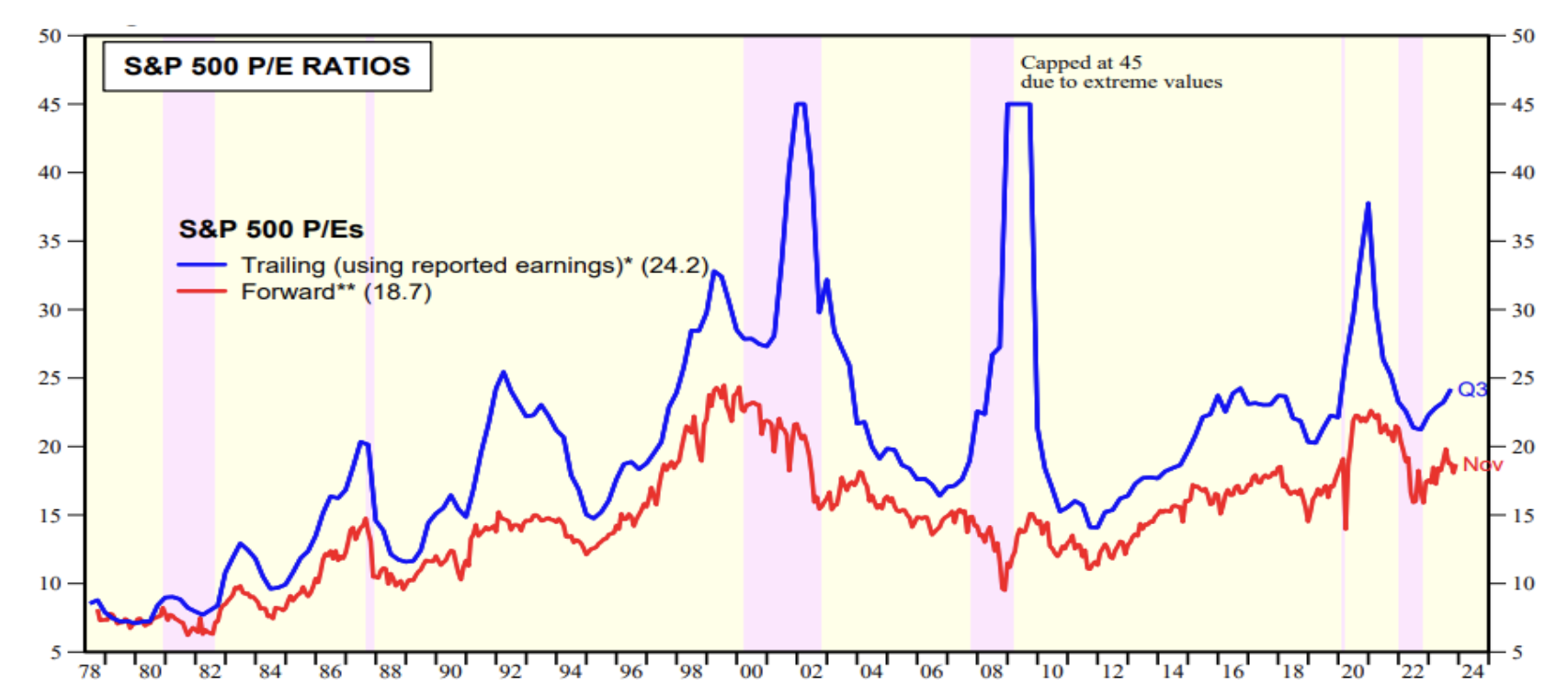

The Mag 7 should continue to grow well given their product line, market share, higher sales growth, higher margins, strong balance sheet and greater re-investment ratio in their market. The main question is one of valuation. Although it may be hard to assess a proper P/E multiple for each of the Mag 7, the wide array of P/E multiples and comparison to the market seem quite overvalued… S&P 500 multiple = 24.2x current and 18.7x forward (source: Yardeni). Tesla at 76.9x current/61.7x forward seems hard to justify especially with earnings growth of -6.1% over the last 12 months. Alphabet, Apple, Meta and even Microsoft trailing 12 months EPS growth do not seem robust enough to merit their valuation either.

| Stock Symbol | Company | PE current | PE forward | Market Capitalization | EPS Growth 5-year Avg. | EPS Growth Last 12 mos. |

|---|---|---|---|---|---|---|

| GOOG | Alphabet | 25.38x | 19.80x | $1.66 trillion | 25.4% | 3.4% |

| AMZN | Amazon | 76.69x | 41.03x | $1.52t | 63.0% | 74.1% |

| AAPL | Apple | 31.55x | 27.16 | $3.01t | 14.4% | 0.3% |

| META | META | 28.10x | 18.17x | $0.82t | 8.9% | 3.1% |

| MSFT | Microsoft | 36.08x | 28.76x | $2.77t | 18.4% | 10.5% |

| NVDA | Nvidia | 61.48x | 22.61x | $1.15t | 27.7% | 264.5% |

| TSLA | Tesla | 76.87x | 61.72x | $0.76t | 40.5% | -6.1% |

| S&P 500 | 24.2x | 18.7x | $37.7t |

Goldman Sachs Global Investment Research is forecasting a 6% growth for 2024 for the S&P 500. This does not validate the P/E multiples of the S&P 500.

“Investors should be skeptical of history-based models. Beware of geeks bearing formulas”

Warren Buffett

Greatest Asset of a Pension… TIME!

I recently spoke at the FPPTA conference in Orlando on pension risk management. One of the speakers was Mike Welker, CEO of AndCo Consulting, who I thought had the most...

Source: Greatest Asset of a Pension… TIME!

I recently spoke at the FPPTA conference in Orlando on pension risk management. One of the speakers was Mike Welker, CEO of AndCo Consulting, who I thought had the most incisive comment of the conference. Mike said,“the greatest asset of a pension is time.” He was referencing that pensions have a long-time horizon to work in… perhaps, perpetuity. With such a long horizon, short-term distractions and corrections should not make a pension detour from its long-term goal and strategy. Mike is very right.

Ryan ALM believes that the best way to buy time is to cash flow match a pension plan’s liabilities chronologically. Almost any performance return study on asset classes shows that given time most, if not all, asset classes perform in line with their return and risk expectations. We’ve also observed that pension plans generally sweep cash from all asset classes each month to fund current benefits and expenses (B + E). We urge plan sponsors not to provide liquidity in this way, as S&P 500 data suggests that 47% of the S&P 500 index returns come from dividends and the reinvestment of dividends over 10-year rolling periods since 1940.

We urge plan sponsors and their consultants to separate liquidity assets from growth assets. Let bonds be the liquidity assets. Let bonds fund B + E chronologically for as long as the time you need for the growth assets to grow unencumbered. Based on S&P data, equities outperform bonds 82% of the time on a rolling 10-year basis, which seems like a proper time horizon for a cash flow matching strategy. Buying time should be a major strategy for pension plans and its liquidity needs.

Cash Flow Matching

Cash flow matching is a very old and well tested fixed income strategy. It used to be called Dedication in the 1970-1990s. It is an accurate and tedious process to build a bond portfolio whose cash flows (principal + interest) will cash flow match the liability cash flows (B + E) monthly. It is a future value (FV) matching process not present value (PV), which differentiates it from Immunization and duration matching strategies that are subject to great volatility and uncertainty of cash flows since they are focused on present value matching. Interest rates change every day across the yield curve and term structure of liabilities making PV matching mission impossible. The greatest value of bonds is the certainty of their cash flows (FV). Liability cash flows tend to be quite certain as well, especially for Retired Lives. That is why bonds have been used historically to fund liability cash flows. Today it is referred to as cash flow driven investing (CDI) especially in Europe and Canada. Ryan ALM believes that the value in bonds is the certainty of their cash flows. We do not view bonds as performance or growth assets. We see bonds as the liquidity assets!

Buy Time!

By cash flow matching B + E for the time you need

Let bonds be the liquidity assets and fund B + E chronologically

Let the performance assets grow unencumbered for the time you need (7-10 years)

Response to: Presidential Memo on Pensions

Response to: Presidential Memo on Pensions Mr. President, I applaud your memo of October 22 to the Secretaries of Treasury, Commerce and Labor. You gave them an order to review...

Source: Response to: Presidential Memo on Pensions

Response to: Presidential Memo on Pensions

Mr. President,

I applaud your memo of October 22 to the Secretaries of Treasury, Commerce and Labor. You gave them an order to review the Delphi pension matter and inform you “within 90 days of this memorandum of any appropriate action that may be taken, consistent with applicable law to (i) address affected Delphi retirees’ lost pension benefits and (ii) bring transparency to the decision to terminate the plan. This review shall include an evaluation of the feasibility of enacting legislation.”

The solution you are looking for can be found in the Butch Lewis Act (BLA) passed by the House through a bipartisan vote (all Democrats + 29 Republicans) on July 26, 2019 as H.R. 397. It has been awaiting approval by the Senate since then. The BLA would create a new agency under the Treasury Department called the Pension Rehabilitation Administration (PRA). The PRA would provide low-interest-rate loans to critical and declining multi-employer pensions at the 30-year Treasury rate plus a profit margin (@ 0.25%). The BLA would provide 100% payment of all retirees benefits in sharp contrast to the PBGC limit of $12,870 for a 30-years of services retiree ($35.75 x 12 months x years of service). The Council of Budget Office estimates the cost of the BLA at $34 billion (if no loans are repaid), which can be minimized by the fact that all PRA loans come with a profit margin. Even at $34 billion it is a small burden compared to the potential cost to cover 1.4 million workers’ pensions affected by the current pension crisis. The PBGC is not the answer… but the BLA is. I urge you to have the Senate approve the BLA legislation that is awaiting their approval for over 15 months now. Time is of the essence!

God Bless Pension America!